TL;DR:

- Medical evacuation insurance is essential for covering the high costs of urgent transport when local healthcare facilities are inadequate. It functions by coordinating timely medical transport to appropriate facilities, especially in remote or high-risk regions. Effective use depends on prompt insurer contact, thorough documentation, and understanding coverage exclusions and coordination networks.

A medical emergency abroad can happen to anyone, regardless of how carefully you plan your trip. What most travellers do not realise is that standard travel insurance rarely covers the full cost of getting you to adequate medical care, and evacuation costs can escalate into the tens or even hundreds of thousands of pounds, particularly in remote locations or when intensive care is required. Medical evacuation insurance exists specifically to fill this gap, funding and coordinating urgent transport to proper facilities when your life may depend on it. This article walks you through everything you need to know about medevac cover, from how it works to what the fine print really means.

Table of Contents

- What is medical evacuation insurance and why does it matter?

- How medical evacuation works in practice

- Medical evacuation versus repatriation: what’s the difference?

- Fine print and limitations: what most policies exclude

- How to maximise your coverage and claim success

- What most travellers miss about medevac insurance: the importance of coordination

- Protect your health abroad with expert medical evacuation cover

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| High costs covered | Medical evacuation insurance protects you from unexpectedly large emergency travel bills that could reach hundreds of thousands of pounds. |

| Different from repatriation | Evacuation insurance is for urgent transport to a nearby hospital, while repatriation returns you home once you are stable. |

| Policy fine print matters | Trip length, distance, and documentation rules can affect your coverage, so you must review terms carefully. |

| Coordination is crucial | The insurer’s ability to coordinate logistics and approvals can be as important as the amount they pay. |

| Take action for claims | Always contact your insurer immediately and keep all medical documentation to ensure claim success. |

What is medical evacuation insurance and why does it matter?

Understanding medical evacuation insurance starts with knowing exactly what it does. At its core, medevac insurance funds and coordinates urgent transportation, often via ambulance or air ambulance, from the location where you fall ill or are injured to the nearest adequate medical facility. This is not the same as standard travel insurance, which typically covers trip cancellations, lost luggage, and limited medical treatment costs. Medical evacuation cover takes over when the healthcare available locally simply is not sufficient for your condition.

This distinction matters enormously. You might have a robust travel insurance policy and still find yourself facing a bill of £80,000 or more if you need to be airlifted from a remote region of South-East Asia or sub-Saharan Africa to a hospital capable of treating your condition. Standard policies often place strict caps on emergency transport or exclude it altogether. That is the gap medevac cover is designed to close.

Who needs this type of cover? The short answer is: almost any international traveller. But medevac cover is especially beneficial for expatriates, long-term travellers, those visiting regions with limited healthcare infrastructure, and anyone with a pre-existing condition that could require specialist intervention abroad. If you are living and working overseas, the stakes are even higher because you are not simply passing through.

| Situation | Risk level | Why medevac matters |

|---|---|---|

| Remote trekking or adventure travel | Very high | Air ambulance may be the only option |

| Expatriate living in a developing country | High | Local hospitals may lack specialist care |

| Cruise ship passenger | High | Nearest port facility may be inadequate |

| Business traveller in a major city | Moderate | Specialist treatment may still require transfer |

| Short holiday in Western Europe | Lower | Still possible if condition is serious enough |

Consider the scenario of a British expatriate working in rural Indonesia who suffers a cardiac event. The nearest hospital may not have the cardiac surgery capability needed. Getting that person to Singapore or Kuala Lumpur, cities with advanced cardiac centres, could cost more than £60,000 by air ambulance. Without medevac cover, that bill falls entirely on the individual or their employer.

Pro Tip: When reviewing any travel or expat insurance plan, check whether medical evacuation is included as a standalone benefit or only as an add-on. Many basic plans list it in small print as secondary coverage, meaning it only pays out after other insurance has been exhausted.

For a solid introduction to medevac insurance, including what to look for in a plan, it is worth reviewing the basics before comparing providers. If you are new to the concept, reading about emergency medical evacuation basics can also help you ask the right questions.

How medical evacuation works in practice

Knowing that medevac cover exists is one thing. Understanding what actually happens when you need to use it is another. The process is more structured than most people realise, and knowing the steps in advance can reduce confusion during what is already an extremely stressful situation.

