TL;DR:

- Group medical coverage for tours offers collective emergency health and evacuation protection, replacing individual policies with a single comprehensive plan. It typically includes emergency treatment, hospitalization, and evacuation, with comprehensive plans providing broader benefits than basic ones. Prioritizing evacuation coverage is crucial, as costs can exceed $50,000, and foreign hospitals may require upfront payment, making it the most vital benefit for responsible travel planning.

Group medical coverage for tours is the specialised insurance that provides collective emergency health and evacuation protection to every member of an organised travel group, replacing the patchwork of individual policies with one consistent plan. The industry term for this protection is group travel medical insurance, and it covers emergency treatment, hospitalisation, and medical evacuation for all enrolled participants during the travel period. Without it, a single medical crisis abroad can cost one traveller more than $50,000 in evacuation fees alone, according to U.S. Embassy guidance. For tour organisers and participants alike, securing the right group medical coverage before departure is not optional. It is the foundation of responsible travel planning.

What does group medical insurance for tours typically cover?

Group travel medical insurance commonly includes emergency medical treatment, physician visits, hospitalisation, and emergency medical evacuation during the travel period. Coverage is temporary, aligned with your travel dates, and is structured to address the specific risks of being far from home rather than providing long-term health management. That distinction matters: you are buying protection for acute events, not routine care.

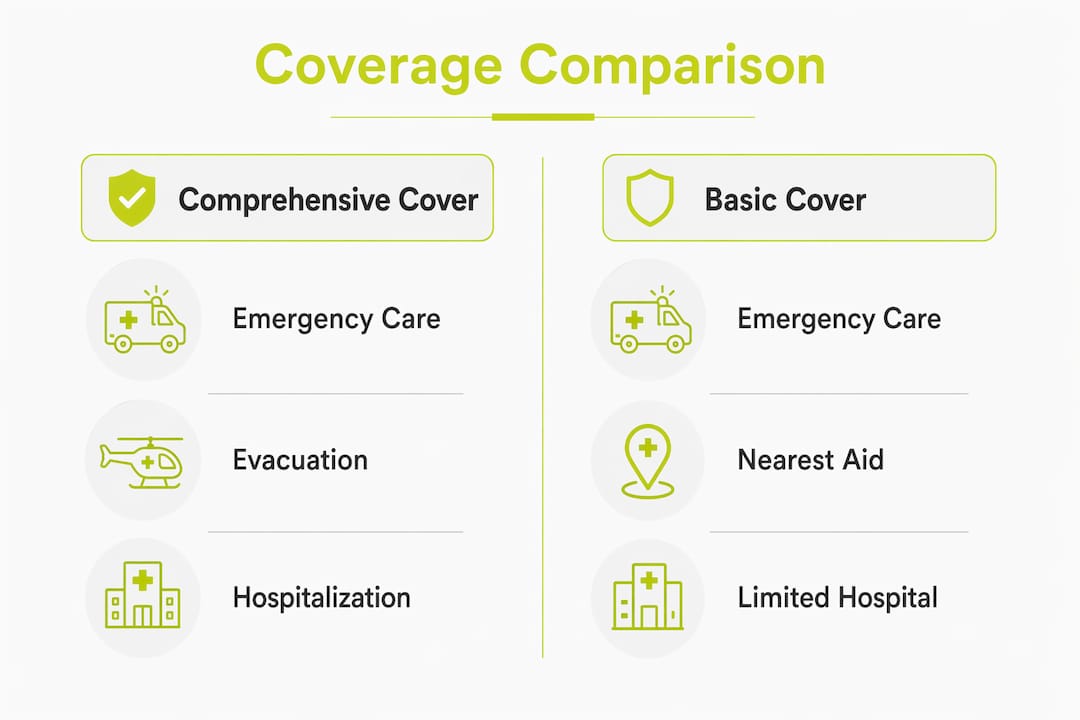

Most group policies divide their benefits into two tiers. Comprehensive plans include emergency medical treatment, diagnostic tests, prescription medicines, hospital stays, emergency dental, and full medical evacuation with repatriation. Basic plans cover emergency treatment and evacuation only, with lower benefit limits and higher out-of-pocket costs. The table below shows how these two levels compare across the most critical benefit categories.

| Benefit | Comprehensive cover | Basic cover |

|---|---|---|

| Emergency medical treatment | Included, high limits | Included, lower limits |

| Hospitalisation | Included | Included |

| Physician visits and diagnostics | Included | Limited or excluded |

| Emergency medical evacuation | Included, direct billing | Included, reimbursement only |

| Trip interruption | Often included | Rarely included |

| Pre-existing condition cover | Available with waiver | Usually excluded |

The right level depends on your destination, the age profile of your group, and the activities planned. A tour to a remote region of South America or Southeast Asia warrants comprehensive cover; a short city tour in Western Europe with younger travellers may suit a basic plan if local hospital infrastructure is strong.

