TL;DR:

- Trip protection, or travel insurance, safeguards your nonrefundable trip costs against cancellations, delays, medical emergencies, and baggage issues abroad. Purchasing coverage early and matching it to your trip’s expenses and destination risks maximizes protection, especially with optional CFAR upgrades for added flexibility. Proper documentation and understanding policy exclusions are essential for successful claims and comprehensive travel safety.

Trip protection is the insurance coverage designed to safeguard your prepaid, nonrefundable trip costs against cancellations, interruptions, delays, and medical emergencies abroad. It goes by several names in the industry, with “travel insurance” being the standard term used by providers such as Allianz, Aviva, and AAA. Whether you are booking a single trip to Southeast Asia or planning a multi-leg European tour, understanding what trip protection covers, and what it does not, is the difference between recovering your losses and absorbing them entirely.

What does trip protection cover and how does it work?

Trip protection, or travel insurance, is built around five core coverage areas. Each one addresses a specific category of financial risk that travellers face before and during a journey.

-

Trip cancellation and interruption. Cancellation and interruption coverage reimburses eligible nonrefundable costs if you must cancel before departure or cut your trip short due to a covered emergency such as sudden illness, a family bereavement, or a natural disaster. This is the most commonly claimed benefit and the one most travellers think of first.

-

Travel delays. Delay coverage activates after a waiting period, typically between 3 and 12 hours, and reimburses reasonable costs for meals, lodging, and ground transport. That waiting period matters because a one-hour delay at Heathrow will not trigger a claim, but an overnight delay in Bangkok almost certainly will.

-

Baggage loss and delay. Baggage delay coverage activates after your bags have been missing for 12 to 24 hours, allowing you to purchase essentials. Permanent loss is typically declared after 14 to 21 days, following the airline’s own search timeline. A quality luggage tag set can help reunite you with your bags faster, but insurance covers the financial gap when it does not.

-

Medical emergencies overseas. Medical cover pays for hospital stays, treatment, and specialist consultations abroad. More critically, emergency evacuation reimburses transport to a better-equipped facility or back to your home country, costs that can exceed £80,000. For remote destinations with limited medical infrastructure, this benefit alone justifies the policy cost.

-

Repatriation of remains. Some policies include repatriation cover for fatalities abroad, handling complex international legal and logistical arrangements that families would otherwise face alone.

Common exclusions include high-risk or extreme sports activities, pre-existing medical conditions unless declared and accepted, and events related to war or civil unrest. Reading the exclusions section of any policy is not optional. It is where most claim disputes originate.

| Coverage type | What it pays for |

|---|---|

| Trip cancellation | Nonrefundable deposits and prepaid costs for covered reasons |

| Travel delay | Meals, accommodation, and transport after qualifying wait period |

| Baggage loss | Replacement value of permanently lost items after carrier search |

| Medical emergency | Hospital treatment, specialist care, and evacuation costs abroad |

| Repatriation | Return of remains and associated legal costs |

Pro Tip: Always check whether your policy covers the specific activities you plan to do. Scuba diving, skiing, and trekking above certain altitudes are routinely excluded from standard plans and require an adventure sports add-on.

What is Cancel For Any Reason trip protection?

Cancel For Any Reason, widely known as CFAR, is an optional upgrade to standard travel insurance that allows you to cancel your trip for reasons not listed in the base policy and still receive partial reimbursement. Standard travel insurance covers cancellations only for specified unforeseen reasons such as death, serious illness, or sudden job loss. CFAR removes that restriction entirely.

The trade-off is cost and timing. CFAR must typically be purchased within 10 to 21 days of your first trip payment, and you must cancel at least 48 hours before departure to qualify for a payout. Miss either window and the upgrade is worthless. This is the single most common mistake travellers make with CFAR.

The reimbursement rate is partial, not full. Most CFAR plans pay back 50% to 75% of nonrefundable prepaid costs, with select plans reaching 80%. On a £15,000 trip, that means recovering between £7,500 and £12,000, not the full amount. That is still a meaningful financial cushion, but it is not a complete safety net.

The cost premium is real. CFAR increases travel insurance premiums by 40% to over 100% compared to a standard policy. On a £20,000 trip where standard insurance costs roughly £1,000, adding CFAR can push that figure to £1,500 or more. Many travellers underestimate this cost until they see the quote.

- CFAR is particularly valuable when travelling to politically unstable regions where standard exclusions for civil unrest would otherwise leave you unprotected.

- It suits travellers with health concerns that may not yet qualify as a formal pre-existing condition but could realistically cause a cancellation.

- It is worth considering for expensive, complex itineraries with multiple nonrefundable components, such as safari packages or cruise bookings.

- It is less useful for budget trips where the cost of the upgrade approaches the value of what you are protecting.

Pro Tip: Buy your travel insurance, including any CFAR upgrade, on the same day you make your first trip payment. This locks in the widest possible eligibility window and protects you from any events that become “known” after purchase.

For a deeper look at CFAR options available in 2026, the CFAR trip insurance guide from Unparalleledglobalbenefits covers current plan structures in detail.