Medevac logistics follow a coordination workflow: gathering clinical details, identifying the most appropriate receiving facility, arranging transport, and securing authorisation from the insurer or assistance provider. Each step must happen in the right order, and delays at any point can affect both your safety and your claim.

Here is what typically occurs once an evacuation is triggered:

- Medical assessment: A treating physician on the ground documents your condition and confirms that local facilities cannot provide adequate care. This physician statement is critical for authorisation.

- Contact with your insurer: You or a companion calls the insurer’s 24-hour emergency line. This call should happen as early as possible. Insurers will not typically reimburse transport arranged without prior authorisation except in life-threatening situations where no time exists.

- Coordination of transport: The insurer’s assistance team identifies the appropriate receiving hospital and arranges the mode of transport, whether that is a commercial flight with a medical escort, a chartered air ambulance, or ground transport.

- Authorisation and documentation: The insurer reviews the clinical information and formally authorises the evacuation. At this point, transport providers receive confirmation that costs will be covered.

- Transfer and handover: You are transported to the receiving facility, where the medical team has been briefed in advance. The insurer’s coordination team remains in contact throughout.

“The difference between a smooth evacuation and a chaotic one often comes down to how quickly the insurer is contacted and whether the clinical documentation is in order from the outset.”

The insurer’s assistance network plays a central role here. Established providers maintain relationships with hospitals, air ambulance operators, and medical escorts across the globe. This network is what makes vital protection abroad a practical reality rather than just a policy promise. For expatriates in particular, understanding evacuation procedures for expats before an emergency arises is one of the most sensible things you can do.

Pro Tip: Store your insurer’s 24-hour emergency number in your phone before you travel, not just in your policy documents. In a genuine emergency, searching for paperwork wastes precious time.

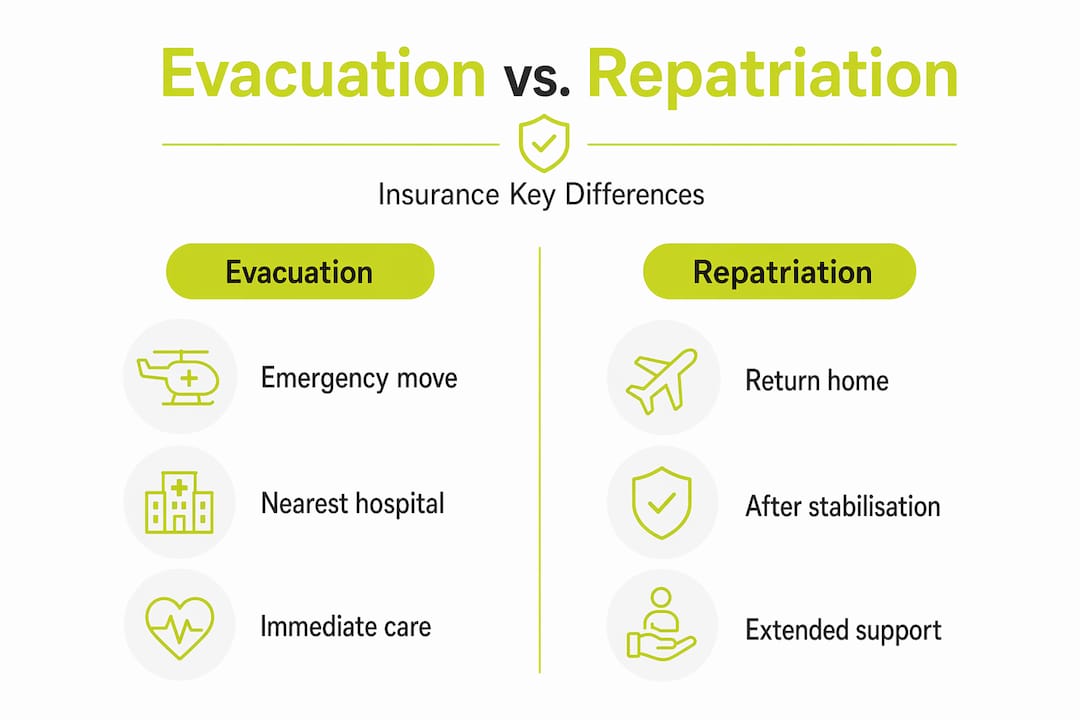

Medical evacuation versus repatriation: what’s the difference?

