TL;DR:

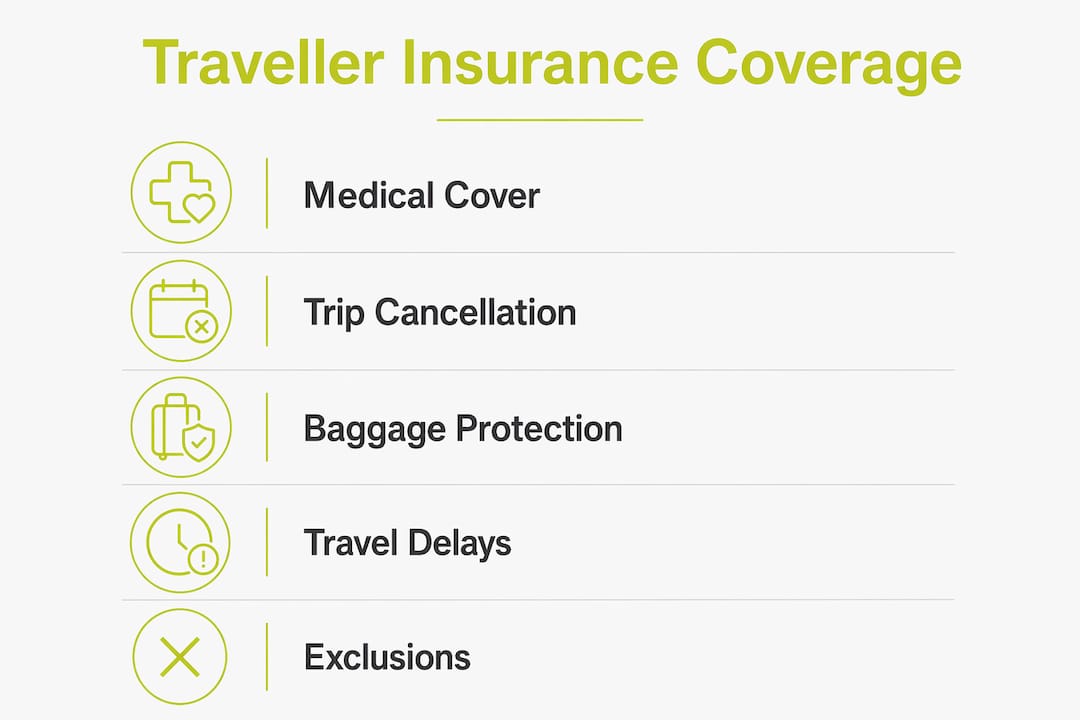

- Travel insurance provides financial protection against unexpected trip costs, including medical emergencies and cancellations.

- It covers emergency medical treatment, evacuations, baggage issues, and delays, with specific exclusions for pre-existing conditions and high-risk activities.

Travel insurance is defined as a financial safety net that reimburses you for unexpected costs before or during a trip, including medical emergencies, trip cancellations, lost baggage, and travel delays. Understanding what does travelers insurance cover is not just useful knowledge. It is the difference between a manageable setback and a financially devastating one. Comprehensive policies cover medical emergencies, evacuations, cancellations, luggage loss, and travel delays. Basic plans focus on emergency medical costs, while fuller options add trip cancellation and interruption protection. Knowing the scope of your policy before you depart gives you real control over your risk.

Which types of medical coverage does travellers insurance include?

Emergency medical coverage is the most critical component of any travel insurance policy. Standard domestic health insurance, including Medicare, does not cover medical treatment abroad. Without dedicated travel medical insurance, you face the full cost of foreign hospital care out of your own pocket.

Travel medical insurance covers three core areas:

- Emergency medical treatment: Hospital stays, surgery, and doctor consultations abroad, up to the policy’s stated limit.

- Emergency dental care: Acute dental pain or injury treatment in a foreign country, though routine dental work is excluded.

