TL;DR:

- Many visa rejections stem from missing or non-compliant insurance documents, not travel intentions or criminal history. Travel insurance must meet specific coverage, territorial, and formatting requirements; failure to do so can cause immediate application refusal. Properly prepared insurance signals responsible planning, increasing the likelihood of visa approval while providing essential financial protection during your trip.

Many visa rejections have nothing to do with travel intentions, criminal history, or financial records. They happen because of a single insurance document that was missing, incorrectly dated, or simply below the required coverage limit. Travel insurance is not a bureaucratic afterthought — it is often the first document a visa officer checks, and a non-compliant certificate can end your application before anything else is reviewed. This guide explains exactly what embassies require, how officers evaluate your policy, and how to choose cover that satisfies both visa rules and your genuine protection needs.

Table of Contents

- Why travel insurance is a key requirement for many visas

- How visa officers evaluate your travel insurance

- Benefits of travel insurance: More than just a visa box-tick

- Common mistakes and smart tips for choosing visa-accepted insurance

- What happens if you do or don’t get travel insurance for your visa

- Our take: The real reason travel insurance changes visa outcomes

- Ready to secure the right travel insurance for your visa?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Requirements vary by country | Some visas demand travel insurance while others simply recommend it. |

| Non-compliance leads to rejection | Missing or incorrect insurance documents will result in instant visa refusal for some destinations. |

| Insurance signals responsibility | Having travel insurance shows you are financially prepared and serious about your travel. |

| Extra value beyond compliance | Travel insurance offers health and financial protection, not just bureaucracy. |

| Choose wisely for peace of mind | Selecting the right cover avoids mistakes, saves money, and ensures stress-free journeys. |

Why travel insurance is a key requirement for many visas

Not every visa system treats travel insurance the same way, and understanding the differences is essential before you apply. The rules vary enormously depending on your destination, visa type, and nationality.

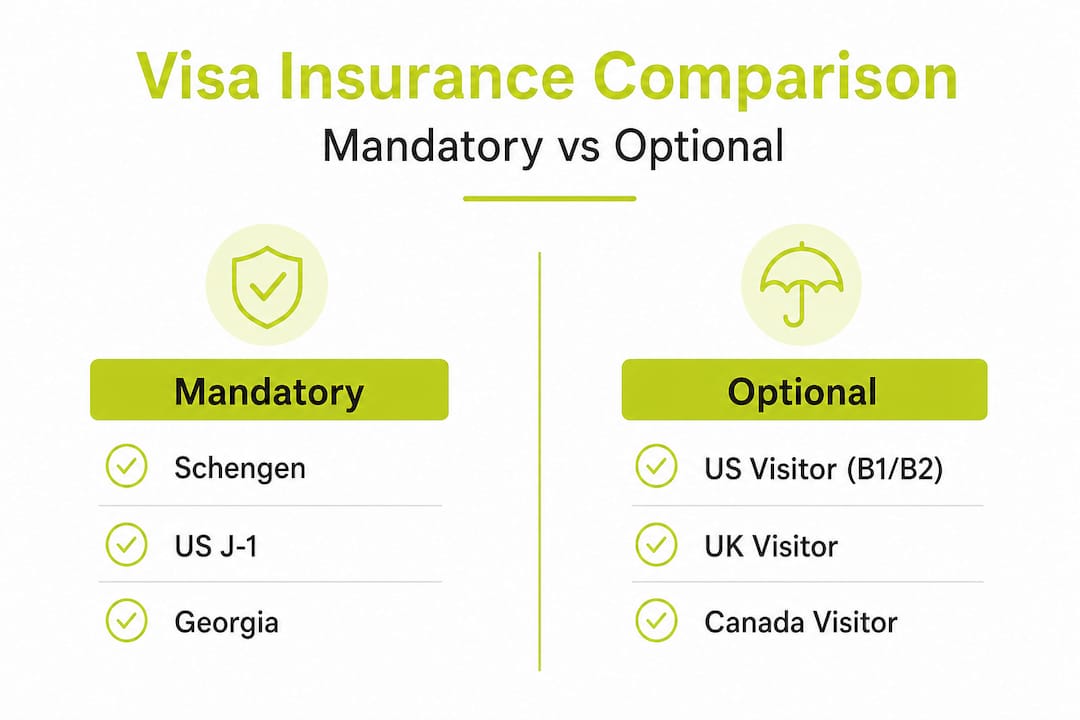

The Schengen Area has the most clearly defined insurance rules in the world. Under Article 15 of the EU Visa Code, travel insurance is a mandatory requirement for Schengen visa applications, requiring a minimum of €30,000 coverage for emergency medical treatment, hospitalisation, repatriation for medical reasons, and death. This policy must be valid across all 29 Schengen states for the entire duration of your stay. Non-compliance results in automatic rejection, full stop. There is no grey area, no appeals process for this specific failure, and no partial credit for submitting a policy that misses even one clause.

