TL;DR:

- Travel insurance is essential because most domestic health plans do not cover medical emergencies abroad, risking significant costs. Adequate family holiday coverage must include medical limits, evacuation, child inclusion, and clear exclusions to prevent unexpected financial burdens. Carefully reviewing policy terms and customizing coverage ensures families are protected against common risks and unexpected events during international trips.

Planning a family holiday abroad is exciting, but one assumption could put your entire family at risk: the belief that your existing health insurance will cover you overseas. It will not, in most cases. Medicare and Medicaid do not pay for medical care outside the United States, and similar restrictions apply to many private domestic health plans worldwide. Without the right cover in place, a single medical emergency could cost your family tens of thousands of pounds, dollars, or euros, turning a dream holiday into a financial crisis. This guide explains exactly what you need, what to look for, and what to avoid.

Table of Contents

- Why family holiday insurance matters: the hidden risks

- Essential features of family holiday insurance

- Understanding exclusions and hidden gaps

- Comparing family insurance plans: a practical framework

- What most family insurance guides get wrong

- Find the right cover for your next family trip

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Medical costs dominate claims | Nearly half of family travel claims are for medical emergencies, making strong cover essential. |

| Check policy exclusions | Always read the fine print for exclusions like pre-existing conditions and pandemics to avoid denied claims. |

| Compare benefits and limits | Use a structured checklist to compare evacuation, child inclusion, and cover triggers when choosing a plan. |

| Don’t rely on home insurance | Most domestic health insurance offers little or no protection once your family leaves the country. |

Why family holiday insurance matters: the hidden risks

The biggest financial shock for families travelling without proper insurance is almost always medical. Think about what it actually costs to receive emergency care in a foreign country: hospital admission fees, specialist consultations, prescription medication, and potentially air ambulance services if your destination lacks adequate local facilities. These costs add up with frightening speed, and they are not theoretical. Nearly half of all travel claims are medical-related, with more than 40% of all insurance claims processed by nib Travel in 2024 falling into this category. That figure reflects what actually happens to real families on real trips.

Your domestic health plan was designed for care within your home country. The moment you cross an international border, most of those benefits either reduce dramatically or disappear entirely. As already noted, Medicare and Medicaid provide no cover for medical care outside the United States, and private insurers often have equally strict geographic limitations buried in the policy terms. Many families only discover this when it is already too late to do anything about it.

Here are the most common situations where uninsured families face serious financial exposure:

- A child develops a sudden high fever requiring hospitalisation in a country where English is not widely spoken

- An adult family member suffers a broken bone or serious injury during a day trip

- A parent needs emergency surgery and requires medically supervised transport home

- A pre-existing condition flares up unexpectedly in a destination with high private healthcare costs

Understanding illness and family member coverage is the first step towards making an informed choice. The second step is accepting that good cover is not optional.

“Without travel insurance, a single hospitalisation abroad can cost more than the entire cost of the family holiday itself. The bill arrives when you are already exhausted and worried.”

Pro Tip: Even policies that do technically cover you abroad often require you to pay the full cost upfront and then reclaim it later. If your savings cannot absorb a £20,000 hospital bill in the short term, you need a plan with direct billing or assistance services built in.

Understanding why families need travel insurance fully means going beyond cost alone. There is also the practical reality of navigating a foreign healthcare system, often in another language, while you are stressed and worried about a family member. A good travel insurance policy does not just pay bills. It provides access to 24-hour assistance lines, referrals to trusted local hospitals, and coordination of care so you are never left making critical decisions alone.

Essential features of family holiday insurance

Once you accept that specialist cover is essential, the next question is: what should that cover actually include? Not all travel insurance policies are created equal, and a cheap single-trip policy that covers one adult for a European city break may be entirely inadequate for a family of four spending three weeks in Southeast Asia.

When comparing emergency medical limits and other key features, you need to assess your family’s actual profile. The age of your children, any pre-existing medical conditions, the duration of your trip, and your destination all affect what level of cover is appropriate. Using a structured checklist, as outlined in U.S. State Department guidance, helps families compare emergency medical limits, evacuation provisions, child inclusion terms, pre-existing condition waivers, and coverage triggers side by side.

Here is a clear reference table to guide your comparison:

| Feature | What to look for | Why it matters |

|---|---|---|

| Emergency medical limit | Minimum £1 million per person | Covers hospitalisation and specialist care |

| Medical evacuation | Included, with direct coordination | Essential if local facilities are inadequate |

| Child inclusion | Up to what age? How many children? | Policies vary widely on child terms |

| Pre-existing conditions | Waiver available or automatic cover? | Adults and children may both be affected |

| Trip cancellation | Covered for illness, death, injury | Protects non-refundable costs |

| 24-hour assistance | Direct access helpline | Critical in an emergency situation |

| Repatriation of remains | Included | Rarely discussed but essential cover |

The detail around child inclusion is particularly important. Many families assume that because they are buying a “family policy,” their children are automatically included at no extra cost and with full benefits. In reality, many insurers set age cut-offs at 18, 21, or sometimes lower, and there may be limits on the number of dependent children included per adult policy.

