TL;DR:

- Medical evacuation and repatriation insurance cover emergency medical transport when local care is unavailable abroad. They are essential for expats and travelers, as costs can reach hundreds of thousands of dollars, and standard insurance often excludes such coverage. The insurer authorizes evacuation based on medical necessity, focusing on the nearest adequate facility, not necessarily your home country.

Medical evacuation and repatriation insurance covers the cost of emergency medical transport when adequate care is unavailable at your location abroad. Without it, a single air ambulance flight can cost between $25,000 and $250,000, depending on distance and medical complexity. Standard domestic health insurance plans frequently exclude medical evacuation entirely, leaving travellers personally liable for those costs. For expats and international travellers, this coverage is not optional. It is the financial safety net that makes the difference between a manageable crisis and a catastrophic one.

What does medical evacuation and repatriation insurance cover?

Medical evacuation, repatriation, and repatriation of remains are legally distinct with different processes and cost structures. Understanding each one prevents nasty surprises when you need to make a claim.

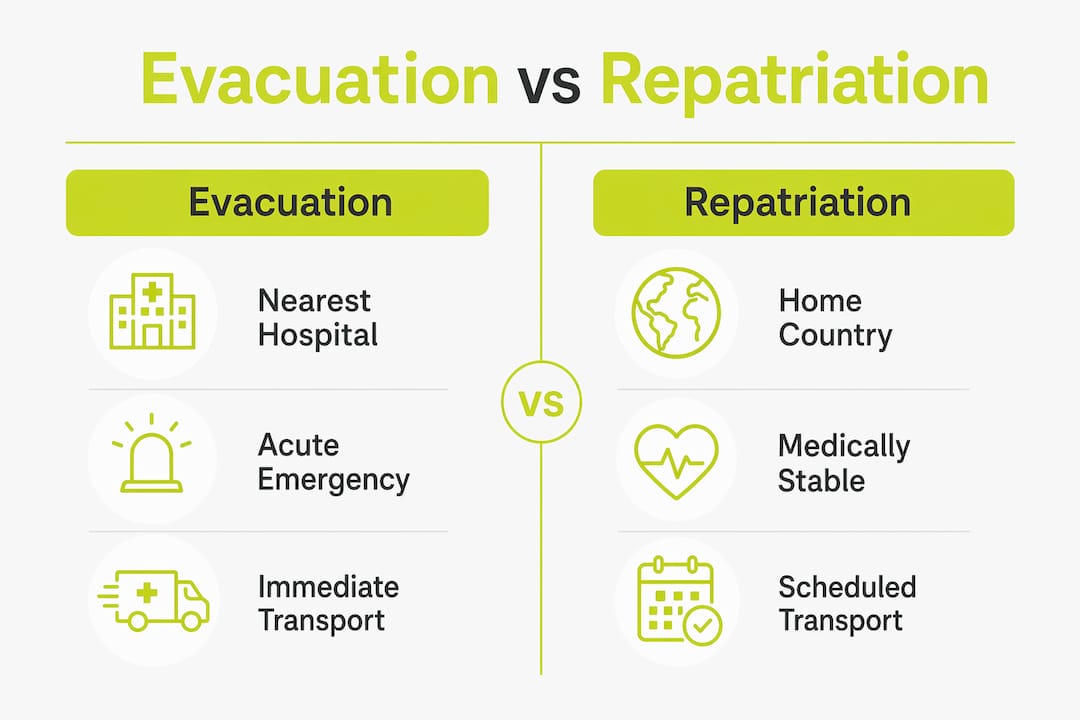

Medical evacuation

Medical evacuation covers transport to the nearest facility capable of treating your condition. This typically includes:

- Air ambulance or medically equipped aircraft

- Medical escort (doctor or nurse on board)

- ICU-level inflight care for critical patients

- Ground ambulance to and from aircraft

The key word here is “nearest.” Evacuation does not mean transport home. It means transport to the closest hospital that can adequately treat you, which may be in a neighbouring country rather than your own.

Repatriation

Repatriation applies once you are medically stable. At that point, your insurer may approve transport back to your home country for ongoing treatment or recovery. This is a separate benefit from evacuation and often carries its own coverage cap. Not every policy includes repatriation automatically, so you need to check your policy wording carefully.

Repatriation of remains

If the worst happens, repatriation of remains covers the return of a deceased person to their home country. This process involves embalming, a sealed container, customs documentation, and significant transport logistics. Costs for remains transport can reach £8,000 to £40,000 or more internationally. Many travellers overlook this benefit entirely, yet it is one of the most emotionally and financially significant aspects of a policy.

Common exclusions

Policies frequently exclude coverage for:

- Pre-existing medical conditions (unless declared and accepted)

- Evacuation from countries listed as high-risk or under government travel warnings

- Adventure sports or hazardous activities unless specifically added

- Evacuations not pre-authorised by the insurer’s medical team

Pro Tip: Always read your policy schedule and benefit summary side by side. Some policies bundle evacuation, repatriation, and remains transport under a single combined limit. Others assign separate caps to each. The difference matters enormously when costs run into six figures.