These two terms are frequently used interchangeably, but they refer to different things and cover different situations. Getting clear on the distinction helps you choose the right combination of cover for your circumstances.

Medical evacuation moves the patient to the nearest adequate hospital, while repatriation refers to transport back to your home country after you have been stabilised. Evacuation is an emergency response. Repatriation may happen days or even weeks later, once you are medically fit to travel.

| Feature | Medical evacuation | Repatriation |

|---|---|---|

| Timing | During acute emergency | After stabilisation |

| Destination | Nearest adequate facility | Home country |

| Purpose | Access to immediate care | Return to home environment |

| Urgency | High, often immediate | Planned, coordinated |

| Covered separately? | Usually yes | Sometimes bundled |

Why does this distinction matter in practice? Imagine you are trekking in Nepal and break your leg in a complex fall. An evacuation might take you from the trekking route to a hospital in Kathmandu. Once treated and stable, repatriation would then arrange your transport back to the United Kingdom for ongoing rehabilitation. These are two distinct journeys, and they may be covered by different sections of your policy or require separate claims.

Some insurers bundle both into a single benefit, while others treat them as separate features with different limits. Always check whether your plan covers repatriation in addition to evacuation, or whether the two share a single financial limit. If they share a limit, an expensive evacuation could leave little remaining cover for your journey home.

Key scenarios where the difference matters:

- Only evacuation needed: You are treated abroad successfully and return home via normal travel. Repatriation is not triggered.

- Only repatriation needed: You were treated locally but wish to return home for recovery. Evacuation was not required.

- Both needed: You are evacuated to a regional hospital and later repatriated home. Both benefits apply in sequence.

Understanding the full landscape of expat insurance types can help you build a policy combination that covers both scenarios without leaving gaps.

Fine print and limitations: what most policies exclude

Even a well-structured medevac policy can leave you exposed if you have not read the terms carefully. Many travellers assume that once they have a policy, they are fully protected. The reality is more nuanced.

Policy edge cases hinge on specific definitions: many plans require that the evacuation be deemed medically necessary by a licensed physician, supported by appropriate documentation, and that it comply with trip-length and distance-from-home requirements built into the policy wording.

Common exclusions and limitations to watch for:

- Distance-from-home rules: Many policies exclude emergencies occurring within 100 miles of your home address, on the basis that you can access domestic healthcare.

- Trip duration caps: Some plans only apply to trips of a specified maximum length, such as 30, 60, or 90 days. Long-term travellers and expatriates may need specialist cover.

- Secondary coverage clauses: Some medevac policies only pay after other applicable insurance has been exhausted, which can slow down claims and create disputes.

- Pre-existing condition exclusions: Conditions you already had before purchasing the policy may not be covered, even if the evacuation itself is unrelated.

- Unapproved transport: If you arrange your own transport without insurer authorisation, you risk having the claim denied entirely.

- Adventurous activities: Evacuation resulting from extreme sports or activities listed as excluded hobbies may not be covered.

One critical point that many travellers overlook is the physician approval requirement. Your insurer needs confirmation from a treating doctor that evacuation is medically necessary. If you attempt to arrange transport without this, you may find your claim is reduced or refused. This is not about bureaucracy; it is about ensuring the insurer has evidence that the decision was clinically justified.

Before purchasing any policy, ask these questions directly: Does the plan require prior authorisation for all evacuations? What documentation must be submitted? Are there trip-length or distance restrictions? Understanding what basic travel insurance covers and where it falls short will help you identify the gaps that medevac cover needs to fill. You should also review travel insurance requirements for safe trips before departure.

How to maximise your coverage and claim success

Selecting the right policy is only the first step. Knowing how to use it effectively during an emergency is equally important. Most claim failures are not due to policy gaps; they are due to process failures at critical moments.

Maximising a successful evacuation claim requires calling your insurer or assistance provider promptly, ensuring a licensed physician confirms medical necessity, and maintaining thorough documentation throughout the process. These three actions address the most common reasons claims are disputed or reduced.

Here is a practical checklist for a smooth claim experience:

- Call immediately. Contact your insurer’s emergency line at the first indication that evacuation may be needed, before transport is arranged.

- Get physician documentation. Ensure the treating doctor records the clinical justification for evacuation in writing.