Pro Tip: Always read the evacuation clause before purchasing. Some basic policies only cover transport to the nearest adequate facility, not repatriation to your home country. For most tour groups, home-country repatriation is the benefit that matters most in a genuine crisis.

How does group cover differ from individual travel insurance?

Individual travel insurance requires each participant to research, purchase, and manage their own policy. Across a group of 20 or 30 people, that creates 20 or 30 different benefit levels, 20 or 30 different insurers to contact in an emergency, and a high probability that at least one traveller will arrive underinsured or uninsured. Standardised group plans eliminate that confusion by giving every enrolled participant identical benefits and a single point of contact for emergency coordination.

The practical advantages of a group plan go beyond administration. Consider these key differences:

- Consistent emergency procedures. When every traveller is on the same plan, the tour leader and the insurer follow one protocol. There is no delay caused by identifying which of several insurers to call first.

- Reduced coverage gaps. Individual purchasers often choose the cheapest option, which may exclude evacuation or have low medical limits. A group plan sets a floor that applies to everyone.

- Simplified enrolment. Group travel medical plans typically require minimal underwriting and quick setup, which is particularly useful when finalising a tour roster close to departure.

- Cost efficiency. Group rates are often more competitive per person than equivalent individual policies, particularly for larger groups where the insurer spreads risk across many participants.

The main challenge with group plans arises when travellers have different trip lengths, ages, or health profiles. A 65-year-old with a pre-existing heart condition and a 28-year-old in full health have very different risk profiles. Some insurers address this through hybrid approaches, where a core group plan covers the majority of participants and supplemental individual riders address specific needs. If your group includes travellers with significant pre-existing conditions, confirm whether the group plan offers a pre-existing condition waiver and what the eligibility criteria are.

Pro Tip: Collect a full roster with dates of birth, travel dates, and destination details before requesting quotes. Sharing this information upfront with an insurer or broker like Unparalleledglobalbenefits means you receive accurate pricing rather than a generic estimate that changes at enrolment.

Why is emergency medical evacuation central to tour group coverage?

Medical evacuation is the single benefit that separates adequate group coverage from genuinely protective coverage. Evacuation costs can exceed $50,000, and foreign hospitals frequently require cash payment upfront before treatment begins. Without evacuation cover, a group member who suffers a serious injury in a remote location faces a financial crisis on top of a medical one.

Local infrastructure is the variable most tour organisers underestimate. A hospital in a major European city may provide excellent care. A clinic in a rural area of Central America or a small island in the Pacific may not have the equipment or specialists needed for a serious cardiac event, a spinal injury, or a complicated surgical case. In those situations, evacuation to an appropriate facility is not a luxury. It is the difference between a manageable disruption and a life-threatening delay.

“Coordinating transport to an appropriate facility can be the difference between a manageable disruption and a major crisis.” — Diversified Quotes, Travel Medical Insurance for Large Groups

When reviewing evacuation provisions in any group policy, check for the following:

- Whether the policy covers evacuation to the nearest adequate facility or to the traveller’s home country

- Whether the insurer operates a 24-hour emergency assistance line with multilingual support

- Whether direct billing is available so the traveller does not pay out of pocket and seek reimbursement later

- Whether the policy covers a medical escort if the traveller cannot travel unaccompanied

For a deeper understanding of how evacuation cover works in practice, the Unparalleledglobalbenefits guide on medical evacuation insurance explains the key provisions and what to look for when comparing plans.

How to select the right group medical coverage for your tour

Choosing the right plan follows a clear sequence. Work through these steps before contacting any insurer or broker.

-

Gather your group data. Collect the full roster including names, dates of birth, nationalities, travel dates, and destinations. Sharing size, destination, dates, and ages with a broker upfront helps identify plans that match your group’s logistics and avoids coverage gaps at enrolment.

-

Define your coverage priorities. Decide whether you need comprehensive cover or whether a medical-and-evacuation-only plan is sufficient. Factor in planned activities. Adventure tours involving hiking, water sports, or high-altitude trekking often require specific activity riders that standard plans exclude.

-

Compare plans using a structured framework. Use the table below to evaluate any plan you are considering against the most critical criteria.

| Selection criterion | What to verify |

|---|---|

| Medical benefit limit | Minimum $250,000 recommended for most international destinations |

| Evacuation benefit | Confirm home-country repatriation, not just nearest facility |

| Pre-existing conditions | Check waiver availability and look-back period |

| Activity inclusions | Confirm planned activities are not excluded |

| 24-hour assistance | Verify multilingual emergency line and direct billing |

| Enrolment timeline | Confirm how quickly coverage can be activated |

-

Assess pre-existing condition rules. Many domestic health plans provide no coverage outside the traveller’s home country, including Medicare for U.S. citizens. Travellers who rely on domestic cover abroad will find themselves unprotected. Confirm that your group plan either covers pre-existing conditions or that affected travellers have supplemental cover in place.

-

Verify insurer support for group administration. A good group insurer provides enrolment assistance, clear documentation for each participant, and a dedicated emergency coordination line. Ask specifically how the insurer handles a multi-person emergency, such as a road accident involving several group members simultaneously.

