TL;DR:

- Schengen visa health insurance must provide at least €30,000 in medical coverage, including repatriation, across the entire Schengen Area for the full stay. The insurance certificate must explicitly state Schengen coverage, the coverage amount, and include repatriation benefits, matching your passport details and travel dates exactly. Using proper, clear documentation aligned with official requirements is essential to avoid visa rejection.

Schengen visa health insurance requirements mandate a minimum of €30,000 medical coverage, valid across all 26 Schengen Area countries, for the full duration of your stay, and inclusive of medical repatriation. This is not optional guidance. Article 15 of the Schengen Visa Code makes it a legal condition of entry, and lower coverage amounts result in automatic refusal. Whether you are visiting France, Germany, Switzerland, or any other Schengen state, your insurance certificate must satisfy every one of these criteria before a consulate will approve your application. Understanding exactly what is required, and how to present it correctly, is the difference between approval and rejection.

What must schengen visa health insurance include?

The term “travel health insurance” is the standard industry term for what visa applicants commonly call Schengen visa insurance. The policy must cover specific medical events, not just general healthcare. Here is what every compliant policy must include:

- Emergency medical treatment and hospitalisation. This covers the cost of urgent care, surgery, and inpatient stays if you fall ill or are injured abroad.

- Medical repatriation. Some budget policies exclude repatriation, which causes direct visa refusal. Your certificate must state this benefit explicitly.

- Repatriation of remains. If the worst happens, the policy must cover the cost of returning your remains to your home country.

- Prescription medicine and urgent dental care. Many applicants overlook these. Consulates expect them to be part of the package.

- A minimum coverage limit of €30,000. This figure is set by law. Policies offering €10,000 or €20,000 are non-compliant, regardless of how comprehensive they appear in other respects.

The €30,000 minimum is a floor, not a ceiling. For longer trips or destinations with high medical costs, such as Switzerland or Norway, a higher limit gives you genuine protection beyond mere compliance.

Pro Tip: Purchase a policy with a €50,000 or higher limit if your budget allows. It costs very little extra and removes any doubt at the consulate window.

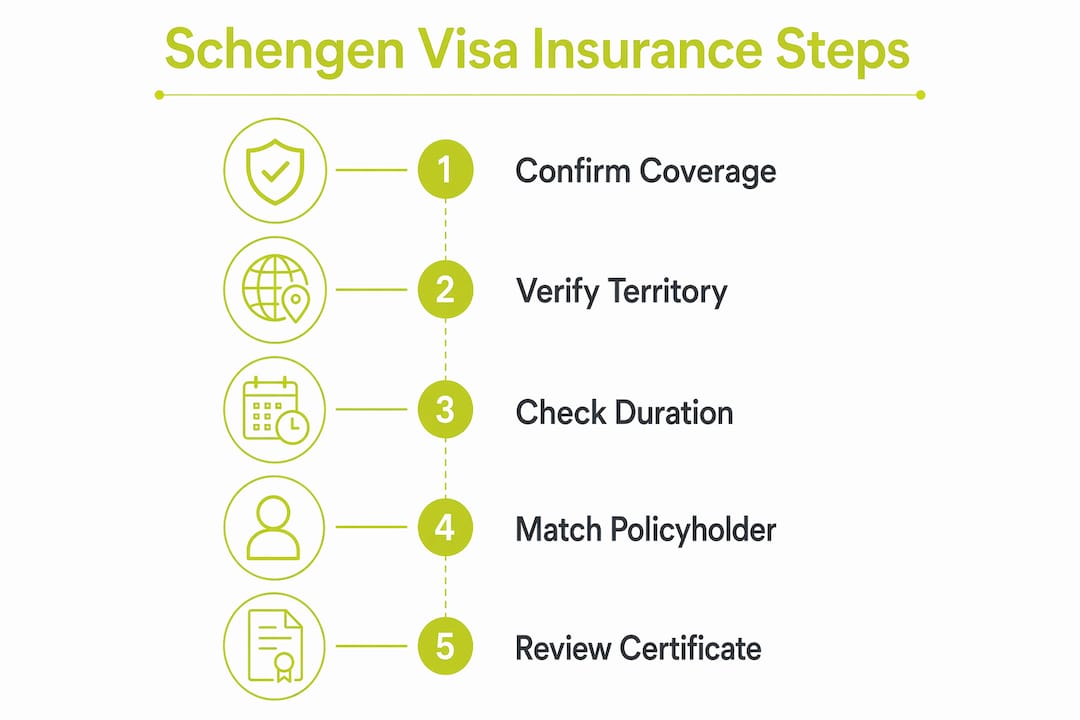

How does your insurance certificate meet schengen standards?