How to choose travel insurance for your trip

Choosing the right travel insurance starts with an honest assessment of your trip’s financial exposure and your personal risk tolerance. There is no single best policy for every traveller, but there is a clear process for finding the right one for you.

Single trip vs annual cover. If you travel once or twice a year, single trip travel insurance is usually the more cost-effective choice. Annual multi-trip policies make financial sense if you take four or more trips per year, as the per-trip cost drops significantly. For long trips lasting several weeks or months, check the maximum trip duration allowed under any annual policy, as many cap individual trips at 31 or 45 days.

Destination-specific risks. Medical infrastructure varies enormously by country. Travelling to the United States without medical insurance for holidays is a serious financial risk, given that a single hospitalisation can cost tens of thousands of pounds. Travelling to rural parts of sub-Saharan Africa or Southeast Asia raises evacuation risk. Your destination should directly influence the level of medical and evacuation cover you select.

Non-refundable costs. Add up every prepaid, nonrefundable expense: flights, hotels, tours, cruise deposits, and event tickets. This total is your financial exposure. Your cancellation cover limit should match or exceed this figure. Underinsuring your trip costs is a common and avoidable error.

- Compare policies using aggregator platforms that show side-by-side exclusions, not just headline prices.

- Check whether pre-existing medical conditions are covered, excluded, or available as a declared add-on.

- Confirm that the policy covers your planned activities, particularly if you intend to hire a vehicle, participate in water sports, or trek at altitude.

- Review the claims process before you buy. A policy with a 24-hour emergency assistance line is worth more than a cheaper policy with a postal claims process.

Buying standard policies before departure is a hard requirement for all providers. Waiting until the day before travel limits your options and may exclude coverage for events already in the news. Timing is not a minor detail. It determines your eligibility for the most valuable benefits.

Travellers with specific health needs will find the travel insurance for health conditions guide from Unparalleledglobalbenefits a useful starting point for understanding declared condition policies.

What to do when your trip is interrupted or delayed

When a disruption occurs, the steps you take in the first few hours directly affect whether your claim succeeds or fails.

-

Contact your insurer’s assistance line immediately. Most policies require you to notify the insurer before incurring significant expenses such as a new flight or hotel booking. Booking first and claiming later is a common mistake that leads to partial or full claim rejection.

-

Obtain written confirmation of the delay or cancellation cause. Airlines issue delay certificates at the gate or customer service desk. Hotels provide written confirmation of early checkout. Without these documents, your insurer has no independent proof of the event.

-

Keep every receipt. Documentation requirements include prepaid booking receipts, cancellation notices, and all new expense receipts incurred during the disruption. Missing documentation is one of the most common reasons claims are denied, particularly for CFAR policies where the burden of proof is higher.

-

Record the timeline precisely. Note the time your delay began, when you were notified, and when you incurred each expense. This timeline supports your claim and confirms you met the policy’s waiting period threshold.

-

Submit your claim promptly. Most policies set a claims submission deadline of 30 to 90 days after the event. Missing this window can void an otherwise valid claim entirely.

Pro Tip: Create a dedicated folder on your phone, using an app like Google Drive or Dropbox, where you store photos of all booking confirmations, receipts, and delay certificates as you travel. This takes seconds and removes the single biggest obstacle to a successful claim.

Standard travel insurance protects against many significant issues like medical emergencies and delays even without CFAR, which reinforces its core value for travellers who find CFAR too costly.