The Schengen visa insurance requirements are non-negotiable, and they serve a clear purpose. If you fall ill or are injured in Germany, Italy, or Spain, the state does not want to absorb your costs. Your insurance certificate is proof that the financial burden falls on your provider, not the host country.

Other destinations take a softer approach. For non-mandatory visas such as the US B1/B2 or UK visitor visa, travel insurance is not required by law but strongly demonstrates financial preparedness and responsibility. Submitting a solid policy alongside your application can genuinely strengthen your case, because it signals that you have planned responsibly and are unlikely to become a burden on public services.

The US J-1 exchange visitor visa stands apart from tourist visas. It mandates specific minimum coverage: $100,000 for medical expenses and $50,000 for medical evacuation. These are real figures with legal weight. Falling short of either means you will not receive your DS-2019 form, and without that form, your J-1 visa cannot be issued.

| Visa type | Insurance required? | Minimum medical cover |

|---|---|---|

| Schengen short-stay | Yes, mandatory | €30,000 |

| US J-1 exchange visitor | Yes, mandatory | $100,000 medical / $50,000 evacuation |

| UK visitor (B category) | Recommended | No fixed minimum |

| US B1/B2 tourist | Recommended | No fixed minimum |

| Georgia tourist (from 2026) | Yes, mandatory | Varies |

This comparison makes it clear: requirements are not uniform, and assuming one set of rules applies everywhere is a common and costly mistake. You can review the minimum travel insurance Schengen requirements in detail before you purchase any policy.

How visa officers evaluate your travel insurance

Understanding what embassies require is just the first step. Ensuring your documents pass consular scrutiny takes insider knowledge about how officers actually process what you submit.

Visa officers do not read your insurance policy like you would read a contract. According to consular processing research, visa officers scan insurance as a “risk document” for quick alignment with your passport and travel itinerary. Formal compliance trumps actual protection quality if your certificate fails their checklist. This means a beautifully worded policy with comprehensive cover can be rejected in seconds if the territory listed does not match your itinerary, or if the dates expire two days before your return flight.

The most common reasons insurance is rejected at the consular stage are:

- Wrong territory coverage: Your policy covers only France, but you are applying for a Schengen visa with stops in the Netherlands and Austria.

- Incorrect dates: Your policy starts the day after your flight departs or ends before your planned return.

- Insufficient medical limits: The certificate shows €20,000 instead of the required €30,000.

- Missing exclusions clarification: Policies that exclude pre-existing conditions without disclosing this clearly can be flagged.

- Wrong document format: Some embassies require the certificate to be printed on the insurer’s official letterhead with specific information fields visible.

“Insurance compliance is judged on form before substance. An officer checking dozens of applications per hour will reject a certificate that does not immediately align with the checklist, even if the underlying policy is solid.” — Consular processing insight from BookForVisa

This is a sobering reality. You could purchase an excellent policy from a reputable provider and still face rejection because the certificate format did not meet the embassy’s specific layout requirements. This is why getting travel insurance for Schengen visas from providers experienced with visa documentation matters significantly.

Pro Tip: Before submitting your application, place the embassy’s published insurance checklist alongside your certificate and verify every single field, including the insurer’s name, your full passport name, policy dates, coverage territory, and the minimum benefit figure. A one-minute check can prevent weeks of delay.

One thing many applicants overlook is the role insurance plays in assessing why visa travel insurance matters beyond the checklist. Officers also use it as an indirect measure of your travel intent. A well-structured certificate from a reputable provider suggests you have invested time in planning. A rejected or inadequate certificate can raise doubts about your preparedness overall.

