TL;DR:

- Multi-trip insurance is an annual policy that covers unlimited trips abroad within a 12-month period, provided each trip stays within the specified duration limit. It offers strong emergency medical protection and simplifies travel planning for frequent travelers, often costing less than multiple single-trip policies. Travelers should carefully check coverage limits, exclusions, and declare pre-existing conditions to ensure comprehensive protection.

Multi-trip insurance is defined as a single annual policy that covers unlimited trips abroad within a 12-month period, removing the need to buy separate cover each time you travel. If you take three or more trips a year, understanding how does multi trip insurance work could save you both money and administrative effort. Providers such as Post Office Travel Insurance, Admiral, and MoneySuperMarket all offer annual policies that typically include emergency medical cover, trip disruption protection, and limited baggage and car rental cover. The core appeal is straightforward: one policy, one renewal date, and continuous protection for every trip you take throughout the year.

How does multi trip insurance work: key features and coverage

Multi-trip insurance, also called annual travel insurance, operates on a simple principle. You pay one premium and receive cover for every trip you take within the policy year, provided each individual trip stays within the policy’s maximum duration limit.

Annual policies cover unlimited trips but restrict how long any single trip can last. Most providers set this limit at 30, 45, or 60 days per trip. If you plan a three-month sabbatical in Southeast Asia, a standard multi-trip policy will not cover the full duration. You would need a separate single-trip policy for that journey.

What does a typical policy cover?

The coverage focus of annual travel insurance sits firmly on emergency medical protection. Here is what most policies include:

- Emergency medical expenses and evacuation: This is the strongest element of any multi-trip plan. Medical bills abroad can run into tens of thousands of pounds, so this cover is the most valuable component.

- Trip cancellation and interruption: Cover applies if you must cancel or cut short a trip due to illness, bereavement, or other listed reasons.

- Travel delays: Compensation for delays caused by airline or transport failures.

- Baggage and personal belongings: Annual plans limit baggage cover more than single-trip policies typically do.

- Rental car excess: Some providers include this, but many do not. Always check the policy wording.

Multi-trip policies generally exclude Cancel For Any Reason cover, which is a benefit sometimes available on single-trip plans. That exclusion matters if you travel for business and need maximum flexibility to cancel without a specific qualifying reason.

Pro Tip: Read the “what is a trip” definition in your policy documents carefully. Some insurers count a return home mid-journey as ending one trip and starting another, which can affect your duration limit.

| Coverage Type | Typical Multi-Trip Cover | Notes |

|---|---|---|

| Emergency medical | High (often unlimited) | Core strength of annual policies |

| Trip cancellation | Moderate | Listed reasons only |

| Baggage loss | Limited | Lower limits than single-trip |

| Rental car excess | Variable | Often excluded or add-on only |

| Cancel For Any Reason | Not included | Single-trip policies only |

| Hazardous sports | Optional add-on | Some providers cover skiing and scuba diving |

Multi trip vs single trip insurance: which is right for you?

The trade-off between annual and single-trip insurance is convenience versus tailored coverage. Annual policies provide consistent protection across all trips, while single-trip plans let you adjust cover precisely to each journey’s risks and duration.

Cost is the deciding factor for most travellers. Cumulative premiums for single-trip policies usually exceed the cost of one annual policy after three or more trips. That means if you travel four times a year for short breaks in Europe or North America, an annual policy almost certainly costs less overall.

Single-trip insurance wins on flexibility. Single-trip policies offer tailored options such as Cancel For Any Reason, higher baggage limits, and cover for trips lasting longer than 60 days. If you take one long trip per year or travel to a destination with specific risks, a single-trip policy is the better fit.

| Factor | Multi-Trip (Annual) | Single-Trip |

|---|---|---|

| Cost for 3+ trips | More cost-effective | More expensive overall |

| Trip duration | Limited (30–60 days max) | Unlimited, set per trip |

| Baggage cover | Lower limits | Higher, customisable |

| Cancel For Any Reason | Not available | Available on some plans |

| Hazardous sports | Add-on required | Can be included per trip |

| Convenience | One policy, no reapplication | New policy needed each trip |

Pro Tip: If you travel for both leisure and business, check whether your annual policy covers both trip types. Some policies restrict cover to leisure travel only, leaving business trips unprotected.

For families travelling together frequently, a family multi-trip policy can extend the same annual cover to all members under one premium, which adds further savings. If you are visiting multiple countries on a single trip, a multi-country travel guide can help you confirm your annual policy covers every destination.