Visa officers scrutinise the exact certificate wording more than the underlying policy terms. A policy can be fully compliant, yet still cause rejection if the certificate is unclear. Follow these steps to get it right.

- Verify your name matches your passport exactly. Even a minor spelling difference can trigger a refusal. Check middle names, hyphens in surnames, and accented characters.

- Confirm coverage dates span your entire trip. Policies with gaps in start or end dates often cause visa refusal. If your visa is for 30 days, your insurance must cover all 30 days, including travel days.

- Check for “Schengen Area” wording. Certificates must explicitly state “Schengen Area” rather than “Europe” or “EU.” Switzerland is part of the Schengen Area but not the European Union, so “EU” wording is legally insufficient.

- Confirm the €30,000 coverage limit is stated clearly. The figure must appear on the certificate itself, not just in the policy schedule.

- Check that medical repatriation is listed. The certificate must name this benefit. A general reference to “emergency cover” is not enough.

- Remove ambiguous deductibles or co-pay references. Consulates reject certificates that suggest gaps or exclusions in coverage. If your policy has a deductible, confirm it does not appear in a way that implies reduced coverage.

Pro Tip: Treat your insurance policy and your insurance certificate as two separate documents. Consulates focus on the certificate details, not the full policy wording. Always submit the certificate, not the policy booklet.

The table below summarises the certificate checklist at a glance.

| Certificate Element | Requirement |

|---|---|

| Policyholder name | Exact match with passport |

| Coverage territory | Must state “Schengen Area” explicitly |

| Coverage dates | Must cover entire planned stay |

| Medical coverage limit | Minimum €30,000 stated on certificate |

| Repatriation cover | Must be named explicitly |

| Deductibles | Must not suggest gaps or reduced cover |

Common pitfalls when choosing schengen area insurance

Many applicants arrive at the consulate with the wrong document. These are the mistakes that cause the most rejections.

- Using ordinary domestic health insurance. Regular health insurance from your home country usually does not meet Schengen visa insurance requirements. It typically lacks repatriation cover, does not state Schengen Area coverage, and does not produce a compliant certificate format.

- Choosing a policy with “EU” or “Europe” territorial wording. As noted above, this is insufficient. Switzerland, Iceland, Norway, and Liechtenstein are Schengen states but not EU members. A certificate that says “EU only” excludes them.

- Buying insurance that starts the day after departure. Coverage must begin on your first day of travel, including the outbound journey. A one-day gap at the start is enough to trigger refusal.

- Submitting a digital confirmation email instead of a formal certificate. Some consulates expect printed, consulate-ready insurance certificates separate from policy documents. A marketing brochure or email confirmation is not acceptable.

- Selecting a policy from an insurer not authorised in a Schengen state. Policies must come from insurers authorised in a Schengen state or collaborating insurers. This ensures the policy is recognised and trusted by consular offices.

- Assuming travel insurance and Schengen visa insurance are the same product. Standard travel insurance often covers trip cancellation and baggage but may not meet the specific medical and repatriation thresholds required for a Schengen visa. Always confirm compliance before purchasing.

You can read a detailed breakdown of the step-by-step insurance requirements on the Unparalleledglobalbenefits website if you want to cross-check your policy against each criterion.

What are the best options for schengen visa health insurance?

The right policy depends on your trip length, nationality, and how many times you plan to enter the Schengen Area. Here is how the main options compare.

| Policy Type | Best For | Key Advantage | Watch Out For |

|---|---|---|---|

| Single-trip travel medical insurance | One visit, fixed dates | Affordable, easy to match exact dates | Does not cover multiple trips |

| Multi-trip annual insurance | Frequent travellers | Cost-effective for 3+ trips per year | Check per-trip day limits |

| Schengen-specific visa insurance | First-time applicants | Designed to meet consulate requirements | Confirm €30,000 limit is stated |

| International health insurance | Long-stay or expat applicants | Broader coverage beyond emergencies | May need a separate Schengen certificate |

For most first-time applicants taking a single trip, a dedicated Schengen visa insurance product is the most straightforward choice. These policies are built specifically to meet consular requirements, and reputable providers issue certificates in a format that consulates recognise immediately.

When comparing providers, look for insurers authorised within the Schengen Area, clear certificate issuance, no deductibles on the certificate, and explicit repatriation cover. Providers such as those listed on Unparalleledglobalbenefits offer compliant Schengen visa coverage with certificates ready for submission.

