TL;DR:

- Moving abroad without proper medical insurance exposes you to significant financial risk and potential devastating bills.

- Thorough plan comparison requires understanding your health needs, evaluating total costs, coverage features, provider networks, and exclusions before enrolling.

Moving abroad or travelling long-term without the right medical insurance is one of the most financially exposed positions you can put yourself in. Knowing how to compare medical insurance plans before you commit can mean the difference between full coverage and a bill that runs into tens of thousands. The challenge is that international plans vary wildly in cost, coverage scope, exclusions, and provider networks. This guide walks you through the exact process of health cover comparison, from gathering the right information to verifying your final choice with confidence.

Table of Contents

- Key takeaways

- What to gather before you compare medical insurance plans

- Comparing costs effectively: beyond the monthly premium

- Evaluating coverage features for international travellers

- Common pitfalls when comparing medical plans

- Final steps: verifying and enrolling with confidence

- My honest take on international insurance comparison

- Find the right plan with Unparalleledglobalbenefits

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Look beyond the premium | Total annual cost including deductibles and copays matters far more than the monthly figure alone. |

| Verify provider networks first | Confirm your preferred doctors and hospitals are covered before enrolling in any plan. |

| Pre-existing conditions vary widely | Waiting periods for pre-existing conditions range from three to four years depending on the insurer. |

| Age drives international costs | Visitor medical insurance costs rise sharply with age, so factor this into your budget early. |

| Use independent brokers | Commission-driven comparison sites may omit the best-value policies from their results. |

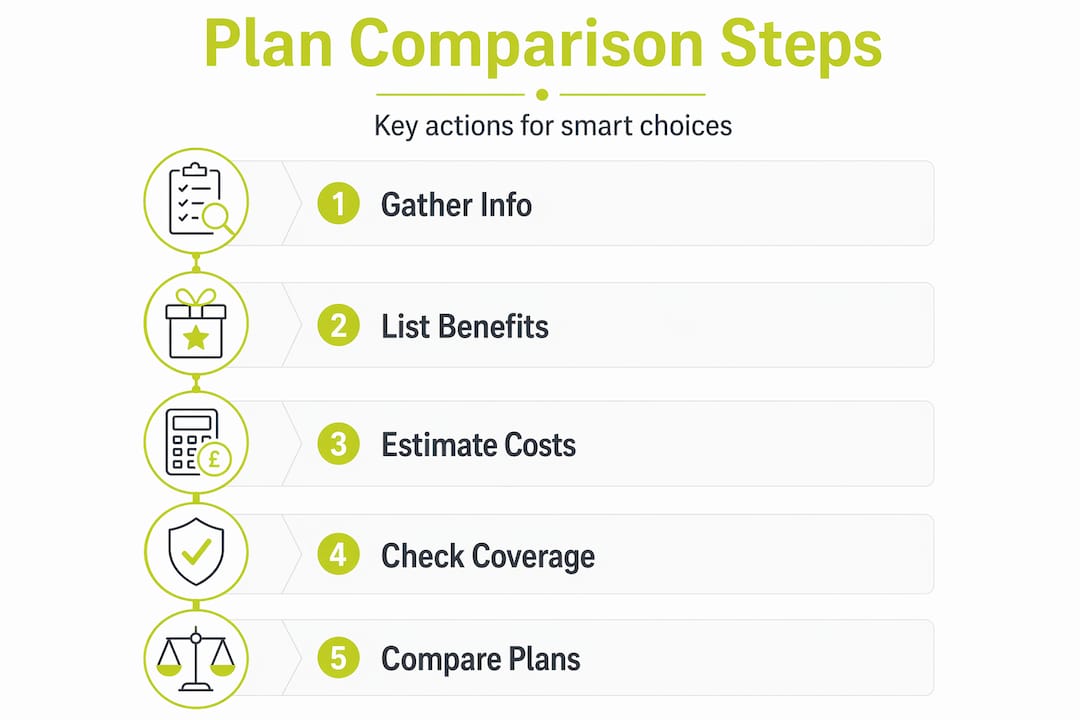

What to gather before you compare medical insurance plans

Before you open a single comparison tool or request a quote, you need two things: a clear picture of your personal health situation and a solid understanding of the plan types available to you. Without these, you are comparing apples with oranges and guessing at what you actually need.

Start with your personal profile. Your age, existing health conditions, how frequently you travel, and where you are going all change the maths significantly. Visitor medical insurance costs vary drastically with age, running from roughly $50 to $120 per month for those aged 20 to 40, but jumping to $180 to $450 per month for those aged 60 to 80. If you are in the older bracket, this is not a minor line item. It is the foundation of your entire budget for cover abroad.

Next, understand the plan categories you are choosing between. The three most relevant for international living and travel are:

- Travel insurance: Short-term cover, typically for trips under 180 days. Protects against trip interruption, emergency medical costs, and evacuation.

- Visitor insurance: Designed for people visiting a country on a temporary visa. Useful for family members joining you abroad or individuals on visitor visas.