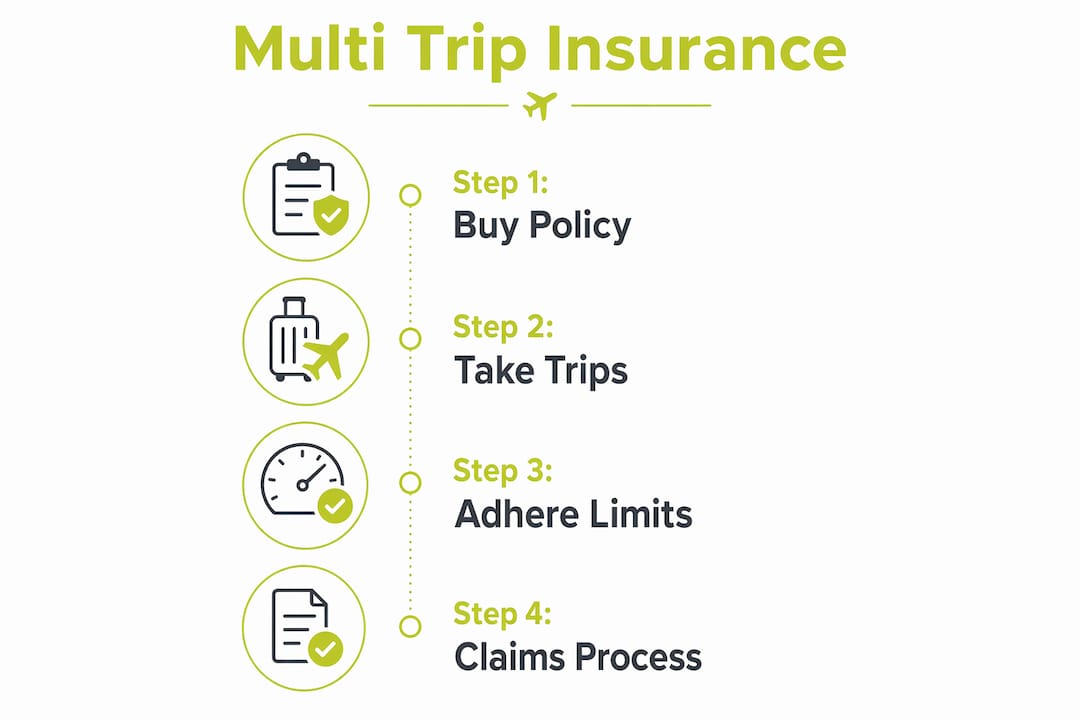

How to buy multi trip insurance: a practical step-by-step guide

Buying the right annual policy requires more than picking the cheapest quote. Follow these steps to avoid coverage gaps.

-

Assess your travel frequency and destinations. Count how many trips you took last year and where you went. If you visited the USA or Canada, confirm the policy includes North American medical cover, as costs there are significantly higher than in Europe.

-

Choose your maximum trip duration. Check the policy’s maximum trip duration before buying. If your longest trip is 45 days, a 30-day limit policy will leave you exposed. Select 45 or 60 days to be safe.

-

Declare pre-existing medical conditions. Failing to declare a condition can void your entire policy. Providers such as insurers specialising in health conditions offer annual plans that include cover for pre-existing conditions, sometimes at a higher premium.

-

Check sporting activities cover. If you ski, snowboard, or scuba dive, confirm these activities are included. Some providers cover hazardous sports as standard, while others require a paid add-on.

-

Compare at least three quotes. Use comparison platforms and check provider reputations through independent review sites. Look beyond the premium to compare excess amounts, medical cover limits, and exclusion lists.

-

Buy before your first trip departs. Trip cancellation cover only applies to trips booked after the policy start date. Buying early protects you from the moment you book your first journey.

-

Set a renewal reminder. Annual policies do not automatically adjust to your changing travel habits. Review your policy each year to confirm the trip duration limit and destination cover still match your plans.

Pro Tip: If you are unsure whether annual or single-trip cover suits you better, use an annual vs single-trip calculator to compare total costs based on your actual travel pattern.

Common questions when using multi trip insurance

Even after buying a policy, questions arise when you actually use it. Here are the situations travellers encounter most often.

What counts as a new trip? A trip typically begins when you leave your home country and ends when you return. If you fly home between two holidays, that counts as two separate trips. Each must stay within your policy’s per-trip duration limit.

What happens if your trip runs over the duration limit? Cover stops at the limit. If you are abroad on day 31 of a 30-day policy and you fall ill, you are not covered. Contact your insurer before departure if you think a trip might run long. Some providers allow a one-off extension.

Can you make multiple claims in one policy year? Claims can be made multiple times within a policy year, provided each trip stays within the duration limit. Each claim is assessed independently. Making several claims in one year may affect your renewal premium.