For applicants with pre-existing conditions, a specialist policy is worth the additional cost. Some standard Schengen insurance products exclude pre-existing conditions entirely, which could leave you underinsured even if the certificate passes the consulate check. The Unparalleledglobalbenefits guide on travel insurance for health conditions covers this in detail.

Planning a trip for yourself, a resident, or visiting family? UGB + Ekta can arrange travel insurance for seniors up to 100 years old. Just click here: https://ektatraveling.com/?partner_uid=808 and add the promo code “UGB” to receive an additional 10% discount.

Watch this short overview for additional guidance on selecting the right cover:

https://youtu.be/bjzvma7Sh1g

Key takeaways

Schengen visa health insurance compliance depends on the certificate wording as much as the policy itself, so verify every detail before submission.

| Point | Details |

|---|---|

| Minimum €30,000 coverage | Article 15 of the Schengen Visa Code mandates this; lower amounts cause automatic refusal. |

| “Schengen Area” wording required | “EU” or “Europe” is insufficient; Switzerland and Norway are Schengen but not EU. |

| Certificate over policy document | Consulates review the certificate, not the full policy; submit the correct document. |

| Repatriation must be named | Budget policies often exclude this; confirm it appears explicitly on your certificate. |

| Dates must match your stay exactly | Any gap in coverage dates, even one day, is grounds for visa refusal. |

Why certificate clarity matters more than policy price

I have reviewed a considerable number of Schengen visa insurance cases over the years, and the pattern is consistent. Applicants who are refused rarely bought the wrong policy. They submitted the wrong document, or they bought a policy with unclear certificate wording and assumed it would pass.

The single most useful shift in thinking is this: stop evaluating insurance by price and start evaluating it by certificate quality. A €15 policy with a clean, explicit certificate will outperform a €60 policy with vague territorial wording every time. Visa officers are not reading your policy schedule. They are reading one page, and that page needs to say the right things in the right order.

My other strong recommendation is to buy early. Waiting until the week before your appointment creates pressure, and pressure leads to shortcuts. Buying four to six weeks ahead gives you time to request a corrected certificate if something is wrong, without risking your appointment date.

One thing I see applicants get wrong repeatedly is assuming that “Europe” covers everything they need. It does not. Switzerland alone is enough to invalidate an EU-only certificate if your itinerary includes Geneva or Zurich. Always read the territorial clause on the certificate before you submit anything.

If you are applying through a German, French, or Dutch consulate in particular, expect close scrutiny of the repatriation wording. These consulates are known to reject certificates that reference repatriation only in the policy booklet rather than on the certificate face. Get it in writing, on the certificate, before you apply.

— Coert

Get schengen-compliant cover through Unparalleledglobalbenefits

Unparalleledglobalbenefits specialises in international health and travel insurance for people living, working, and travelling abroad. If you need a policy that meets every Schengen visa insurance requirement, including the €30,000 minimum, explicit repatriation cover, and a consulate-ready certificate, the team can help you find the right plan quickly.

Whether you are a first-time applicant or a frequent traveller needing annual cover, Unparalleledglobalbenefits offers access to international health plans for expats and travellers that are built for exactly this purpose. You can compare options, request a quote, and receive your certificate in a format that consulates accept. Do not leave your visa application to chance with a policy that may not pass scrutiny.

FAQ

What is the minimum medical coverage for a schengen visa?

The minimum is €30,000, as required by Article 15 of the Schengen Visa Code. Policies with lower limits result in automatic visa refusal.

Does “europe” coverage on my certificate satisfy schengen requirements?

No. Your certificate must explicitly state “Schengen Area.” Countries such as Switzerland and Norway are Schengen members but not EU members, so “EU” or “Europe” wording is legally insufficient.

Can i use my regular health insurance for a schengen visa application?

Ordinary domestic health insurance generally does not meet Schengen travel insurance requirements. It typically lacks repatriation cover, does not state Schengen Area coverage, and does not produce a compliant certificate.

Does my insurance need to cover the entire trip duration?

Yes. Coverage must span every day of your planned stay, including travel days. A single-day gap at the start or end of the policy is grounds for refusal.

What document should i submit to the consulate?

Submit the insurance certificate, not the full policy document. Visa officers focus on the certificate wording, and a printed, consulate-ready certificate is required. Digital confirmation emails or marketing brochures are not acceptable.

Recommended

- Minimum insurance for Schengen visa: what you need in 2026 – Unparalleled Global Benefits

- Insurance Requirements for Schengen Visa: A Step-by-Step Guide – Unparalleled Global Benefits

- Travel Insurance for Schengen Visa: Get Approved Easily – Unparalleled Global Benefits

- Get the minimum travel insurance for Schengen visa compliance – Unparalleled Global Benefits