Planning your European adventure only to discover your insurance doesn’t meet Schengen visa requirements can derail your entire trip. Many visa applicants face rejection simply because their coverage falls short of mandatory standards or fails to include proper documentation. Understanding the minimum insurance coverage of €30,000 and preparing correct proof ensures your application sails through smoothly. This guide walks you through essential requirements, document preparation, and common pitfalls to avoid when securing insurance for your 2026 Schengen journey.

Table of Contents

- Understanding The Minimum Insurance Requirements For Schengen Visa

- How To Choose The Right Insurance For Your Schengen Visa Application

- Documents And Proof Of Insurance For Schengen Visa Application

- Common Mistakes And How To Avoid Insurance Issues With Your Schengen Visa

- Explore Trusted International Insurance Options For Your Schengen Visa

- FAQ

Key takeaways

| Point | Details |

|---|---|

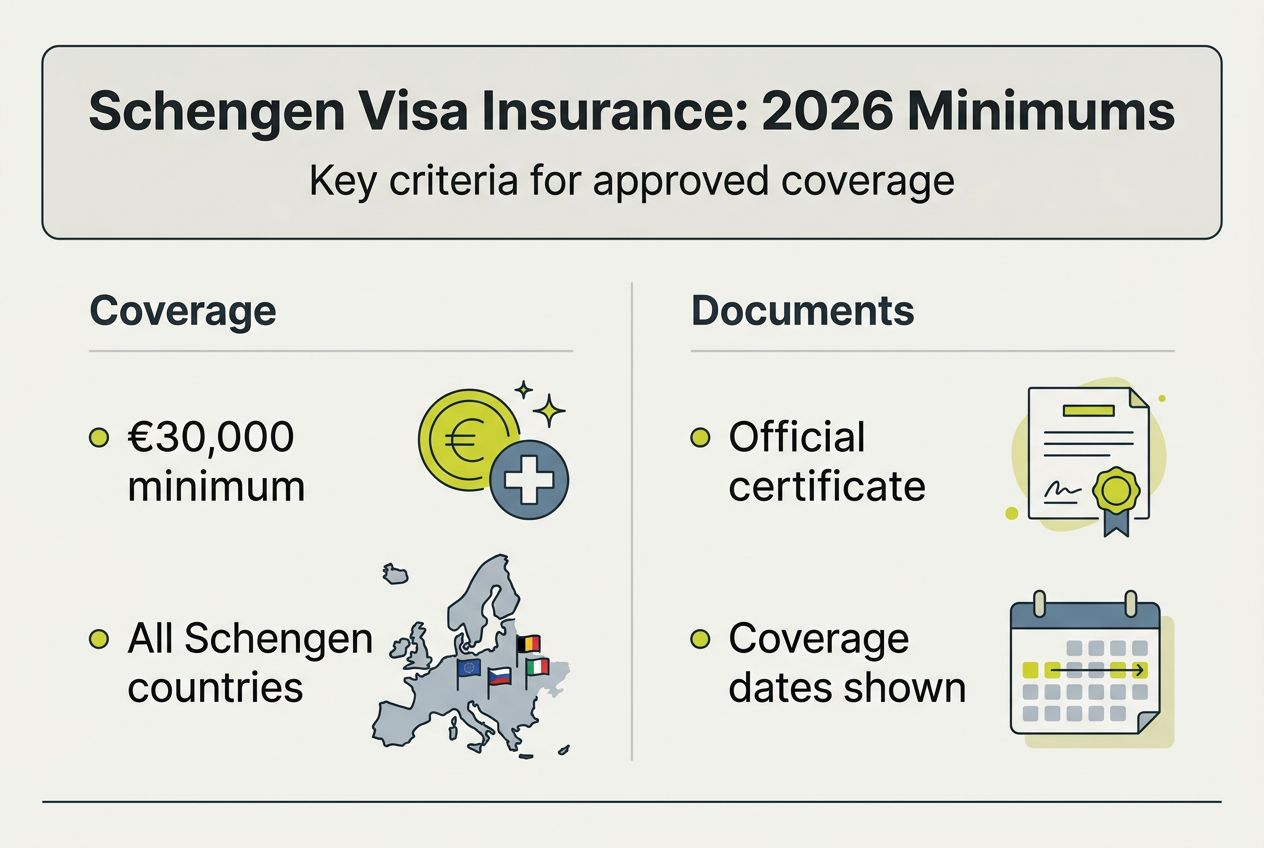

| Mandatory coverage threshold | Schengen visa applications require minimum €30,000 coverage for medical emergencies and repatriation costs |

| Geographic validity matters | Your insurance policy must explicitly cover all Schengen Area member states, not just your primary destination |

| Duration alignment critical | Coverage dates must span your entire stay within the Schengen Area without gaps or early expiration |

| Documentation is non-negotiable | Official insurance certificates showing coverage amount, validity period, and geographic scope must accompany your visa application |

Understanding the minimum insurance requirements for Schengen visa

Securing the right insurance starts with knowing exactly what Schengen authorities demand. The minimum coverage of €30,000 isn’t arbitrary, it reflects the potential costs of emergency medical treatment, hospital stays, and repatriation across European healthcare systems. Your policy must explicitly state it covers these emergency expenses throughout your trip.

Geographic validity extends beyond your primary destination. Even if you’re only visiting France, your insurance must cover all 27 Schengen member states because border-free travel means you could legally move between countries. Policies restricted to single nations or regions will trigger automatic visa refusal, regardless of how comprehensive the coverage appears otherwise.