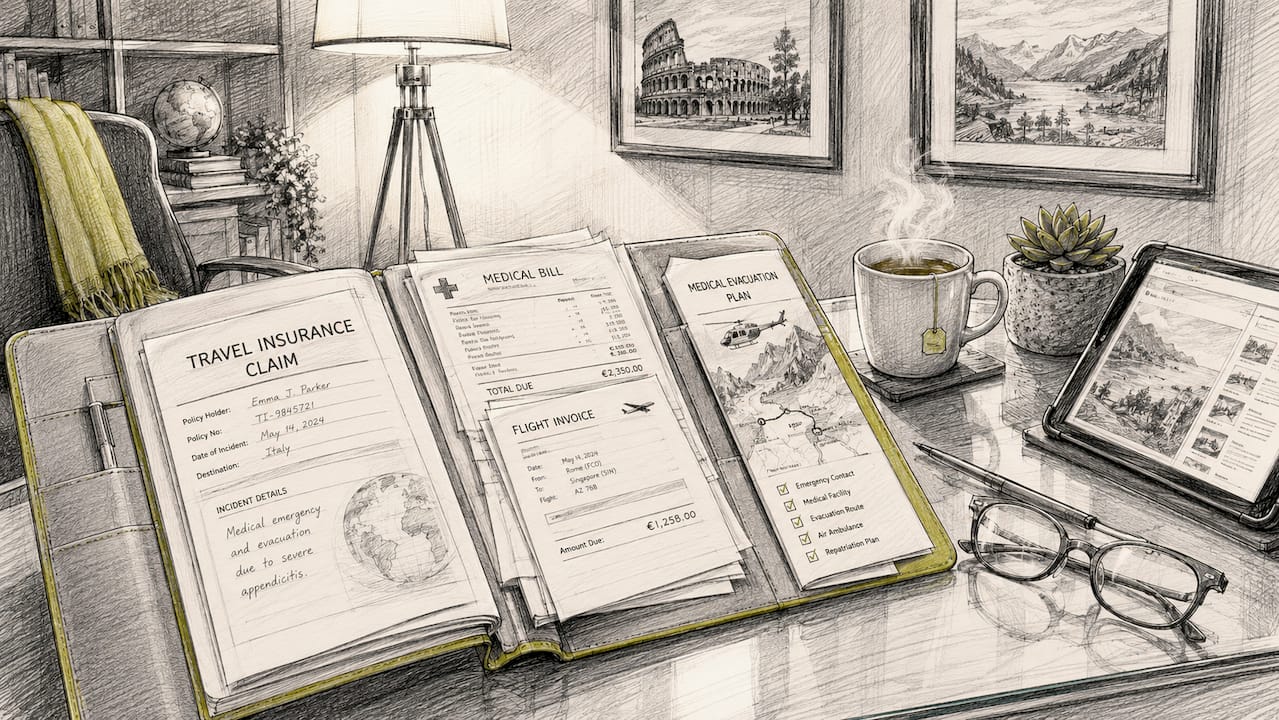

- Medical evacuation and repatriation: Transport to a better-equipped facility or back to your home country when local care is inadequate. Medical evacuation is particularly critical for remote destinations where local hospitals cannot handle serious conditions.

The cost of a medical evacuation flight can run into tens of thousands of pounds. A policy that covers this expense is not a luxury. It is a practical necessity for any international trip.

Many policies also require pre-authorisation from the insurer before you receive non-emergency treatment abroad. Insurers frequently exclude coverage for activities they classify as high-risk unless you have added a specific rider. Failing to get pre-approval or disclosing a relevant activity can result in a denied claim.

Pro Tip: Always carry your insurer’s emergency contact number separately from your phone. If your phone is lost or stolen during a medical crisis, you still need to reach your insurer for pre-authorisation.

For a clear breakdown of how travel medical cover differs from standard health policies, the guide on health and travel insurance differences is worth reading before you buy.

How does travellers insurance protect against cancellations, interruptions, and delays?

Trip cancellation, interruption, and delay coverage addresses the financial loss when your plans change through no fault of your own. These three protections are related but distinct, and confusing them is one of the most common mistakes travellers make.

Here is how each one works:

-

Trip cancellation: Reimburses prepaid, non-refundable costs when you cancel before departure for a covered reason. Covered reasons typically include serious illness, a family bereavement, jury duty, natural disaster at the destination, or a travel advisory issued by your government. Voluntary cancellations are excluded.

