TL;DR:

- Most failed overseas insurance claims result from avoidable documentation errors and missed pre-authorisation steps.

- Preparing and organizing digital copies of all necessary documents before treatment significantly increases claim success.

You are sitting in a foreign clinic, medical bill in hand, with no clear idea of what to do next. It is a scenario many expats face, and it is more stressful than it needs to be. Claiming on your overseas health insurance does not have to feel like a maze of paperwork and unanswered questions. This guide walks you through every stage of the process, from the moment you need care to the moment your claim is settled, so you can focus on what matters most: your recovery.

Table of Contents

- What to prepare before you claim

- Step-by-step process for overseas claims

- Direct billing vs reimbursement: choosing your best option

- What to expect after you submit your claim

- Why most expats lose out on overseas claims and how you can avoid their mistakes

- Explore global health insurance solutions for expats

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Document essentials | Gather all receipts, reports, and authorisations before submitting your overseas claim. |

| Choose claim method wisely | Understand whether direct billing or reimbursement is best for your care and convenience. |

| Appeal if denied | You can challenge denied claims by providing missing evidence within the deadline. |

| Expect 5–20 day turnaround | Most overseas insurance claims are processed within 5 to 20 working days if documents are correct. |

What to prepare before you claim

Before you even think about submitting a claim, getting your documentation in order is the single most important thing you can do. Insurers will not process a claim without the right paperwork, and missing one small item can delay your payout by weeks. Think of preparation as your first line of defence.

Documents you will typically need:

- Medical reports and discharge summaries from the treating doctor or hospital

- Itemised receipts and invoices for all treatments, consultations, and medications

- Completed claim forms supplied by your insurer (often downloadable from their portal)

- Proof of insurance such as your policy number and membership card

- Prescriptions and pharmacy receipts where applicable

- Bank account details for reimbursement payments

- Passport or ID copy if required for identity verification

It is also worth understanding the distinction between an emergency and a planned medical claim, because the process differs significantly. For medical emergency steps abroad, the rule is straightforward: seek treatment first, notify insurer as soon as possible via their 24/7 hotline. For planned procedures, you must obtain pre-authorisation, sometimes called a Guarantee of Payment (GOP), before the treatment takes place. Skipping this step for a non-emergency procedure is one of the most common and costly mistakes expats make.

Most insurers offer several ways to get in touch, including dedicated telephone hotlines, online portals, and mobile apps. Whichever channel you use, notify your insurer as early as possible. Timely notification is a contractual obligation in most policies, and late reporting can jeopardise your entire claim.

| Document type | Emergency claim | Planned claim |

|---|---|---|

| Medical report | Required | Required |

| Pre-authorisation (GOP) | Not always required | Mandatory |

| Itemised receipts | Required | Required |

| Completed claim form | Required | Required |

| Insurer notification timing | ASAP after treatment | Before treatment |

When filing insurance abroad, having digital copies of everything saves considerable time. Photographs of receipts, scanned reports, and PDF copies of forms can all be uploaded instantly to an insurer’s portal.

Pro Tip: Create a dedicated folder on your phone or cloud storage labelled with your policy number. Scan every receipt and medical document as it is issued. When it is time to claim, you will have everything in one place and will not be scrambling at a stressful moment.

Step-by-step process for overseas claims

With your documents ready, you can move confidently through the actual claim process. Whether you are dealing with a routine consultation or a hospitalisation, the core steps remain consistent.

- Receive treatment. Prioritise your health above all else. Keep every document the clinic or hospital provides.

- Notify your insurer. Contact them via hotline, app, or online portal as soon as reasonably possible. Confirm whether direct billing is available at your treating facility.

- Confirm the claim method. Establish whether you will use direct billing (the provider bills the insurer directly) or reimbursement (you pay upfront and claim back).

- Gather all required documents. Collect itemised invoices, medical reports, prescriptions, and any other items your insurer specifies.

- Complete the claim form. Download and fill in the insurer’s official claim form accurately. Errors here are a leading cause of delays.

- Submit your claim. Upload documents via the online portal or app, or post them if required. Note the submission date and any reference number issued.

- Track your claim. Use the insurer’s portal or app to monitor progress and respond promptly to any requests for additional information.

- Receive payment or confirmation. Once approved, reimbursements are typically transferred directly to your bank account.

Different insurers handle submissions differently. For medical procedures abroad, it is worth knowing your provider’s specific tools and timelines in advance. As an example, Cigna processes claims via an online portal or app within approximately 5 working days for straightforward cases, offers direct billing at partner facilities, and requires claims to be submitted within 12 months of treatment. Allianz and Bupa similarly offer apps and portals with direct billing networks. Knowing these specifics before you need to claim makes the whole experience far smoother.

| Submission method | Speed | Admin burden | Best suited for |

|---|---|---|---|

| Online portal | Fast | Low | Most claims |

| Mobile app | Very fast | Very low | Simple, routine claims |

| Post/mail | Slow | High | Insurers requiring originals |

| In-person (branch) | Variable | Medium | Complex or disputed claims |

If you are unsure about the step-by-step overseas claim process with your specific insurer, their customer service team or a broker can walk you through it. Do not guess, as assumptions are expensive when it comes to insurance.