- International health insurance: Long-term, comprehensive cover for expats and long-stay travellers. Often includes routine care, specialist visits, and preventive benefits.

Understanding which category fits your situation is the starting point for any meaningful health cover comparison. Reading about the key differences abroad between travel medical and health insurance can help clarify this.

Once you know your plan type, gather the specific details for each policy you are evaluating: the monthly premium, annual deductible, copayment amounts, out-of-pocket maximum, coverage limits per condition or per year, the provider network, and a full list of exclusions. Also compile your own documentation: a list of your current medications, names of any doctors you want to continue seeing, and any upcoming planned procedures.

Pro Tip: When sourcing plan information, go directly to the insurer’s website or request a full policy document. Summary brochures and third-party comparison sites often omit critical detail on sub-limits and exclusions.

Comparing costs effectively: beyond the monthly premium

The monthly premium is the number most people look at first, and it is genuinely the least useful number in isolation. Consumers often neglect cumulative annual cost and focus on monthly premiums alone, which leads to costly mistakes.

Here is how to think about total cost instead. For any plan you are seriously considering, calculate your likely annual spend under three scenarios: low medical usage (one or two GP visits), moderate usage (a minor procedure, two or three specialist visits), and high usage (hospitalisation or ongoing treatment). For each scenario, add the annual premium to your expected deductible and copay costs, then check whether you would hit your out-of-pocket maximum.

A plan with a low monthly premium and a high deductible can actually cost more overall, depending on how much medical care you use. This is one of the most reliably misunderstood dynamics in insurance purchasing.

The table below illustrates how different cost structures play out across a moderate-usage year for a 45-year-old expat:

| Cost component | Plan A (low premium) | Plan B (mid-range) | Plan C (comprehensive) |

|---|---|---|---|

| Annual premium | £1,800 | £2,640 | £4,200 |

| Annual deductible | £1,500 | £800 | £300 |

| Copay per visit (est. 6 visits) | £180 | £120 | £60 |

| Out-of-pocket max | £5,000 | £3,000 | £1,500 |

| Estimated total (moderate use) | £3,480 | £3,560 | £4,560 |

At low usage, Plan A wins. At high usage, Plan C’s lower out-of-pocket maximum could save you thousands. The point is that no single plan is objectively cheapest. It depends entirely on your likely medical consumption.

Where applicable, also check subsidy eligibility. In some markets, over 90% of enrollees receive premium subsidies with average savings exceeding $500 per month. For expats returning home or those with dual residency, this can significantly alter the cost equation.

Pro Tip: Never compare plans using monthly figures alone. Build a simple spreadsheet with annual premium, likely out-of-pocket spend under two scenarios, and the out-of-pocket maximum. That single comparison will tell you more than any premium-only table.

Evaluating coverage features for international travellers

Cost gets you in the door. Coverage is what actually protects you. When you compare health care plans for use abroad, several features carry outsized importance that you would not necessarily consider when choosing a domestic plan.

Pre-existing conditions are the most significant differentiator for many travellers. Waiting periods for pre-existing diseases range from three to four years depending on the insurer. If you have a chronic condition and need treatment within the first year of cover, some plans will not pay out at all. Always request written confirmation of how a specific condition is treated under each plan before enrolling.

Provider networks deserve equal attention. Verifying your specific doctors and hospitals are in-network avoids expensive out-of-network charges that can erase any premium savings. For expats in countries with mixed public and private healthcare, this matters enormously. Ask each insurer for a list of in-network providers in your specific city, not just the country.

Beyond the basics, here are the features that frequently make or break international cover:

- Emergency evacuation: Does the plan cover medical evacuation to a facility capable of treating your condition? This is non-negotiable for remote postings.

- Telehealth access: Many plans now offer online medical consultations, which are particularly useful in countries where English-speaking doctors are scarce.

- Annual health checks: Some international plans include preventive care. Others do not. If routine screening matters to you, verify it explicitly.

- Restoration benefits: Restoration benefits replenish the sum insured after claims, either once or without limit. For anyone with chronic conditions or high healthcare usage, this feature can mean the difference between being covered for the full year or running out of benefit by September.

- Claims settlement ratio: This tells you what percentage of claims an insurer actually pays. A low ratio is a warning sign, regardless of how attractive the premium appears.

Lower premiums often come with hidden limits such as sub-limits for room rent and narrower hospital networks, causing higher out-of-pocket costs in emergencies. Read the fine print on accommodation limits, as some plans cap daily hospital room costs at figures that fall well short of private hospital rates in expensive cities.

Common pitfalls when comparing medical plans

Even well-researched buyers make avoidable mistakes. Here are the most common errors to watch for when you compare medical plans for international use:

- Focusing only on the monthly premium. As discussed, this is the single most misleading metric. A cheaper premium with a high deductible can cost significantly more over a full policy year.

- Skipping network verification. The cheapest plan is worthless if your preferred doctors are not covered. Verify network directories before enrolment, not after.

- Ignoring exclusions. Every policy has them. Common exclusions include adventure sports injuries, mental health treatment, fertility treatments, and dental care. Make sure you understand what is not covered, not just what is.