How and when are evacuation or repatriation decisions made?

The insurer’s medical team authorises evacuation, not the patient or their family. This surprises many travellers who assume they can simply request transport home. The decision rests on specific clinical and logistical criteria.

The typical process works as follows:

- Medical emergency occurs. You or someone on your behalf contacts the insurer’s 24-hour emergency line immediately.

- Local assessment. The insurer’s medical team contacts the treating hospital to assess the standard of care available locally.

- Adequacy determination. If local facilities cannot provide the required treatment, evacuation is authorised to the nearest adequate facility.

- Transport arranged. The insurer coordinates the air ambulance, medical escort, and receiving hospital directly.

- Ongoing monitoring. Once stable, the medical team reassesses whether repatriation to your home country is appropriate.

The nearest adequate facility principle is central to every evacuation decision. Insurers will not approve transport to a preferred hospital in your home country if a suitable facility exists closer. This is a common source of frustration for travellers who expect a “get me home” service.

Timing also matters. Evacuation during acute instability carries far higher costs than transport once a patient is stabilised. Insurers balance medical necessity against cost, and their medical teams are trained to make those calls.

Pro Tip: Never arrange your own evacuation transport and expect reimbursement later. Unauthorised evacuations are routinely denied, even when medically necessary. Always call your insurer’s emergency line first.

What are the costs and coverage limits of evacuation insurance?

The financial exposure without proper cover is severe. An intercontinental ICU flight can exceed $200,000. Even a regional air ambulance within Europe or Southeast Asia regularly costs $25,000 to $80,000. These are not edge cases. They are standard costs for medically equipped transport.

| Scenario | Typical cost range |

|---|---|

| Regional air ambulance (within continent) | $25,000–$80,000 |

| Intercontinental ICU flight | $100,000–$250,000+ |

| Repatriation of remains (international) | $5,000–$15,000+ |

| Medical escort (nurse or doctor) | Included or $3,000–$8,000 extra |

Policy benefit caps vary significantly by region and plan tier. European policies typically cap at €50,000 to €250,000. US premium plans can provide $500,000 to $1,000,000 in evacuation cover. Some high-tier European plans reach €500,000. That gap matters if you are travelling between continents.

Emergency medical evacuation is also distinct from emergency medical coverage. Evacuation arranges and pays for transport to adequate care. Medical coverage reimburses your hospital bills once you arrive. You need both, and they often come from different benefit pools within the same policy.

Some travellers supplement their insurance with premium evacuation memberships. These memberships arrange transport to a hospital of your choice, bypassing the insurer’s adequacy gatekeeper. The critical caveat: memberships cover transport only. They do not pay hospital bills. They work best as a complement to full insurance, not a replacement.

Pro Tip: If you are travelling on a cruise, visiting a remote region, or undertaking hazardous activities, opt for the highest evacuation limit available. The cost difference between a standard and premium tier is modest. The cost difference in a real emergency is not.

What are common pitfalls and exclusions in evacuation cover?

Geographic exclusions are one of the most significant traps in evacuation policies. If your destination appears on your insurer’s excluded country list, evacuation costs fall entirely on you. These exclusions shift with geopolitical conditions, so a destination that was covered last year may not be covered this year.

| Common exclusion | What it means for you |

|---|---|

| High-risk country exclusion | No evacuation cover if destination is on the insurer’s restricted list |

| Unauthorised evacuation | Claim denied if you arrange transport without prior insurer approval |

| Pre-existing condition | Evacuation linked to an undisclosed condition may be excluded |

| Adventure activity exclusion | Skiing, diving, or trekking injuries may not be covered unless added |

| Combined benefit cap | Evacuation and repatriation share one limit, which can be exhausted quickly |

Reading fine print is the single most important step before purchasing any evacuation policy. Some policies bundle evacuation, repatriation, and remains transport under one combined limit. If an evacuation costs $80,000 and your combined cap is $100,000, you have only $20,000 left for repatriation and remains transport. That may not be enough.

Confusion around bundled versus separate caps is one of the most frequent causes of underinsurance. Always ask your insurer or broker to confirm whether each benefit carries its own limit or shares a pool.

Pro Tip: Verify coverage for your specific activities and destination before you travel. If you plan to scuba dive in the Philippines or ski in the Caucasus, confirm in writing that those activities are covered. Do not assume.

How to select the right evacuation and repatriation cover

Choosing the right policy requires matching your cover to your actual risk profile. A weekend city break in Western Europe carries very different risks from a six-month posting in sub-Saharan Africa. Use these criteria to guide your selection:

- Destination risk level. Research local hospital standards and proximity to specialist care. Remote or developing regions require higher evacuation limits.

- Trip duration. Short-term travel insurance suits single trips. Expats and long-term residents need annual international health insurance with built-in evacuation benefits.

- Coverage limits. For destinations outside Europe, aim for evacuation limits of at least $500,000. For intercontinental travel, consider plans with uncapped or very high limits.

- Separate versus combined caps. Prioritise policies that assign independent limits to evacuation, repatriation, and remains transport.