Pro Tip: Always check your policy for the claim submission deadline. Most insurers, including Cigna, allow up to 12 months, but some require submission within 90 days of treatment. Missing this window means forfeiting your claim entirely.

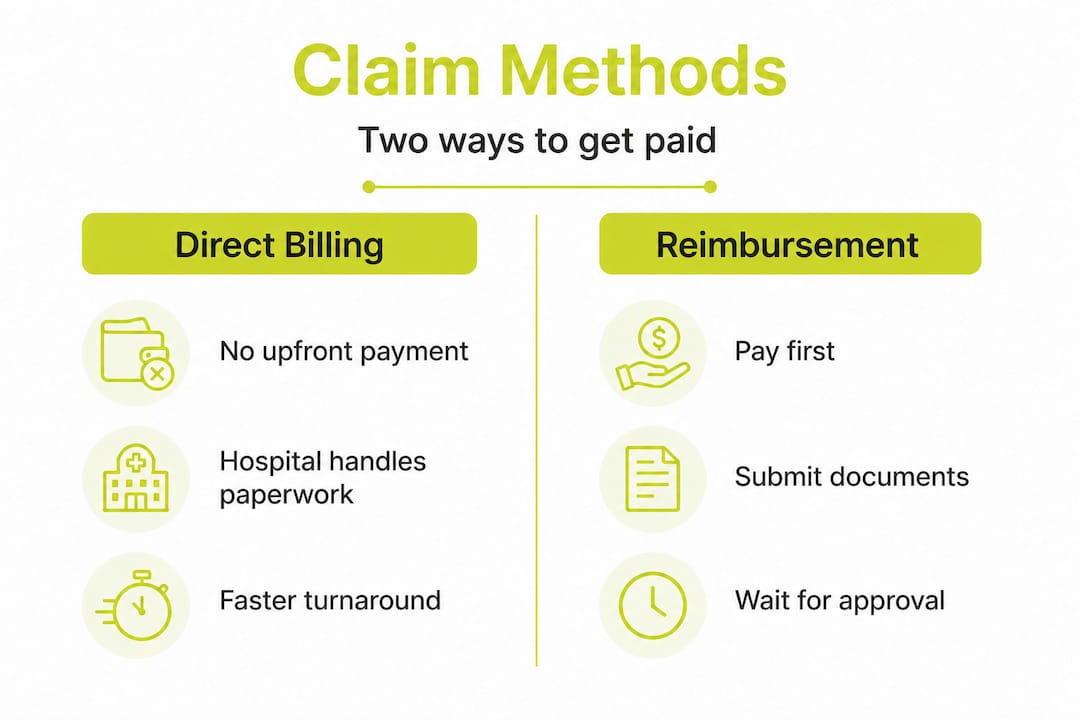

Direct billing vs reimbursement: choosing your best option

Two methods dominate overseas insurance claims, and understanding the difference between them is essential for every expat. Each has genuine advantages, and your choice will often depend on the circumstances of your treatment.

Direct billing means the hospital or clinic bills your insurer directly. You receive treatment, present your insurance card, and the provider handles the paperwork on your behalf. There is little or no upfront cost to you, which makes it particularly valuable during hospitalisations or expensive procedures. The limitation is that direct billing only works at facilities within your insurer’s approved network. If you visit a clinic outside that network, you will need to pay upfront and seek reimbursement instead.

Reimbursement gives you the freedom to visit virtually any licensed medical provider. You pay the bill yourself and then claim back the costs from your insurer. This is highly practical in countries where the insurer’s network is limited, or in emergency situations where you cannot check network status in advance. The trade-off is more administration: you need to gather every receipt, complete all claim forms yourself, and wait for the funds to be returned to your bank account.

“Reimbursement offers flexibility with any provider but comes with a significant admin burden; direct billing is seamless but network-limited. Brokers can assist with complex cases.”

Key considerations when choosing your method:

- Is the treating facility in your insurer’s network? If yes, direct billing is almost always the better choice.

- Do you have the funds available to pay upfront if needed? If not, it is worth calling your insurer before treatment to arrange a Guarantee of Payment.

- Is the claim complex, involving multiple providers or international specialists? An insurance broker can act as an intermediary and reduce your admin burden considerably.

- Have you kept all itemised receipts? Reimbursement claims without detailed receipts are regularly rejected or reduced.

Navigating coverage abroad can feel complex at first, but once you understand these two methods, you will approach any medical situation with far greater confidence. Many experienced expats actually use both methods at different times, choosing based on the nature of each treatment.

When comparing expat insurance plans before purchasing, pay close attention to the size of the direct billing network in your host country. A plan with a strong local network can save you significant time, money, and stress over the course of your time abroad.

What to expect after you submit your claim

Submitting your claim is not the end of the process. The post-submission phase requires your attention too, particularly if your insurer requests additional information or if there are unexpected delays.

![]()

Most major insurers aim to resolve straightforward claims quickly. Claims are typically processed within 5 to 20 working days, with appeals possible for denied claims by providing missing evidence, usually within 30 days of the initial decision. Complex claims involving hospital stays, specialist referrals, or multiple providers can take longer.

