TL;DR:

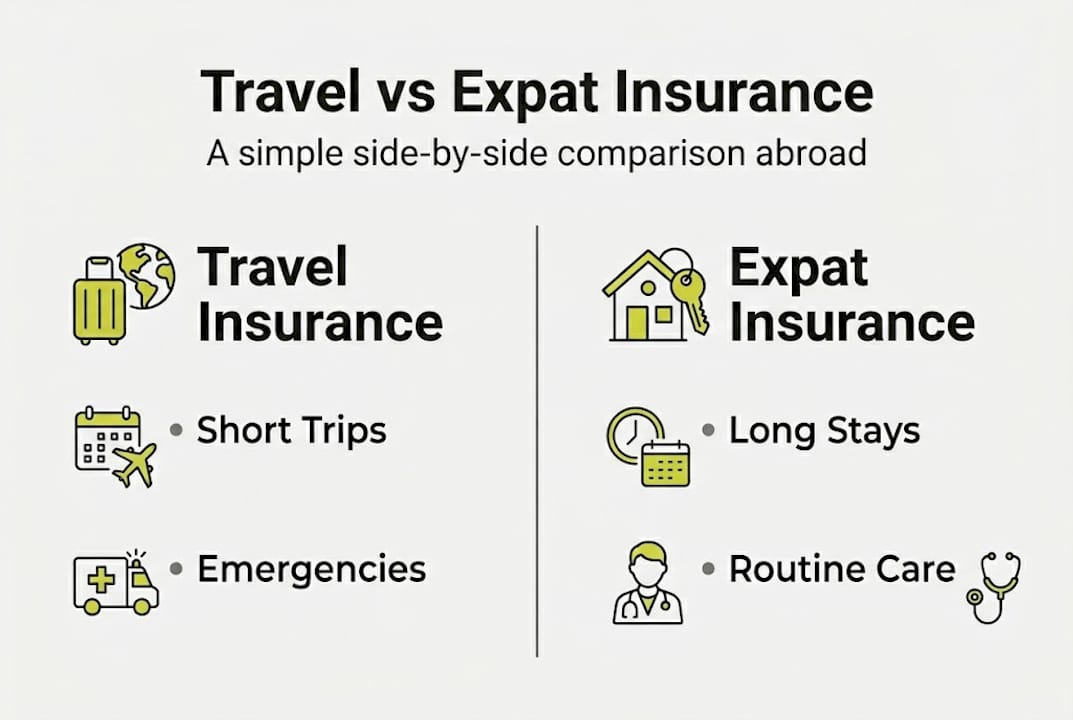

- Travel insurance is for short-term trips and lacks routine or long-term health coverage.

- Expat insurance offers comprehensive, long-term healthcare tailored for extended stays and visa compliance.

- Choosing the right policy depends on duration, healthcare needs, family, and local regulations.

Travel vs expat insurance: choose the right cover abroad

Choosing the wrong insurance policy when living or travelling abroad can cost you far more than the premium difference. Many people assume that the travel insurance policy they use for a fortnight’s holiday will protect them equally well during a year-long relocation or an extended stay in South-East Asia. It will not. The gap between travel insurance and expat insurance is significant in terms of cost, scope, and the kind of protection each one actually provides. This guide breaks down exactly what each policy covers, how they compare, and how you can make a confident, informed decision before you go.

Table of Contents

- What is travel insurance and how does it work?

- What is expat insurance and how does it work?

- Travel vs expat insurance: key differences at a glance

- How to choose: practical considerations for your journey

- A fresh perspective: why the right insurance matters more than you think

- Explore your insurance options with confidence

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Travel insurance covers emergencies | Travel insurance is best for short trips and provides protection mainly for unexpected medical and travel mishaps. |

| Expat insurance protects routine care | Expat insurance offers comprehensive cover for ongoing health, chronic conditions, and meets visa requirements for longer stays. |

| Cost and scope differ greatly | Travel insurance is much cheaper, but expat insurance offers broader benefits and is essential for long-term expatriation. |

| Digital nomads need careful planning | Nomads may start with travel insurance but should upgrade to expat cover if staying over six months or needing routine healthcare. |

| Check visa and government rules | Always verify your destination’s requirements and never rely solely on travel insurance for residency or legal compliance. |

What is travel insurance and how does it work?