- Overlooking coverage lapses. If you are transitioning from one plan to another, check for any gap period where you would be uninsured. Even a week without cover abroad can be extremely risky.

- Rushing the comparison process. Side-by-side comparison of at least three plans is a minimum standard. Reading two and picking the cheaper one is not a comparison.

- Trusting commission-driven comparison sites uncritically. Commission-based comparison websites may omit the best-value policies. Always cross-reference results with an independent broker or regulator-approved source.

This is also worth noting for those comparing cover for older family members. Travel insurance for seniors comes with its own set of eligibility requirements and cost structures, and many standard comparison tools do not account for these adequately.

Final steps: verifying and enrolling with confidence

Once you have narrowed down your options to two or three plans, the verification phase begins. This is where most people rush, and where mistakes most often happen.

Work through the following before you finalise any plan:

- Confirm subsidy or cost-sharing eligibility if you are buying through an official marketplace or employer scheme. Subsidies can dramatically change the true cost of a plan.

- Use official marketplaces or licensed brokers rather than generic aggregators. For international expat cover, work with a specialist who understands cross-border policy nuances.

- Verify provider participation directly. Call the hospital or clinic you intend to use and confirm they accept your plan. Do not rely solely on the insurer’s online directory, as these are not always current.

- Check prescription coverage specifically. If you take regular medication, confirm it is covered under the plan’s formulary and at what cost-sharing level.

- Set calendar reminders for your open enrolment window and annual renewal date. Missing a renewal deadline abroad can leave you uninsured without warning.

- Store your insurance documents securely. Keep digital and physical copies of your policy number, emergency contact lines, and claims procedures. In a medical emergency, you do not want to be searching for this information.

My honest take on international insurance comparison

I have worked with expats and international travellers long enough to know that the comparison process rarely gets the attention it deserves. People spend hours researching flights and accommodation, then spend 20 minutes choosing a plan that could cost them tens of thousands if it fails them.

The pattern I see most often is this: someone picks a plan based on price, moves abroad, and then discovers that their preferred hospital is out-of-network, or that their existing condition has a four-year waiting period. By then, it is too late to change course without a coverage gap.

What actually works is treating the comparison like a financial model, not a product search. Run the numbers for how you actually expect to use healthcare, not how you hope you will use it. Then verify every assumption directly with the insurer before you sign.

The features most people overlook are restoration benefits and emergency evacuation. Both feel abstract until you need them. A plan that replenishes your sum insured after a major claim keeps you protected for the rest of the year. A plan without evacuation cover could leave you hundreds of kilometres from the nearest adequate facility with no financial support.

My advice is to spend as much time on coverage features as you do on cost. They are equally important, and the cost of getting it wrong is not just financial.

— Coert

Find the right plan with Unparalleledglobalbenefits

Comparing international medical insurance plans is genuinely complex, and it gets more so when you factor in different countries, visa types, age brackets, and pre-existing conditions. Unparalleledglobalbenefits specialises in exactly this: helping expats, long-stay travellers, visitors, and families find cover that fits their actual situation, not just the cheapest option available.

Whether you need expat health insurance for full-year cover abroad, visitor cover for family members joining you, or guidance on the types of expat insurance that apply to your circumstances, the team at Unparalleledglobalbenefits can walk you through your options and arrange a personalised quote.

Planning a trip for yourself, a resident, or visiting family? UGB + Ekta can arrange travel insurance for seniors up to 100 years old. Just click here: https://ektatraveling.com/?partner_uid=808 and add the promo code “UGB” to receive an additional 10% discount.

You can also watch this short overview to understand your options better:

https://youtu.be/bjzvma7Sh1g

FAQ

What is the most important factor when comparing medical insurance plans?

Total annual cost is more reliable than monthly premium alone. Add your premium, expected deductibles, and copays together for a realistic picture of what each plan will actually cost you.

How do I compare health insurance plans for international living?

Start by identifying the plan type you need (travel, visitor, or international health insurance), then compare costs, provider networks, exclusions, and key features such as emergency evacuation and pre-existing condition terms across at least three plans.

What are pre-existing condition waiting periods and why do they matter?

Waiting periods are the length of time you must hold a policy before a pre-existing condition is covered. These range from three to four years depending on the insurer, making this a critical factor for anyone with an ongoing health condition.

Should I use a comparison website to find the best health insurance plan?

Use comparison tools as a starting point, but be aware that commission-based sites may not show all available options. Cross-reference with an independent broker or directly with insurers to confirm you are seeing the full picture.

How do provider networks affect my cover abroad?

If your doctor or hospital is outside your plan’s network, you will pay significantly more out of pocket, often enough to erase any savings you made on the premium. Always verify network participation before enrolling.

Recommended

- How insurance works overseas: a guide for expats and travellers – Unparalleled Global Benefits

- 7 Essential Steps to Compare Medical Insurance Plans Abroad – Unparalleled Global Benefits

- How to Compare Insurance Plans for Global Lifestyles

- Best International Insurance Plans for Expats – Expert Comparison 2025 – Unparalleled Global Benefits