How to track your claim:

- Log in to your insurer’s online portal or app to check the claim status in real time.

- Save all email confirmations and reference numbers from the moment you submit.

- Respond promptly to any insurer requests for further documentation; delays on your side extend the processing time.

- If your insurer has a dedicated claims team, keep the direct contact number saved on your phone.

What to do if your claim is delayed:

- Contact the insurer directly and reference your claim number.

- Request a written explanation for the delay.

- Supply any additional documentation they require as quickly as possible.

What to do if your claim is denied:

- Read the denial notice carefully to understand exactly what was refused and why.

- Gather any missing or additional evidence that addresses the insurer’s concerns.

- Lodge a formal appeal, typically within 30 days of the denial notice.

- Consider engaging a broker or independent claims adviser if the situation is complex.

| Insurer type | Typical processing time | Appeal window |

|---|---|---|

| Major international (e.g., Cigna, Bupa) | 5 to 10 working days | 30 to 60 days |

| Regional international insurers | 10 to 15 working days | 30 days |

| Smaller or local providers | 15 to 20 working days | Varies |

For those doing insurance comparison steps before choosing a new policy, claims processing speed and the ease of the appeal process are worth weighing heavily alongside premium costs.

Pro Tip: Set a calendar reminder 25 days after submitting your claim. If you have not heard back or received payment by that point, follow up immediately. Do not wait until the appeal window closes before taking action.

Why most expats lose out on overseas claims and how you can avoid their mistakes

Here is something that rarely gets said directly: most failed overseas insurance claims are not the insurer’s fault. They result from predictable, avoidable errors made by the policyholder. That is uncomfortable to hear, but it is the most useful truth we can share with you.

The most common pattern we see is an expat who assumes the process is largely automatic. They receive treatment, pay the bill, and expect the claim to resolve itself. When it does not, they are caught off guard by requests for itemised receipts, pre-authorisation forms, or documents they never knew they needed. By then, deadlines have passed and the claim cannot be salvaged.

Small documentation errors are the single biggest cause of claim failure. A receipt that lists a lump sum rather than itemised costs, a medical report that omits a diagnosis code, or a claim form with a minor error in the policy number can all result in rejection. These are not deliberate obstacles. They are standard requirements that the insurer communicates in the policy documents, which most people do not read until something goes wrong.

Pre-authorisation is another area where expats consistently underestimate the stakes. If your policy requires a Guarantee of Payment for specialist consultations or planned procedures, and you proceed without one, you may be personally liable for the entire bill. The insurer is within their rights to decline, and no amount of appeals will change that outcome.

Our advice is to build a digital claim kit before an emergency happens. This means saving your policy documents, your insurer’s hotline number, the claims portal URL, and a copy of your membership card all in one accessible location. Learn your insurer’s app or portal now, not at 2am in a foreign hospital. Spend fifteen minutes exploring the features so that when you need it, you are not navigating it for the first time under pressure.

Getting insured abroad is an essential step, but the real value of your insurance only materialises if you claim it successfully. Treat your policy as a tool you need to learn how to use, not simply a document you file away and forget.

Explore global health insurance solutions for expats

Managing overseas insurance claims is much easier when you have the right plan from the start.

At Unparalleled Global Benefits, we help expats find international coverage that is built around their actual circumstances, including policies with strong direct billing networks, transparent claims processes, and genuine support when it matters. Whether you are researching your first expat policy or reviewing your current coverage, our guide to international expat health insurance is a practical starting point. You can also explore our essential expat insurance tips for broader guidance on protecting your health and finances abroad. When you are ready to compare providers, our overview of top international insurers offers a clear, unbiased reference point.

Frequently asked questions

Can I claim overseas insurance for treatment at any hospital?

You can submit a reimbursement claim for treatment at most licensed providers, but direct billing is limited to hospitals and clinics within your insurer’s approved network.

How long do overseas insurance claims take to process?

Most major international insurers process claims within 5 to 20 working days, provided all required documents are submitted correctly from the outset.

What if my claim is denied or delayed?

You can appeal a denied claim by supplying any missing or additional evidence, and most insurers allow you to do this within 30 days of the original decision.

Is pre-authorisation always required for overseas claims?

Pre-authorisation is mandatory for planned treatments under most policies; however, for emergencies, treatment comes first and insurer notification should follow as soon as possible afterwards.

Can a broker help if my claim gets complicated?

Absolutely. Brokers assist with complex claims by acting as an intermediary between you and the insurer, which is particularly valuable when documentation requirements or appeal processes become involved.

Recommended

- How to File Insurance Claim Abroad: Step-by-Step Guide – Unparalleled Global Benefits

- Step-by-step guide to expat insurance: secure global cover – Unparalleled Global Benefits

- How to Submit Insurance Claims: A Complete Step-by-Step Guide

- How to advise expat insurance: 5 steps for reliable cover – Unparalleled Global Benefits

- Servicios para expatriados en España – Lexmovea

- Philippines document attestation guide for UAE expats