- Pre-existing conditions. Declare all conditions at the point of purchase. Undisclosed conditions are the most common reason claims are denied.

- Visa requirements. The Schengen zone legally requires proof of medical evacuation coverage for visa entry. Check requirements for your destination before purchasing.

- Advance purchase. Buy cover before you depart. Some policies exclude conditions that arise between purchase and travel if bought too close to departure.

For travellers planning international business trips, understanding how evacuation cover fits into broader travel planning is worth reviewing before you finalise your policy.

Unparalleledglobalbenefits offers tailored expat health insurance plans that include evacuation and repatriation benefits suited to a wide range of destinations and trip profiles.

Key takeaways

Medical evacuation and repatriation insurance is the only reliable protection against evacuation costs that routinely reach six figures, and no standard domestic health plan covers it.

| Point | Details |

|---|---|

| Evacuation goes to nearest facility | Insurers transport you to the closest adequate hospital, not necessarily your home country. |

| Pre-authorisation is non-negotiable | Arranging your own evacuation without insurer approval almost always results in a denied claim. |

| Costs reach six figures | Air ambulance flights cost $25,000–$250,000+; remains transport adds $5,000–$15,000 or more. |

| Caps vary by region and tier | European plans typically cap at €50,000–€250,000; US premium plans can reach $1,000,000. |

| Read the fine print on bundling | Combined caps for evacuation, repatriation, and remains can be exhausted by a single event. |

Coert’s view: what most travellers get wrong about evacuation cover

The most persistent misconception I encounter is the belief that evacuation insurance is a “get me home” service. Travellers picture a comfortable flight back to their own hospital, surrounded by familiar faces. The reality is far more clinical. The insurer’s medical team decides where you go, based on where adequate care exists. That might be a hospital in Thailand, not the UK.

The second thing people consistently underestimate is the insurer’s control over the entire process. You cannot call an air ambulance yourself and submit the receipt. The insurer must authorise the transport, arrange it, and pay the provider directly. If you bypass that process, even with the best intentions, you are likely to receive nothing back.

What I find genuinely alarming is how many people rely on standard travel insurance with a £50,000 evacuation cap and assume that is sufficient. For a regional emergency in Europe, it might be. For an ICU flight from Southeast Asia or Latin America, it almost certainly is not. The gap between what people think they are covered for and what they are actually covered for is where financial disasters happen.

My advice is straightforward. Review your evacuation and repatriation limits every time your travel patterns change. If you are moving abroad, switching to a long-term expat plan, or taking on a higher-risk trip, your cover needs to reflect that. Insurance that was adequate for a fortnight in Spain is not adequate for a year in Indonesia.

— Coert

How Unparalleledglobalbenefits can help you get the right cover

Choosing the right medical evacuation and repatriation coverage is easier when you have expert guidance. Unparalleledglobalbenefits specialises in international health and travel insurance for expats, long-term travellers, and families living abroad.

The team at Unparalleledglobalbenefits can help you compare international insurance plans for expats and identify policies with the evacuation and repatriation limits your destination actually requires. Whether you need a single-trip plan or annual expat cover, the right policy is available. Planning a trip for yourself, a resident, or visiting family? UGB + Ekta can arrange travel insurance for seniors up to 100 years old. Just click here: https://ektatraveling.com/?partner_uid=808 and add the promo code “UGB” to receive an additional 10% discount.

For a broader overview of what international cover includes, the international health insurance guide on the Unparalleledglobalbenefits site is a practical starting point.

Watch this short video for more on protecting yourself abroad:

https://youtu.be/bjzvma7Sh1g

FAQ

What is medical evacuation and repatriation insurance?

Medical evacuation and repatriation insurance covers the cost of emergency transport to an adequate medical facility when local care is insufficient, and later, transport home once you are stable. Without it, travellers face costs of $25,000 to $250,000 or more.

Does standard travel insurance include evacuation cover?

Standard domestic health insurance frequently excludes medical evacuation entirely. Some travel insurance policies include a basic evacuation benefit, but the limits are often too low for intercontinental emergencies.

Who decides when a medical evacuation happens?

The insurer’s medical team authorises evacuation based on clinical criteria, not patient preference. They determine whether local care is adequate and, if not, arrange transport to the nearest suitable facility.

Is repatriation the same as medical evacuation?

No. Medical evacuation moves you to the nearest adequate hospital during an acute emergency. Repatriation returns you to your home country once you are medically stable. They are separate benefits and often carry separate coverage caps.

Do I need evacuation cover for Schengen visa travel?

Yes. The Schengen zone legally requires proof of medical coverage, including evacuation, as a condition of visa entry. Policies must meet minimum coverage thresholds to satisfy Schengen visa requirements.

Recommended

- Medical evacuation insurance: protecting your health abroad – Unparalleled Global Benefits

- Complete Guide to Medical Evacuation Insurance Cover – Unparalleled Global Benefits

- Medical Evacuation Coverage: Vital Protection Abroad – Unparalleled Global Benefits

- Travel insurance emergency medical evacuation guide – Unparalleled Global Benefits