Timing precision matters enormously for coverage periods. Your insurance must activate on or before your planned entry date and remain valid until your scheduled departure. A policy expiring even one day early creates a coverage gap that consulates cannot overlook. Many applicants mistakenly purchase insurance matching their flight dates rather than their visa validity period, creating unnecessary complications.

Common pitfalls include selecting policies with lower limits like €20,000 or €25,000, assuming these amounts suffice for short trips. Consulates apply the €30,000 minimum universally, regardless of trip duration or activities planned. Another frequent error involves purchasing general travel insurance without verifying it meets specific Schengen criteria, particularly regarding repatriation coverage.

Pro Tip: Request a policy summary document from your insurer explicitly confirming Schengen compliance, coverage amount, and geographic validity before submitting your visa application to eliminate any ambiguity.

How to choose the right insurance for your Schengen visa application

Selecting suitable travel insurance for Schengen visa applications requires balancing mandatory requirements with practical travel needs. Start by filtering options that guarantee €30,000 minimum coverage and Schengen-wide geographic validity, then evaluate additional benefits that enhance your protection and travel experience.

Beyond basic emergency medical coverage, consider policies offering emergency dental treatment, trip cancellation protection, and 24-hour multilingual assistance services. Repatriation coverage becomes crucial if serious illness or injury requires medical evacuation to your home country, potentially costing tens of thousands without proper insurance. Some comprehensive plans include coverage for lost baggage, flight delays, and personal liability, adding valuable peace of mind.

Provider reputation significantly impacts both visa approval and claims experience. Research insurers with established track records serving Schengen visa applicants, checking reviews specifically mentioning smooth documentation processes and responsive emergency assistance. Official recognition by consulates, while not mandatory, indicates the insurer understands visa requirements and provides appropriate documentation formats.