Key takeaways

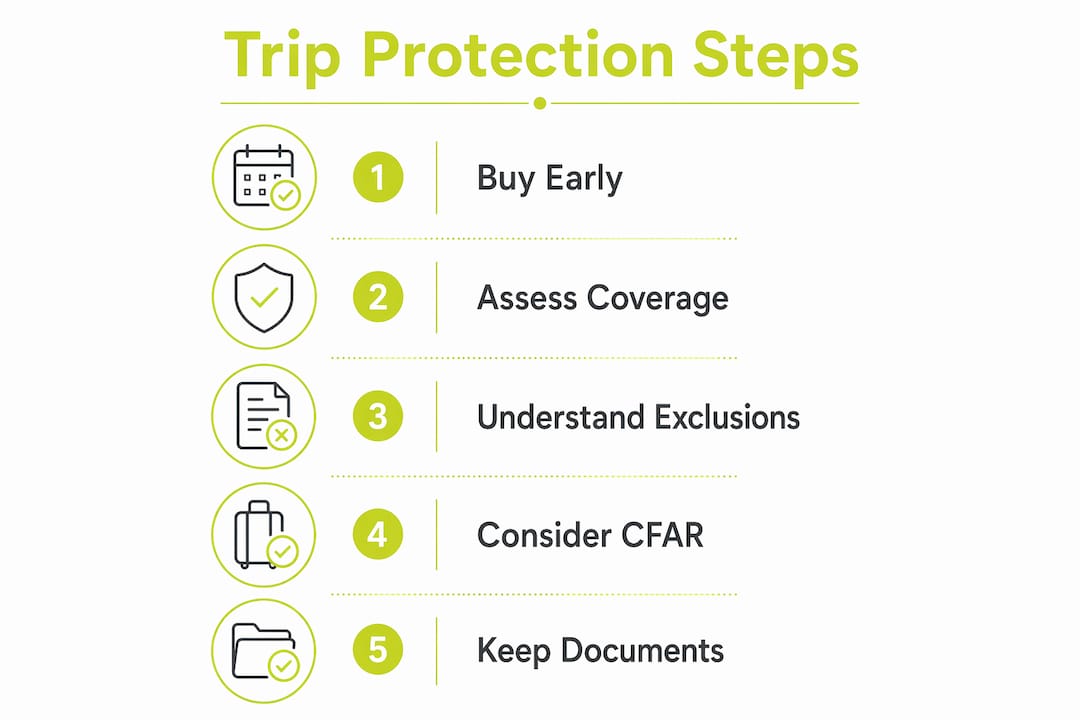

Trip protection works best when purchased early, matched to your actual nonrefundable costs, and chosen with your destination’s specific medical and safety risks in mind.

| Point | Details |

|---|---|

| Buy early | Purchase cover on the day of your first trip payment to maximise eligibility windows. |

| Match cover to costs | Your cancellation limit should equal your total nonrefundable trip expenditure. |

| CFAR has strict rules | You must buy within 10 to 21 days of first payment and cancel 48 hours before departure. |

| Medical cover is non-negotiable | Evacuation costs can exceed £80,000; always include medical and evacuation cover. |

| Documentation wins claims | Keep all receipts, delay certificates, and booking confirmations in one accessible place. |

Why I think most travellers get trip protection backwards

Most people treat travel insurance as the last item on their pre-trip checklist, something to sort out the night before departure. In my experience, that approach costs travellers money and options in equal measure. The most valuable benefits, particularly CFAR and time-sensitive medical cover for pre-existing conditions, are only available within days of your first booking. By the time you remember to buy, the window has often closed.

The other mistake I see repeatedly is insuring the wrong thing. Travellers focus on the headline cancellation benefit and ignore the medical and evacuation cover, which is where the genuinely catastrophic financial exposure sits. A cancelled holiday costs you hundreds or thousands of pounds. A medical evacuation from a remote location costs tens of thousands. The priority should reflect the magnitude of the risk, not the likelihood of it.

CFAR is genuinely useful, but it is not for everyone. If your trip costs less than £3,000 and you have reasonable flexibility, the premium increase rarely justifies the partial reimbursement. For complex, expensive itineraries with multiple nonrefundable components, it is worth every penny. The key is matching the product to the actual risk profile of your specific trip, not buying the most expensive policy because it feels safer.

Technology has made comparison far easier. Platforms that display policy exclusions side by side, rather than just premiums, have changed how informed travellers shop. Use them. The cheapest policy is rarely the right one, but the most expensive policy is not automatically the best either.

— Coert

How Unparalleledglobalbenefits can protect your next trip

Unparalleledglobalbenefits specialises in international insurance solutions tailored to individual travellers, expats, and families. Whether you need single trip cover for a two-week holiday or a more complex policy covering medical conditions and extended stays, the team can match you with a plan that fits your actual itinerary and risk profile. For a clear overview of how travel insurance works and what to look for, the travel insurance basics guide is a strong starting point.

Planning a trip for yourself, a resident, or visiting family? UGB + Ekta can arrange travel insurance for seniors up to 100 years old. Just click here: https://ektatraveling.com/?partner_uid=808 and add the promo code “UGB” to receive an additional 10% discount.

For a helpful overview of trip protection options, watch this short video:

https://youtu.be/bjzvma7Sh1g

FAQ

What is trip protection in travel insurance?

Trip protection is the collective term for travel insurance benefits that cover financial losses from cancellations, interruptions, delays, baggage issues, and medical emergencies. It protects the nonrefundable costs you have already paid for your trip.

When should I buy trip protection?

Buy trip protection on the same day you make your first trip payment. This maximises your eligibility for time-sensitive benefits like CFAR and pre-existing condition waivers, which typically require purchase within 10 to 21 days of the initial booking.

Does basic travel insurance cover medical emergencies abroad?

Yes. Standard travel insurance includes medical emergency cover and, in most cases, emergency evacuation. Evacuation costs can exceed £80,000 for remote destinations, making medical cover one of the most financially critical components of any policy.

What is the difference between trip cancellation and CFAR cover?

Standard trip cancellation cover reimburses nonrefundable costs only for specified reasons such as illness, bereavement, or job loss. CFAR allows you to cancel for any reason and typically reimburses 50% to 75% of prepaid costs, at a premium increase of 40% to over 100%.

What travel insurance do I need for a long trip?

For long trips, prioritise high medical and evacuation limits, cover for the full trip duration, and baggage protection. Check that any annual policy allows trips of the length you are planning, as many cap individual journeys at 31 or 45 days.

Recommended

- Multi-country travel insurance: your 2026 guide – Unparalleled Global Benefits

- Trip Cancellation Insurance Guide 2025: Essential Info for Global Travellers – Unparalleled Global Benefits

- Family multi trip travel insurance: your 2026 guide – Unparalleled Global Benefits

- Choosing travel insurance: expert guidance for global trips – Unparalleled Global Benefits