Travel insurance is a short-term policy designed to protect you during a temporary trip away from your home country. Think of it as a safety net for the unexpected: a sudden illness, a missed flight, stolen luggage, or a cancelled hotel. It is not built for routine healthcare, ongoing medical conditions, or extended stays abroad. Understanding this distinction early will save you from a costly misunderstanding later.

Most standard travel insurance policies provide cover across a fairly predictable set of categories:

- Emergency medical treatment including hospitalisation and evacuation

- Trip cancellation or interruption due to unforeseen events

- Lost, stolen, or delayed baggage

- Personal liability in the event of accidental damage or injury to others

- Accidental death or disability benefits

What travel insurance typically does not cover is equally important to understand. Routine GP visits, ongoing prescriptions, dental check-ups, pre-existing conditions (in most cases), and mental health support for chronic issues are generally excluded. If you travel with an existing condition and need regular medication or monitoring, a standard travel policy is unlikely to help you.

You can learn more about basic travel insurance cover to understand exactly what a typical policy includes before making any assumptions.

The cost of travel insurance is relatively accessible. Annual plans average around $298, while digital nomad-style monthly travel plans typically range between $45 and $120 per month. These figures make travel insurance attractive to short-term travellers, and rightly so. But they also reflect the limited scope of the cover involved.

“Travel insurance is designed for emergencies during temporary travel, not as a substitute for health insurance. It does not cover routine or preventive care abroad.” This is the consistent position of public health advisors and insurers alike, and it is a critical point if you plan to stay abroad for several months.

Pro Tip: If you are comparing policies and wondering whether travel insurance overlaps with your existing domestic health plan, read our breakdown of travel insurance vs health insurance to avoid gaps in your coverage.

One common trap is treating travel insurance as a flexible, extendable product. Most policies cap coverage at 30 to 180 days. Extending a travel policy repeatedly is not the same as holding a proper long-term expat plan. The cover weakens, exclusions accumulate, and some providers will refuse renewal once a claim has been made. For a holiday or a short business trip, travel insurance is entirely appropriate and usually sufficient. For anything longer or more settled, you need a fundamentally different kind of policy.

What is expat insurance and how does it work?

Expat insurance, also referred to as international health insurance or expatriate health cover, is designed for individuals who are relocating abroad, living in a foreign country for an extended period, or working overseas on assignment. It is a long-term product that mirrors the kind of comprehensive healthcare access you would expect from a domestic health plan, but structured for use internationally.

The key difference lies in what expat insurance covers on a routine, ongoing basis. A well-structured expat plan typically includes:

- Inpatient and outpatient cover including routine consultations and specialist referrals

- Chronic and pre-existing condition management (subject to underwriting)

- Mental health support including therapy and psychiatric care

- Dental and optical cover (often available as add-ons)

- Maternity and newborn benefits

- Prescription drugs and ongoing medication costs

- Emergency evacuation and repatriation

This breadth of cover is particularly important if you are relocating with family, managing a health condition, or planning to stay in a country where local public healthcare is inaccessible or of limited quality for foreigners. You can explore the full range of types of expat insurance to understand which plan structure suits your circumstances.

Expat insurance also plays a critical role in visa compliance. Many countries require proof of adequate health insurance as part of the residency or long-stay visa application process. A travel policy is often not accepted for this purpose. Countries like Germany, the Netherlands, and Thailand specify minimum cover requirements, and only qualifying expat health plans meet those standards.