- Follow insurer instructions. Your assistance provider will guide you step by step. Deviating from this process can affect your claim.

- Keep all receipts and records. This includes hospital invoices, physician statements, transport receipts, and any correspondence with your insurer.

- Confirm the receiving hospital. The insurer’s coordination team should arrange the destination facility. Confirm this in writing where possible.

- Notify family or a trusted contact. They can assist with communication and documentation if your condition prevents you from managing the process yourself.

Beyond the claims process, the CDC advises treating medevac cover selection as a coordination problem rather than simply a cost-limit problem. A policy with a £500,000 evacuation limit but a weak assistance network may serve you less well than one with a £200,000 limit backed by a global network of vetted hospitals and transport providers.

Review the step-by-step evacuation claims process to prepare in advance. If you are travelling for a medical procedure, understanding travel insurance for medical procedures abroad is also worth your time.

What most travellers miss about medevac insurance: the importance of coordination

Here is a perspective that most comparison articles do not discuss. When people shop for medical evacuation cover, they tend to focus on two things: the premium and the coverage limit. Neither is the most important factor. The quality of the coordination network behind the policy is what truly determines whether you receive the care you need, when you need it.

Think about what a medevac event actually involves. It is not just a financial transaction. It is a live operational challenge: identifying the right hospital, securing beds and specialists, arranging specialist air transport, communicating between multiple parties across time zones, and doing all of this under pressure. An insurer with a strong global network can execute this in hours. One without can take days, and in serious cases, that delay is the difference between full recovery and long-term damage.

The phrase “nearest adequate facility” is another detail most travellers miss. Your policy will likely state that evacuation is to the nearest facility capable of treating your condition. But who defines “adequate”? Your insurer’s medical team does, in coordination with their ground network. An insurer with established relationships in a region will have up-to-date knowledge of which hospitals can genuinely handle complex cardiac cases, trauma surgery, or paediatric emergencies. An insurer without those relationships may default to a facility that is geographically close but clinically limited.

For expatriates especially, this matters enormously. You are not a tourist passing through. You have a community, a routine, and potentially a family depending on your ability to return to health efficiently. The right international health cover for expats is one that prioritises coordinated care, not just high limits on paper. Our strong advice: before you commit to any policy, ask your provider directly about their assistance network and which regions it covers. The answer will tell you more than any policy document.

Protect your health abroad with expert medical evacuation cover

Finding the right level of protection for your international travels or expatriate lifestyle does not have to be complicated, but it does require the right guidance.

At Unparalleled Global Benefits, we specialise in matching travellers and expatriates with cover that genuinely reflects their circumstances, not just generic plans. Whether you are seeking international expat health insurance with robust medevac benefits, want to understand the full range of types of expat insurance available to you, or are ready to compare options from top global insurers, we are here to help you make an informed decision. Medical evacuation is not an optional extra for serious travellers. It is a foundational layer of protection. Let us help you get it right.

Frequently asked questions

Does medical evacuation insurance cover COVID-19-related emergencies?

Some policies may cover COVID-19 evacuations when medically necessary, but terms vary significantly between providers, so always confirm COVID-specific inclusions before purchasing your policy.

Can I use emergency evacuation cover within my home country?

Most policies exclude emergencies within 100 miles of your home address, on the assumption that domestic healthcare is accessible, so always check your plan for specific distance-from-home rules.

Is repatriation included in medical evacuation insurance?

Evacuation and repatriation are separate features with different purposes; some policies bundle them into a single benefit, but you should always verify whether repatriation is covered independently and at what limit.

How much does a typical international evacuation cost?

Expenses can rise from around USD 25,000 to over USD 500,000 depending on location, distance, and transport type, making evacuation cover essential for any serious international traveller or expatriate.

What must I do first when I need evacuation abroad?

Call your insurer promptly, confirm that a licensed physician has documented the medical necessity, and follow your assistance provider’s coordination steps for authorisation and transport logistics.

Recommended

- Medical Evacuation Coverage: Vital Protection Abroad – Unparalleled Global Benefits

- International Expat Health Insurance: Protecting Your Wellness Abroad – Unparalleled Global Benefits

- Medical Evacuation Procedures: A Guide for Travelers and Expats

- How to Get Medical Insurance Abroad: Your Essential Guide for Expats and Travelers