-

Communicate the plan to every participant. Once coverage is confirmed, share the policy number, the emergency assistance number, and the claims process with every group member in writing before departure.

Pro Tip: Use the travel medical coverage checklist from Unparalleledglobalbenefits to verify that no critical benefit has been overlooked before you finalise any group policy.

Key takeaways

Effective group medical coverage for tours requires evacuation cover, standardised benefits for all participants, and verified insurer support before departure.

| Point | Details |

|---|---|

| Evacuation cover is non-negotiable | Medical evacuation can exceed $50,000; confirm home-country repatriation is included. |

| Group plans reduce coverage gaps | Standardised benefits replace the inconsistency of individual purchases across a large roster. |

| Domestic insurance does not apply abroad | Most home-country health plans, including Medicare, provide no overseas cover. |

| Collect full roster data first | Ages, destinations, and travel dates determine accurate pricing and eligibility. |

| Verify activity inclusions | Adventure activities often require specific riders that standard group plans exclude. |

Why evacuation is the benefit most organisers overlook

I have reviewed hundreds of group travel insurance enquiries over the years, and the pattern is consistent. Tour organisers focus on the medical treatment benefit and treat evacuation as a secondary consideration. That is the wrong priority order.

Medical treatment abroad is expensive, but it is finite. A hospital stay, even a serious one, has a calculable cost. Evacuation is where costs become genuinely unpredictable. A medical flight from a remote location in Southeast Asia or Latin America, with a medical escort and specialist equipment, can cost more than the entire tour budget for a mid-sized group. And it happens faster than anyone expects.

The other misunderstanding I see regularly is the assumption that domestic health insurance provides some level of overseas protection. It almost never does. The U.S. Embassy is explicit on this point: Medicare does not cover overseas medical costs, and most private domestic plans offer no meaningful international benefit. Travellers who discover this after a medical event abroad face both a health crisis and a financial one simultaneously.

My practical advice for any tour organiser is this: treat the evacuation benefit as your primary selection criterion, not an add-on. Once you have confirmed that evacuation cover is adequate, work backwards through the other benefits. That approach consistently produces better outcomes than starting with price and hoping evacuation is included.

Proactive planning also means communicating the policy details to every group member before departure. A laminated card with the emergency assistance number and policy reference, distributed to each participant, has resolved situations that would otherwise have been chaotic. It costs nothing and can make an enormous difference.

— Coert

How Unparalleledglobalbenefits can help you secure group cover

Planning group medical coverage for a tour abroad does not need to be complicated, but it does require the right guidance and the right insurer match for your specific group profile.

Unparalleledglobalbenefits specialises in international insurance solutions for travellers, expats, and groups of all sizes. Whether you are organising a cultural tour, an adventure expedition, or a family group trip, the team can help you compare plans, verify evacuation provisions, and match coverage to your roster’s specific needs. Start with the international health insurance guide for a thorough overview of your options, or explore the travel health insurance guide for practical next steps. Contact Unparalleledglobalbenefits directly for a personalised group quote.

Planning a trip for yourself, a resident, or visiting family? UGB + Ekta can arrange travel insurance for seniors up to 100 years old. Just click here: https://ektatraveling.com/?partner_uid=808 and add the promo code “UGB” to receive an additional 10% discount.

For a helpful overview of group travel medical insurance, watch this short video:

https://youtu.be/bjzvma7Sh1g

FAQ

What does group medical coverage for tours include?

Group medical coverage for tours typically includes emergency medical treatment, hospitalisation, physician visits, diagnostic tests, and emergency medical evacuation for all enrolled participants during the travel period. Comprehensive plans may also cover trip interruption and pre-existing conditions with an approved waiver.

Does domestic health insurance cover travellers abroad?

Most domestic health plans, including Medicare for U.S. citizens, provide no coverage overseas. Travellers must purchase dedicated international or travel medical insurance before departure to avoid paying out of pocket for treatment abroad.

How much does medical evacuation cost without insurance?

Medical evacuation abroad can cost over $50,000, and foreign hospitals often require upfront cash payment before treatment begins. Evacuation cover is the most critical benefit in any group travel medical plan.

How is group travel medical insurance different from individual policies?

Group plans provide standardised benefits to all participants, simplify emergency coordination, and reduce the coverage gaps that occur when individuals purchase their own policies separately. Standardised group cover also improves communication and ensures consistent emergency procedures across the entire tour group.

What information do I need to get a group travel insurance quote?

You need the full group roster including dates of birth, travel dates, destination countries, and group size. Sharing these details upfront with a broker allows accurate pricing and helps identify plans that match your group’s specific logistics and risk profile.

Recommended

- What does travel health insurance cover: your 2026 guide – Unparalleled Global Benefits

- Multi-country travel insurance: your 2026 guide – Unparalleled Global Benefits

- Family multi trip travel insurance: your 2026 guide – Unparalleled Global Benefits

- Navigate medical coverage abroad confidently in 2026 – Unparalleled Global Benefits