The cost reflects this higher level of protection. Expat insurance typically costs between $150 and $600 per month, or roughly $3,000 to $9,000 annually, depending on your age, the region of cover, and your chosen deductible. Including the United States in your coverage area adds a notable 40 to 80 per cent to the premium, given the high cost of American healthcare.

Pro Tip: If you will not be spending significant time in the USA, excluding it from your coverage region can reduce your expat insurance premium substantially. Speak to a provider to understand which regions are included by default before selecting a plan. Reviewing a thorough expat health insurance guide will help you identify the most relevant options.

The underwriting process for expat insurance is also more detailed. Insurers will ask about your medical history, current conditions, and sometimes require a medical questionnaire or GP report. This is not unusual and should not discourage you from applying, but it does mean that starting the process early before your departure date is strongly advisable. Many expat health insurance plans offer modular structures, meaning you can build the level of cover you need rather than paying for benefits you will not use.

Travel vs expat insurance: key differences at a glance

With both types now clearly defined, a direct comparison helps you see which one fits your situation. The differences are substantial, not just in price, but in fundamental purpose and scope.

| Feature | Travel insurance | Expat insurance |

|---|---|---|

| Duration of cover | Days to 6 months | 1 year or more |

| Routine medical care | Not covered | Covered |

| Emergency cover | Yes | Yes |

| Pre-existing conditions | Usually excluded | Manageable with underwriting |

| Visa compliance | Rarely accepted | Often qualifies |

| Dental and optical | Emergency only | Available as add-ons |

| Monthly cost range | $45 to $120 | $150 to $600 |

| Mental health cover | Very limited | Standard or add-on |

| Maternity benefits | Not included | Available with waiting period |

The distinction becomes especially important when you consider digital nomads and remote workers. Travel insurance may suffice for short stays, but it consistently fails for stays exceeding six months. Many countries with digital nomad visa programmes require a minimum level of health cover, such as €30,000 for Schengen area entry or $50,000 for Thailand, and a basic travel policy often falls short of those thresholds.

Who needs which policy? Here is a simple numbered breakdown:

- Short-term holidaymakers (up to 30 days): Travel insurance is appropriate and cost-effective.

- Business travellers on frequent short trips: An annual multi-trip travel policy works well.

- Expats relocating for work or family (1 year or more): Expat insurance is essential, as government guidance from the CDC confirms.

- Students studying abroad for a semester: Travel insurance may cover emergencies but expat plans offer better routine access.

- Digital nomads on rolling stays: A hybrid may work initially, but transitioning to expat cover is recommended for sustainability.

- Families with children relocating abroad: Expat insurance is strongly recommended to cover paediatric care and schooling-related medical needs.

For a detailed side-by-side review, our expat insurance comparison and the difference between health and travel insurance pages offer thorough guidance. It is also worth reviewing the state department insurance guidance to understand what the US government advises its citizens travelling internationally, regardless of your nationality.

How to choose: practical considerations for your journey

Knowing the differences is one thing. Applying that knowledge to your specific situation is another. Your decision should be based on a combination of practical factors, and it is worth considering each one carefully before committing to a policy.

Key factors to weigh before choosing:

- Length of stay abroad: Anything under three months favours travel insurance; beyond six months, expat insurance becomes necessary.

- Routine healthcare needs: Do you take regular medication or see a specialist? Expat insurance is the only option that will cover these costs ongoing.

- Family cover requirements: If you are travelling with children or a partner, routine care becomes far more critical.

- Visa requirements: Research your destination’s insurance requirements before selecting a policy, not after.

- Access to local healthcare: Some countries have excellent public systems that accept residents; others require fully private arrangements.

Pro Tip: Always verify the specific insurance requirements for your destination country’s visa or residency permit before purchasing any policy. Some countries specify minimum benefit amounts, cover types, or even named insurers. Government advice on insurance abroad is a reliable starting point alongside your destination country’s official immigration portal.