-

Trip interruption: Applies when you must cut a trip short after it has already begun. The policy reimburses unused, prepaid costs and may cover the additional cost of an early return flight. This coverage activates for the same categories of covered reasons as cancellation.

-

Trip delay: Reimburses meals, accommodation, and local transport costs when your carrier delays your journey beyond the policy’s waiting period. Trip delay coverage activates after a wait of typically 3–12 hours, depending on the policy terms.

The key distinction is timing. Cancellation applies before departure. Interruption applies during the trip. Delay applies when you are stuck in transit.

One add-on worth understanding is “Cancel for Any Reason” cover, known as CFAR. CFAR coverage is an optional upgrade that lets you cancel for reasons outside the standard list, such as simply changing your mind. It carries a higher premium and is not available on all policies. If you are booking a trip with significant non-refundable costs and uncertain circumstances, CFAR offers a level of flexibility that standard cancellation cover cannot match.

Pro Tip: Purchase your travel insurance as soon as you make your first trip payment. Many cancellation benefits only apply if you buy the policy within a set number of days of your initial booking, often 14–21 days.

What baggage and personal belongings protection does travellers insurance provide?

Baggage cover protects you against the financial impact of lost, delayed, stolen, or damaged luggage and personal items. The cover operates differently depending on whether your bags are delayed or permanently lost.

Baggage delay cover

Baggage delay coverage triggers when your bags are delayed by 6–24 hours, reimbursing you for essential purchases such as clothing and toiletries. Policies commonly require a 12–24 hour delay before the benefit activates. Keep all receipts for purchases made during the delay period, as the insurer will require them.

Baggage loss and theft

When bags are permanently lost, the process takes longer. Insurers typically declare baggage officially lost after a 14–21 day search period. You cannot file a permanent loss claim until the carrier formally confirms the bags are gone. This waiting period is standard across most carriers and affects your claim timeline significantly.

| Scenario | Typical trigger | What is reimbursed |

|---|---|---|

| Baggage delay | 12–24 hour delay | Clothing, toiletries, essentials |

| Baggage loss | 14–21 days after carrier declares lost | Replacement value up to policy limit |

| Baggage theft | Police report required | Replacement value up to policy limit |

| Damaged baggage | Damage report from carrier | Repair or replacement up to limit |

Key points to keep in mind:

- High-value items such as jewellery, cameras, and laptops often have sub-limits within the overall baggage benefit. Check your policy schedule for these caps.

- Airline liability is separate from your travel insurance baggage cover. The airline’s liability under the Montreal Convention is limited and may not cover the full value of your belongings.

- Documentation matters. File a Property Irregularity Report with the airline at the airport immediately. Without this report, most insurers will not process a baggage claim.

Planning a trip for yourself, a resident, or visiting family? UGB + Ekta can arrange travel insurance for seniors up to 100 years old. Just click here: https://ektatraveling.com/?partner_uid=808 and add the promo code “UGB” to receive an additional 10% discount.

What are common exclusions and special considerations in travel cover?

Travel insurance policies contain exclusions that can catch you off guard if you have not read the policy terms carefully. Knowing what is not covered is just as important as knowing what is.

Common exclusions include:

- Pre-existing medical conditions: Most standard policies exclude conditions you had before purchasing the policy. Some insurers offer cover for stable pre-existing conditions at an additional premium. The guide on travel insurance with medical conditions explains how to approach this.

- Pandemics and epidemics: Many policies exclude losses arising from declared pandemics unless you have purchased a specific rider.

- High-risk activities: Activities like skiing, scuba diving, and bungee jumping may void your medical coverage for related injuries unless you add an adventure sports rider.

- Voluntary cancellation: Changing your mind about a trip is not a covered reason under standard cancellation cover. CFAR is the only way to address this.

- Geographical limits: Some policies exclude certain countries or regions, particularly those under government travel advisories. Check your destination against the policy’s territorial scope.

The value of travel insurance depends on your individual circumstances, your existing coverage, and your financial exposure on non-refundable costs. A weekend city break carries different risk than a three-week trekking expedition in a remote region. Match the policy to the trip, not the other way around.

If you are travelling as part of a group, the benefits of group tours for adventure travellers include shared logistical support, but each traveller still needs individual medical and cancellation cover.