Benefits of travel insurance: More than just a visa box-tick

Knowing how insurance is judged is essential, but it is just as important to understand why it matters for your actual trip, not solely for your paperwork.

Consider what happens if you fracture your wrist in Rome. Without insurance, a hospital visit, X-ray, surgery, and a night’s stay could cost several thousand euros out of pocket. With a compliant policy, those costs are handled by your insurer. The financial protection alone makes insurance worth every cent, even if you never file a claim.

Travel insurance also provides cover in situations that have nothing to do with medical emergencies. Trip cancellation cover reimburses non-refundable bookings if you cannot travel due to illness, a family bereavement, or severe weather. Lost or delayed baggage cover replaces essentials while airlines locate your luggage. Emergency evacuation cover funds the cost of transporting you home or to a better medical facility if the situation demands it.

For medical insurance for visa applications, the cover you choose should align with both the embassy’s requirements and your own health needs. Pre-existing conditions, adventure activities, and extended trips all influence which policy is right for you.

The benefits for your visa application extend beyond compliance too. For non-mandatory visas, omitting insurance signals poor planning to officers assessing your intent to return and your financial stability. It is a subtle but real signal. Officers are evaluating whether you are a responsible traveller who has prepared for contingencies, or someone who might overstay, claim public services, or encounter problems they cannot handle.

Pro Tip: When applying for a US or UK visitor visa, consider including a brief cover note with your insurance certificate explaining the scope of cover. This demonstrates awareness and preparation, two qualities officers value when assessing discretionary applications.

Here is a summary of practical benefits that go beyond visa compliance:

- Protection against medical costs that could otherwise run into tens of thousands of pounds

- Compensation for cancelled or disrupted travel plans

- Cover for lost, stolen, or delayed baggage

- 24-hour emergency assistance helplines available wherever you are

- Possible multi-destination cover that protects you in countries beyond your primary destination

- Strengthened visa application profile for discretionary decisions

You can explore getting the right medical insurance for a visa and understand how to align your personal health needs with embassy requirements simultaneously.

Common mistakes and smart tips for choosing visa-accepted insurance

Beyond general benefits, let us focus on practical steps and common pitfalls to help you make confident, cost-effective decisions.

Many applicants rush to purchase the cheapest policy available, only to discover after submission that it fails one or more visa criteria. Others over-invest in comprehensive policies with benefits far exceeding what the embassy requires, spending significantly more than necessary. Neither approach serves you well. Here are the most frequent mistakes and how to avoid them:

- Not verifying all visa criteria are met: Always cross-reference the specific embassy checklist for coverage amount, territory, and dates before purchasing. Do not assume that any travel insurance product will automatically qualify.

- Skipping visa-refusal refund cover: Some policies offer a visa refusal refund clause for approximately €15 to €35 for a two-week Schengen trip. If your visa is refused for unrelated reasons, this refunds your premium. Importantly, insurance never reimburses the embassy’s visa application fee.

- Relying on bank card travel insurance: Basic complimentary insurance offered through current accounts and credit cards is rarely sufficient for visa purposes. The coverage limits are typically too low, the territories too restricted, and the certificate format unsuitable for embassy submission.

- Choosing excessive coverage when minimum suffices: If the embassy requires €30,000 and you purchase €500,000 coverage without additional genuine benefit to you, you are overpaying. Match coverage to requirements and your personal risk profile.

- Ignoring exclusion clauses: A policy that excludes the activities you plan to undertake, or excludes pre-existing conditions relevant to you, may leave you unprotected even if it satisfies the visa requirement on paper.

Pro Tip: Always confirm that your certificate is in the embassy-accepted format before purchasing. Some insurers provide visa-specific certificates on request, which are pre-formatted to match common embassy requirements. This small step saves significant time and reduces rejection risk.

For a clear breakdown of minimum insurance you need in 2026, you can review updated requirements before your application. Community experiences shared in discussions like this travel insurance advice thread also highlight real-world challenges applicants encounter, particularly for non-Schengen destinations where requirements can be less clearly published.

What happens if you do or don’t get travel insurance for your visa

Here is what you risk, and how to avoid it, by skipping or selecting inadequate travel insurance for your visa.

For Schengen applications, the outcome is binary. As confirmed by travel insurance rules across regions, travel insurance is required for Schengen with automatic rejection for non-compliance, strongly recommended for US and UK applications as a trust signal, and increasingly mandatory for a growing list of destinations including Georgia from 2026. For most non-Schengen tourist visas, it remains optional but increasingly advisable.