Pro Tip: Do not assume children are covered for free without reading the specific terms. Check the age cut-off, confirm how many children are included, and verify whether the child benefits mirror the adult benefits or are limited in scope.

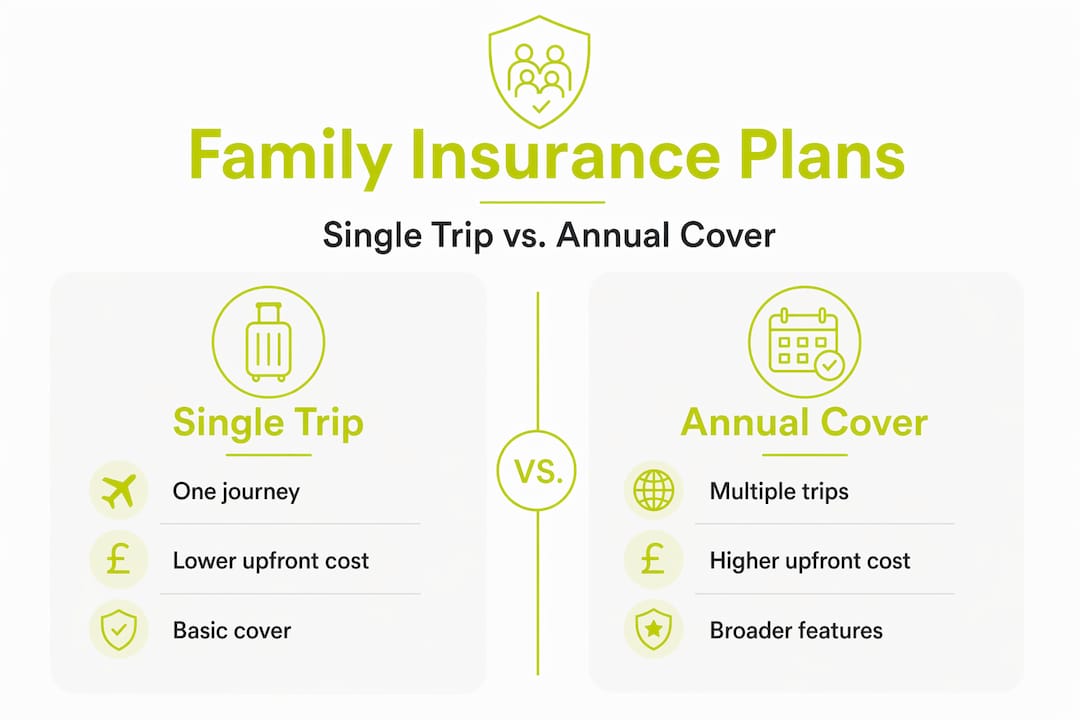

Exploring global family insurance options will also show you the difference between single-trip plans and annual multi-trip policies, which can be more economical for families who travel more than once a year. If you typically take two or three trips per year, an annual plan may offer better overall value, as covered in these annual family cover tips.

Understanding exclusions and hidden gaps

Even the most thorough-looking policy can leave your family exposed if you have not read the exclusions carefully. Exclusions are the situations a policy will not pay out for, and they are arguably more important to understand than the listed benefits. Many claim denials happen not because the insurer acted in bad faith, but because the family genuinely did not know the exclusion existed.

Common exclusions in family insurance include the following categories:

- Known medical conditions that were not declared or are not covered by a waiver

- Pandemic-related illness unless the policy specifically includes epidemic and pandemic cover

- Civil unrest, political events, or travel to government-advised unsafe destinations

- Pregnancy complications and childbirth (most standard travel policies exclude these entirely)

- Hazardous or adventure activities such as skiing, scuba diving, or motorcycling

- Self-inflicted injuries or incidents linked to alcohol consumption

The data supports the need for caution. As documented by Monde du Voyage, common exclusions consistently include known risks, pre-existing conditions, pandemics unless specified, civil or political unrest, pregnancy and childbirth, and hazardous activities.

“Families often buy a policy because it looks affordable, only to discover the activities they planned are excluded. A skiing trip or a snorkelling excursion may require specific add-ons.”

To review exclusions properly before you buy, follow these steps:

- Request the full policy wording, not just the summary document or marketing brochure.

- Search the document for the words “exclude,” “not covered,” and “limitation” to identify restriction clauses quickly.

- Cross-reference every planned activity against the excluded activities list.

- If you or any family member has a pre-existing condition, contact the insurer directly and get written confirmation of whether it is covered.

- Ask specifically about pandemic cover and whether the policy applies if a family member catches a disease in a destination under a travel advisory.

Reviewing a single trip family cover plan in detail before signing will almost always surface at least one exclusion that affects your specific circumstances. This is normal. What matters is that you know about it before you travel, not after a claim is refused.

Comparing family insurance plans: a practical framework

Once you understand what to look for and what to avoid, comparing plans becomes a much more structured exercise. The biggest mistake families make at this stage is choosing on price alone. The cheapest policy is rarely the best value, particularly when the cost of a single uncovered claim dwarfs the savings made on the premium.