Follow these steps to select optimal insurance:

- Identify your specific needs based on trip duration, activities planned, and any pre-existing medical conditions requiring coverage

- Compare at least three policies meeting minimum Schengen requirements, noting coverage limits, exclusions, and premium costs

- Verify policy documents explicitly mention Schengen Area coverage and provide clear emergency contact information

- Purchase coverage well before your visa appointment to allow time for documentation delivery and any necessary corrections

- Obtain official certificates in formats accepted by your destination country’s consulate, confirming all details match your application

Pro Tip: Create a comparison spreadsheet listing coverage amounts, geographic validity, duration flexibility, and premium costs to quickly identify policies meeting both mandatory requirements and your personal travel needs.

| Feature | Basic Policy | Standard Policy | Premium Policy |

| — | — | — |

| Medical coverage | €30,000 | €50,000 | €100,000 |

| Repatriation included | Yes | Yes | Yes |

| Trip cancellation | No | Up to €2,000 | Up to €5,000 |

| Emergency dental | €500 | €1,000 | €2,500 |

| Personal liability | Not included | €25,000 | €50,000 |

| 24-hour assistance | Phone only | Phone and app | Multilingual concierge |

Documents and proof of insurance for Schengen visa application

Proper documentation transforms your insurance purchase into acceptable visa application proof. Consulates require official insurance certificates or policy documents clearly displaying coverage amount, validity period, and geographic scope. Generic confirmation emails or payment receipts don’t suffice, you need formal certificates issued by your insurance provider.

Your insurance documentation must explicitly state several critical details. The coverage amount should appear as €30,000 minimum or equivalent in another currency with clear conversion rates. Geographic validity must list “Schengen Area” or enumerate all member states covered. Dates must match or exceed your planned travel period, showing both start and end dates without ambiguity. Your personal details including full name and passport number should match your visa application exactly.

Most consulates accept both digital and physical insurance certificates, though submission preferences vary by location. Some require original signed documents, whilst others accept colour photocopies or electronic submissions through visa application portals. Verify your specific consulate’s requirements well before your appointment to avoid last-minute scrambling for alternative formats.

Avoid these common documentation mistakes:

- Submitting insurance quotes or proposals instead of confirmed, paid policy certificates

- Providing documents in languages other than English, French, or the destination country’s official language without certified translations

- Including policies with coverage start dates after your planned entry date or end dates before your scheduled departure

- Presenting certificates missing the insurer’s official stamp, signature, or contact information for verification purposes

Obtain and verify correct documentation by requesting official certificates immediately after purchase, checking every detail against your travel plans and passport information. Contact your insurer’s customer service if any information appears incorrect or incomplete, as corrections typically require several business days. Keep both digital and physical copies accessible throughout your application process and actual travel.

Common mistakes and how to avoid insurance issues with your Schengen visa

Insufficient coverage remains the most frequent error costing applicants time and money. Policies offering €25,000 or less automatically fail Schengen requirements, yet many travellers purchase these cheaper options assuming short trips need less protection. Many Schengen visa refusals stem from inadequate or incorrectly documented insurance, forcing applicants to restart the entire process with proper coverage.

Geographic restrictions create another common pitfall. Some travel insurance policies cover only specific European countries or exclude certain Schengen members, particularly newer additions to the area. Always verify your policy explicitly states “valid for all Schengen Area countries” rather than listing individual nations, which might omit recent members or special territories.

Date mismatches between coverage periods and travel plans cause unnecessary application delays. Applicants frequently purchase insurance matching their flight bookings rather than their visa validity dates, creating gaps if travel plans change or consulates grant longer validity periods. Your insurance should ideally cover a slightly longer period than your maximum possible stay to accommodate unexpected delays.

Confusing general travel insurance with Schengen-compliant policies leads many applicants astray. Standard travel insurance might offer medical coverage but lack specific repatriation provisions or fail to meet the €30,000 minimum threshold. Similarly, domestic health insurance rarely extends to international travel with the coverage levels and geographic scope Schengen visas demand.

Proper insurance documentation isn’t just a bureaucratic formality, it’s your financial safety net against potentially devastating medical costs abroad and the single most controllable factor in visa approval success.

Pro Tip: Schedule a final insurance verification call with your provider two weeks before your visa appointment, confirming coverage amounts, dates, and geographic validity whilst requesting duplicate certificates as backup documentation.