Key takeaways

Travel insurance covers medical emergencies, trip cancellations, baggage loss, and travel delays, but exclusions for pre-existing conditions, high-risk activities, and voluntary cancellations mean reading your policy terms is non-negotiable.

| Point | Details |

|---|---|

| Medical cover is the priority | Domestic health insurance does not cover overseas treatment; dedicated travel medical cover fills this gap. |

| Cancellation vs interruption | Cancellation applies before departure; interruption applies once your trip has begun. |

| Baggage delay vs loss | Delay cover activates after 6–24 hours; loss claims require a 14–21 day carrier declaration. |

| Exclusions can void claims | High-risk activities, pre-existing conditions, and pandemics are commonly excluded without specific riders. |

| CFAR adds flexibility | Cancel for Any Reason cover costs more but protects non-refundable costs when standard reasons do not apply. |

What I have learned from years of watching travellers get this wrong

Travel insurance is one of those purchases people treat as a formality. They tick the box, pay the premium, and assume they are covered. The reality is more complicated, and the gap between assumption and actual cover is where most claims disputes happen.

The single most common mistake I see is travellers assuming their existing health insurance extends abroad. It almost never does. Standard domestic health insurance excludes overseas medical treatment as a rule, not an exception. The second most common mistake is buying the cheapest policy without checking whether it covers the specific activities planned for the trip.

My honest view is that the worth of a travel policy is entirely relative. As one analysis from Forbes Advisor notes, the value of travel insurance depends on your individual circumstances, your existing coverage, and your financial risk tolerance for non-refundable costs. A traveller with a fully refundable booking and robust employer health cover needs a very different policy from someone with a complex medical history booking a non-refundable safari.

Read the exclusions first. Not the benefits page. The exclusions. That is where the real policy lives.

— Coert

Travel cover that fits your trip, not just your budget

Choosing the right travel insurance means matching the policy to your actual risk, not just finding the lowest premium. Unparalleledglobalbenefits specialises in international insurance solutions for travellers, expats, students, and visiting families, with plans designed around real-world coverage needs rather than one-size-fits-all products.

Whether you need straightforward trip protection or a policy that covers pre-existing conditions and medical evacuation, the international health insurance guide is a practical starting point. Unparalleledglobalbenefits works with a wide range of international carriers to find cover that reflects your destination, your health profile, and your travel style.

Planning a trip for yourself, a resident, or visiting family? UGB + Ekta can arrange travel insurance for seniors up to 100 years old. Just click here: https://ektatraveling.com/?partner_uid=808 and add the promo code “UGB” to receive an additional 10% discount.

FAQ

What does travellers insurance cover as standard?

Standard travel insurance covers emergency medical treatment abroad, trip cancellation for covered reasons, baggage loss or delay, and travel delays. Basic plans focus on medical costs; comprehensive plans add cancellation and interruption protection.

Does travel insurance cover pre-existing medical conditions?

Most standard policies exclude pre-existing conditions by default. Some insurers offer cover for stable conditions at an additional premium, and specialist policies exist for travellers with complex medical histories.

How does the trip cancellation claim process work?

You submit a claim with supporting documentation such as a doctor’s letter or death certificate, and the insurer reimburses your prepaid, non-refundable costs up to the policy limit. Voluntary cancellations are not covered unless you hold a CFAR add-on.

What is the difference between baggage delay and baggage loss cover?

Baggage delay cover reimburses essential purchases when your bags are delayed by 6–24 hours. Baggage loss cover applies only after the airline formally declares your bags lost, typically after a 14–21 day search period.

Does travel insurance cover adventure sports?

Standard policies exclude injuries from high-risk activities such as skiing, scuba diving, and bungee jumping. You need to add an adventure sports rider to your policy before your trip to receive medical cover for these activities.

Watch this short video for more guidance on protecting yourself abroad:

https://youtu.be/bjzvma7Sh1g

Recommended

- Types of Travel Insurance: Essential Cover in 2025

- What is covered in travel insurance: 2026 guide – Unparalleled Global Benefits

- Why travel with insurance: Stay safe abroad in 2026 – Unparalleled Global Benefits

- Multi trip travel insurance: 12% choose annual cover in 2026 – Unparalleled Global Benefits