For non-mandatory visas, the consequences are less immediate but still real. Your application may face secondary questioning, additional document requests, or simply score lower on the officer’s informal assessment of your preparedness. In competitive or discretionary visa categories, these factors influence outcomes.

Use this checklist before submitting any visa application:

- Territory: Does the policy cover every country you will visit, including transit countries?

- Dates: Does the policy begin on or before your departure and end on or after your return?

- Coverage amounts: Does the medical cover meet the embassy’s stated minimum, in the stated currency?

- Document format: Is the certificate on official insurer letterhead with all required fields completed?

- Exclusions: Are there any exclusions that would leave you uncovered for foreseeable risks during your trip?

- Provider recognition: Is the insurer recognised and accepted by the embassy in question?

Reviewing the Schengen medical insurance essentials is a worthwhile step for any applicant preparing for a European trip, particularly those navigating the requirements for the first time.

Our take: The real reason travel insurance changes visa outcomes

Most guides stop at “insurance is required, here are the rules.” We want to offer a different perspective, because after working with international travellers and expats across dozens of visa types, we have seen what actually separates successful applications from rejected ones.

Travel insurance is the fastest visible signal of genuine intent. A visa officer reviewing your file in minutes needs quick evidence that you have planned responsibly. Your insurance certificate, if correctly formatted and clearly compliant, communicates in seconds that you are organised, financially prepared, and serious about your travel plans. It does more communicative work than almost any other single document in your file.

The price comparison is also striking. A two-week Schengen policy costs roughly €20 to €50 depending on your age and health. A visa rejection costs you the application fee, weeks of waiting, possible rebooking costs, and in some cases, reputational risk for future applications. The arithmetic is clear.

Requirements do shift. Georgia made insurance mandatory in 2026. Other nations may follow. A well-prepared applicant does not assume this year’s rules match last year’s. Checking the specific embassy website before each application takes ten minutes and eliminates a significant source of risk.

We also want to challenge the temptation to treat insurance as pure formality. When you buy the right policy, you are also protecting yourself from real financial harm during your journey. These goals are not separate. The right policy satisfies both. Our expat insurance tips reflect this philosophy, helping you find cover that works for both compliance and genuine security.

Ready to secure the right travel insurance for your visa?

As you prepare your visa documents, getting the insurance piece right is too important to leave to chance.

At Unparalleled Global Benefits, we specialise in insurance solutions tailored for international travellers, visa applicants, expats, and families living or working abroad. Whether you need cover that meets meeting global travel insurance rules or want to understand exactly how travel insurance protects you in practice, our resources are built around your real needs. You can also explore visitor visa health insurance options designed specifically for applicants seeking compliant, affordable plans. Do not let an avoidable insurance error stand between you and your visa approval.

Frequently asked questions

Is travel insurance always required for a visa?

No, it is mandatory for Schengen visas under Article 15 of the EU Visa Code, and for a growing list of destinations such as Georgia from 2026, but it is only recommended or optional for US, UK, and Canadian visitor visas unless a specific programme requires it.

What coverage is needed for a Schengen visa?

You must have at least €30,000 medical cover valid across all 29 Schengen states for the full duration of your stay, including emergency treatment, hospitalisation, and repatriation.

Does travel insurance improve my chances for US or UK visitor visas?

While not formally required, it demonstrates financial preparedness and responsible planning, both of which can positively influence a visa officer’s assessment of your application.

Can I get my travel insurance refunded if my visa is refused?

Some policies include a visa refusal refund clause that reimburses your premium, typically for around €15 to €35 for a Schengen policy, but insurance never covers the embassy’s visa application fee itself.

What happens if my insurance doesn’t match embassy requirements?

Your application can be rejected automatically for non-compliance, regardless of the strength of your other documents or your genuine travel intentions.

Recommended

- Why medical insurance is essential for visa applications – Unparalleled Global Benefits

- Get the right medical insurance for your visa: essential guide – Unparalleled Global Benefits

- Travel Insurance for Visa: Complete Expert Guide – Unparalleled Global Benefits

- Visa Travel Insurance: Why It Matters For Visa Holders – Unparalleled Global Benefits