Families should compare emergency limits, evacuation provisions, child policy terms, condition waivers, and how coverage is triggered before making a final decision. Here is a comparison table to illustrate how different plan types typically differ:

| Plan type | Medical limit | Child inclusion | Activity cover | Pre-existing conditions |

|---|---|---|---|---|

| Budget single-trip | Up to £500,000 | Up to age 17 | Basic only | Rarely included |

| Standard family plan | Up to £2 million | Up to age 21 | Some activities | Optional waiver |

| Premium family plan | £5 million or more | Up to age 25 | Wide activity range | Waiver often available |

| Expat/annual plan | Comprehensive | Varies by plan | Often extensive | Declared conditions covered |

Use this framework alongside the following questions to shortlist your options:

- What is the per-person emergency medical limit, and does it apply to children separately or as part of a family total?

- Does the policy include direct billing, or will you need to pay upfront and claim later?

- Is emergency evacuation covered automatically, or is it a paid add-on?

- How does the policy define a “pre-existing condition,” and is there a look-back period?

- Can the policy be extended from abroad if the trip is delayed or extended unexpectedly?

- What is the claims process, and is there 24-hour telephone support in English?

For a deeper breakdown of how travel medical vs health insurance plans compare, it is worth reviewing the technical differences between the two product types, as many families confuse them. You can also explore top policy comparisons for a broader market overview that can sharpen your shortlist further.

The goal is not to find the most expensive policy or the one with the longest list of included benefits. The goal is to find the policy that fits your specific family, your specific destinations, and your specific health profile as closely as possible.

What most family insurance guides get wrong

Most articles about family travel insurance treat the purchase process as a simple box-ticking exercise. Buy a policy, check a few features, and you are done. The reality is far more nuanced, and this simplified approach is precisely why so many claims get denied.

The real challenge is not finding a policy. It is customising that policy to your family’s actual circumstances. A family with a child who has asthma, a parent with a history of hypertension, and a planned itinerary that includes both water sports and high-altitude trekking has a completely different coverage requirement from a family of healthy adults spending a week at a European beach resort. Generic guides rarely acknowledge this.

Claim denials most often occur because families are unfamiliar with two things: waiver conditions and terminology. A “pre-existing condition waiver” does not automatically mean all pre-existing conditions are covered. It usually means that stable, declared conditions are covered under specific criteria, such as no change in medication in the previous 90 days. If you do not know that, and you have changed a family member’s medication three months before travel, you may be uninsured without realising it.

The insight from due diligence research reinforces this: reading the actual policy wording and confirming real limits is essential before purchase. Marketing summaries are designed to sell policies, not to provide the complete picture.

There is also a tendency for families to over-rely on comparing comprehensive options without verifying the underlying terms. A policy labelled “comprehensive” still has exclusions. The label is a marketing term, not a legal guarantee.

Pro Tip: Before you finalise any policy, write down the three most likely medical scenarios your family could face on this specific trip. Then look up each scenario in the policy wording to confirm it is covered. This ten-minute exercise has saved many families from very expensive surprises.

Find the right cover for your next family trip

Knowing what to look for is the most important step, but the next is taking action before your departure date. Leaving insurance until the last moment limits your options and may mean missing cover for a claim that arises between booking and travel.

At Unparalleled Global Benefits, we specialise in international insurance solutions tailored to the specific needs of travelling families. Whether you need a straightforward travel health insurance guide to understand your options, or you are looking for flexible single trip expat cover that fits an international lifestyle, our resources and expert team are here to help. We work with families across a range of circumstances, from first-time international travellers to long-term expats, to find the cover that genuinely fits. Contact us today to request a personalised quote and get the protection your family deserves before you board.

Frequently asked questions

Does my family need travel health insurance if we have private health cover?

In almost all cases, private health insurance does not pay for care outside your home country, so travel health insurance is essential for international trips. As U.S. State Department guidance confirms, Medicare and Medicaid provide no international cover, and you should check your private insurer’s geographic terms carefully.

Are children always included at no extra charge under family travel insurance?

Not always. Many insurers set age cut-offs and may limit the number of children per family policy, as eligibility criteria vary considerably between providers, so check inclusions closely before you buy.

What are the most common exclusions to look out for?

Exclusions usually include known risks, pre-existing medical conditions, pandemics, civil unrest, and certain activities. According to Monde du Voyage’s exclusion summary, adventure sports and pregnancy-related complications are also frequently excluded from standard policies.

Can travel insurance cover be extended if our holiday runs longer than planned?

Some insurers allow extensions, but you must arrange this before the planned trip end date, as requesting an extension after the policy expires will leave you without valid cover.

What happens if we need emergency evacuation?

If your policy includes evacuation cover, the insurer can arrange and cover transport to appropriate medical facilities, but the limits and triggers vary significantly between plans, so confirm the specific terms before you travel.

Recommended

- Travel Insurance for Families: Protect Your Loved Ones on Every Adventure

- Travel Insurance Family Cover: Ensuring Peace Abroad – Unparalleled Global Benefits

- Family Travel Insurance – Protecting Expat Life Abroad – Unparalleled Global Benefits

- Travel Insurance Illness Family Member: Secure Coverage Guide – Unparalleled Global Benefits