“Annual travel insurance is designed for frequency, not duration. If your trips are short and regular, it works well. If one trip is unusually long or high-risk, consider supplementing with a single-trip policy for that specific journey.”

When should you switch to single-trip cover? Consider switching if you take only one or two trips per year, if a trip exceeds your annual policy’s duration limit, or if you need Cancel For Any Reason cover. For a detailed comparison of medical cover options, the guide on single-trip medical insurance explains the differences clearly.

Key takeaways

Multi-trip insurance works best for frequent travellers taking three or more short trips per year, offering strong emergency medical cover under one annual policy with per-trip duration limits of 30–60 days.

| Point | Details |

|---|---|

| Annual policy structure | One premium covers unlimited trips within 12 months, each within the duration limit. |

| Medical cover is the strength | Emergency medical and evacuation cover is the most valuable element of any annual plan. |

| Duration limits matter | Trips exceeding 30–60 days require separate single-trip cover to avoid gaps. |

| Cost advantage at three-plus trips | Annual premiums typically cost less than buying single-trip cover three or more times. |

| Check exclusions before buying | Cancel For Any Reason and rental car cover are often absent from annual policies. |

Why i think most travellers buy annual cover too late

After years of working with international travellers and expats at Unparalleledglobalbenefits, I have noticed a consistent pattern. Most people only consider annual cover after they have already bought three or four single-trip policies in one year and done the maths. By then, they have overpaid.

The bigger issue is that travellers often underestimate how quickly trips accumulate. A long weekend in Amsterdam, a work trip to New York, a summer holiday in Greece, and a Christmas break in Edinburgh. That is four trips. Four separate policies. Four sets of paperwork. One annual policy handles all of that with a single renewal date.

What I find genuinely underappreciated is the medical cover consistency. With a single-trip policy, you choose your medical limit per trip. With an annual policy, you have the same strong medical protection on every trip, including the spontaneous ones you book at short notice. That consistency has real value.

My honest advice: review your travel pattern every autumn before the next year begins. If you are planning three or more trips, buy your annual policy before you book anything. Trip cancellation cover only kicks in for trips booked after the policy start date. Waiting until January to buy cover for a February trip you booked in November means that cancellation cover is already gone.

One more thing. If you have a pre-existing condition, do not assume annual cover will not work for you. Specialist providers can include your condition, sometimes at a modest additional cost. The international expat health insurance options available in 2026 are considerably more flexible than they were even three years ago.

— Coert

How Unparalleledglobalbenefits can help you travel with confidence

Unparalleledglobalbenefits specialises in international insurance solutions for travellers, expats, and families living or working abroad. Whether you need an annual multi-trip policy, cover for a pre-existing condition, or a plan that works across multiple countries, the team can help you find the right fit.

Explore the full range of travel insurance options to understand what level of cover suits your travel habits. For broader protection abroad, the guide to international expat health insurance is a strong starting point.

Planning a trip for yourself, a resident, or visiting family? UGB + Ekta can arrange travel insurance for seniors up to 100 years old. Just click here: Ekta Travel Insurance and add the promo code “UGB” to receive an additional 10% discount.

Watch this short video for more guidance on choosing the right travel cover:

https://youtu.be/bjzvma7Sh1g

FAQ

What is multi trip insurance?

Multi-trip insurance is an annual policy that covers unlimited trips abroad within a 12-month period under a single premium. Each trip must stay within the policy’s maximum duration limit, typically 30–60 days.

How many trips can you take on an annual policy?

Annual policies cover unlimited trips within the policy year, provided each individual trip does not exceed the maximum duration limit set by your provider.

Is multi trip insurance worth it for three trips a year?

Annual policies become cost-effective at three or more trips per year, as the combined cost of single-trip policies typically exceeds one annual premium at that frequency.

Does multi trip insurance cover pre-existing conditions?

Cover for pre-existing conditions varies by provider. You must declare all conditions when applying, and some insurers offer specialist annual plans that include them, often at an additional premium.

Can you extend a trip that exceeds the policy duration limit?

Some providers allow a one-off trip extension if you contact them before the limit expires. Without an approved extension, cover stops at the maximum duration, leaving you unprotected for the remainder of the trip.

Recommended

- Multi trip travel insurance: 12% choose annual cover in 2026 – Unparalleled Global Benefits

- Multi-country travel insurance: your 2026 guide – Unparalleled Global Benefits

- Family multi trip travel insurance: your 2026 guide – Unparalleled Global Benefits

- Trip protection: your complete 2026 travel guide – Unparalleled Global Benefits