Quickly verify compliance by checking these essential elements:

- Policy certificate shows minimum €30,000 coverage for emergency medical expenses and repatriation

- Geographic validity explicitly includes all Schengen Area member states without exclusions

- Coverage dates span your entire planned stay with buffer days before entry and after departure

- Documentation includes insurer contact details, policy number, and official stamps or signatures

- Personal information matches your passport and visa application exactly, including name spelling and passport number

Explore trusted international insurance options for your Schengen visa

Navigating insurance requirements becomes significantly easier with expert guidance and verified provider options. Our platform features comprehensive international health insurance comparisons specifically designed for Schengen visa applicants, helping you identify compliant policies matching your travel needs and budget constraints.

We’ve partnered with top insurers recognised by European consulates for their reliable coverage and streamlined documentation processes. These providers understand Schengen requirements intimately, offering policies that guarantee visa compliance whilst delivering responsive emergency assistance throughout your European journey. Detailed plan comparisons highlight coverage levels, premium costs, and additional benefits, enabling informed decisions without overwhelming research.

Exploring travel insurance for Schengen visa options early prevents last-minute complications that could delay your application. Our resources include step-by-step guidance on documentation requirements, provider reputation insights, and direct quote requests tailored to your specific travel dates and destinations.

Key advantages of using our insurance services:

- Pre-verified Schengen-compliant policies eliminating guesswork about coverage adequacy

- Side-by-side comparisons showing exactly how different plans meet visa requirements

- Expert support helping you understand policy details and documentation needs

- Direct access to recognised insurers with proven track records for visa applications

Pro Tip: Begin your insurance search at least four weeks before your visa appointment to allow ample time for policy selection, purchase, documentation delivery, and any necessary corrections without rushing.

FAQ

What is the minimum insurance coverage amount for a Schengen visa?

The minimum required coverage is €30,000 for emergency medical expenses and repatriation costs. This threshold applies universally across all Schengen member states regardless of your trip duration or primary destination. The policy must remain valid throughout your entire stay within the Schengen Area.

Does the insurance need to cover all Schengen countries or only the country I am visiting?

Your insurance must cover all 27 Schengen Area member states, not just your primary destination. Border-free travel within the Schengen zone means you can legally move between countries, so consulates require comprehensive geographic coverage. Policies restricted to individual nations will result in visa refusal.

How can I prove my insurance meets Schengen visa requirements?

You must provide an official insurance certificate or policy document clearly showing coverage amount, validity duration, and Schengen-wide geographic scope. The documentation should include your personal details matching your passport, the insurer’s contact information, and official stamps or signatures. Check your specific consulate’s requirements for acceptable formats, as some prefer original documents whilst others accept certified copies or digital submissions.

Can travel insurance with less than €30,000 coverage be accepted for a Schengen visa?

No, insurance coverage below €30,000 does not meet mandatory Schengen visa requirements and will result in application refusal. Consulates apply this minimum threshold uniformly without exceptions for short trips or low-risk travel. You must purchase compliant insurance meeting or exceeding €30,000 coverage to proceed with your visa application.

When should I purchase insurance for my Schengen visa application?

Purchase insurance at least three to four weeks before your visa appointment to allow time for policy processing, certificate delivery, and verification of all details. Early purchase also provides flexibility to correct any documentation errors without delaying your application. Ensure your coverage dates align with your planned travel period, ideally with buffer days before entry and after departure.

Recommended

- Insurance Requirements for Schengen Visa: A Step-by-Step Guide – Unparalleled Global Benefits

- Travel Insurance for Schengen Visa: Get Approved Easily – Unparalleled Global Benefits

- Visa Travel Insurance: Why It Matters For Visa Holders – Unparalleled Global Benefits

- Seguro De Viaje Para Visa Schengen: Guía Completa – Unparalleled Global Benefits

- Peaks of the Balkans – Border Permits Guide