Here is a practical decision table to guide your choice:

| Your situation | Recommended cover |

|---|---|

| Holiday under 4 weeks | Travel insurance |

| Work assignment 3 to 6 months | Travel or short-term expat plan |

| Relocation for 1 year or more | Expat insurance |

| Digital nomad under 6 months | Travel or nomad hybrid plan |

| Digital nomad over 6 months | Expat insurance |

| Family relocating abroad | Expat insurance with family cover |

| Student exchange (one semester) | Travel or student-specific plan |

Common mistakes to avoid include assuming your employer-sponsored cover at home extends abroad (it rarely does beyond brief trips), and choosing the cheapest policy without checking whether it meets visa requirements. Another frequent error is purchasing travel insurance and then extending it multiple times in lieu of obtaining a proper expat plan. For digital nomad insurance specifically, the nuances around visa compliance and rolling stays require careful attention.

When it comes to selecting an expat insurance provider, look for network size, claims processing speed, multilingual support, and whether the provider has experience in your destination country. Reviewing a digital nomad visa guide is also useful if your stay involves a specific visa category, as requirements differ widely. If you are planning to move abroad and need help understanding what health cover to arrange before departure, our resource on move abroad health insurance is a helpful starting point.

A fresh perspective: why the right insurance matters more than you think

Most people underestimate the financial and legal consequences of choosing the wrong type of cover. It is not just about whether a hospital will treat you. It is about whether you will be reimbursed, whether you will be deported for non-compliance with visa rules, and whether a pre-existing condition will leave you with tens of thousands of pounds in uncovered costs.

Both the State Department and the CDC guidance for long-term travellers are explicit: supplemental or expat insurance is essential for extended stays, and travel insurance should not be assumed to provide routine care under any circumstances. Yet thousands of travellers make exactly that assumption every year.

Digital nomads face a particular blind spot. The appeal of flexible, month-to-month travel plans is understandable. But these plans rarely satisfy visa conditions, and they leave gaps in routine care that accumulate quietly until a health issue forces the point. Hybrid approaches have their place, but they are genuinely transitional tools, not sustainable long-term solutions.

Our expert expat insurance comparison makes clear that the right policy is one that matches your actual situation, not the one that looks most affordable at the checkout. Reviewing your expatriate insurance choices with a clear head and accurate information will protect your health, your finances, and your legal standing abroad.

Explore your insurance options with confidence

Understanding the difference between travel and expat insurance is genuinely empowering. You are now equipped to ask the right questions, check the right requirements, and choose a policy that actually fits your life abroad.

At Unparalleled Global Benefits, we specialise in helping travellers, expats, families, and digital nomads find the right international insurance cover for their specific circumstances. Whether you are ready to choose expat insurance that meets your visa requirements, explore the full scope of international expat health coverage, or compare solutions from our network of top insurance providers, we are here to guide you every step of the way. Your peace of mind starts with the right policy.

Frequently asked questions

Is travel insurance enough for long-term stays abroad?

No. Travel insurance is built for short trips and does not cover routine care or meet the visa compliance requirements needed for long-term residency, as confirmed by government sources.

How much does expat insurance cost compared to travel insurance?

Travel insurance is considerably cheaper, with annual plans averaging around $298 compared to expat insurance, which typically costs between $3,000 and $9,000 per year depending on age, deductible, and coverage region.

Do digital nomads need expat insurance or travel insurance?

For stays under six months, a travel or hybrid plan may work, but nomads staying longer or requiring routine care should transition to expat insurance to ensure legal compliance and adequate ongoing cover.

Are government agencies recommending expat insurance for long stays?

Yes. Both the CDC and the State Department advise that expat insurance is essential for individuals relocating abroad for a year or more, as travel insurance cannot substitute for ongoing health coverage.

Recommended

- Types of expatriate insurance: smart cover choices abroad – Unparalleled Global Benefits

- Understanding expat insurance: benefits, cover, and what you need – Unparalleled Global Benefits

- Why expats need travel insurance: Essential protection – Unparalleled Global Benefits

- Selecting The Right “Expat Insurance Provider”