TL;DR:

- International health insurance offers global coverage, portability, and evacuation benefits essential for expats.

- Local plans are limited in scope, benefits, and do not typically cover pre-existing conditions or evacuations.

- Choosing the right plan involves assessing mobility, health needs, regional requirements, and future changes.

Moving abroad is one of life’s biggest decisions, and your health cover should match that scale. Many expats assume travel insurance or a local plan will be enough to protect them overseas, but that assumption can be costly. Medical emergencies abroad can easily exceed £80,000, and being underinsured is far more common than most people realise. This guide explains exactly why international health insurance, also known as international private medical insurance or _(i)PMI_**, delivers a level of protection that no short-term travel plan or locally issued policy can match, and how you can make the smartest choice for your circumstances.

Table of Contents

- The unique risks expatriates face abroad

- What sets international health insurance apart

- International vs local and travel insurance: a clear comparison

- Cost, claims, and the true value of international health insurance

- How to choose international health insurance: practical steps

- What most expats get wrong about health insurance abroad

- Find the right international health insurance for your needs

- frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Worldwide protection | International health insurance ensures seamless coverage across borders for true freedom and security. |

| Evacuation and emergencies | IPMI protects expats from catastrophic costs of evacuation and emergency care, often not covered by local plans. |

| Better benefits and renewability | Global policies offer higher limits and lifetime renewability, unlike most local or travel plans. |

| Meets legal requirements | International health insurance can satisfy visa or residency rules required in many countries. |

The unique risks expatriates face abroad

Living abroad brings excitement, but it also brings a distinct set of health risks that most expats underestimate until it is too late. From sudden accidents and acute illness to the management of ongoing chronic conditions, your health needs do not pause because you have crossed a border. Yet many expats still rely on cover that was simply not designed for long-term overseas life.

Consider some key vulnerabilities expats face:

- Access to quality care varies dramatically between countries, particularly in developing regions.

- Language barriers can delay diagnosis and treatment, especially in emergencies.

- Limited benefit caps on local plans leave you exposed to large out-of-pocket costs.

- No policy portability means your cover stops the moment you leave your host country.

- Group travel risks are magnified when travelling between multiple countries for work or family.

The data underlines just how exposed expats can be. 1 in 6 travellers make a claim, with medical issues accounting for 42% of all claims, and illness affecting 50 to 75% of those spending time in developing countries. These are not rare events. They are statistically likely outcomes of an international lifestyle.

Local insurance plans are cheaper, but as research shows, they lack portability, higher limits, and evacuation cover and are only suitable for expats on long-term stays in countries with strong local healthcare systems who do not travel frequently. For everyone else, local cover creates a dangerous gap. Understanding wellness abroad starts with knowing which type of cover actually fits your life.

“The risk is not just financial. Being stuck in a foreign hospital without the right cover means delays, language difficulties, and decisions made under pressure.”

Pro tip: Always declare pre-existing conditions when applying for any policy. Non-disclosure is the single most common reason claims are denied, and the consequences abroad can be severe.

Exploring the types of expat insurance available is a sensible first step before committing to any plan. With these hidden risks in mind, let us examine what makes international health insurance uniquely robust.

What sets international health insurance apart

International private medical insurance is built from the ground up for people who live, work, or move across borders. It is not a stretched version of a domestic plan. It is an entirely different product designed around global mobility. Here is what genuinely sets it apart.

Understanding global coverage means recognising that worldwide portability is the foundation of any strong international policy. You remain covered whether you are in Singapore, South Africa, or Spain. You do not need to re-apply each time you move, and your medical history travels with you.

Key distinguishing features of international health insurance include:

- Pre-existing condition coverage: Many international plans will cover declared pre-existing conditions, subject to underwriting, unlike most local or travel policies which exclude them entirely.

- Emergency evacuation and repatriation: International plans include evacuation to the nearest appropriate facility or back to your home country, a benefit rarely found in local plans.

- Direct billing: Leading international insurers maintain private hospital networks globally, meaning you often do not pay upfront and claim back later.

- Travel medical insurance add-on modules allow you to tailor cover for short trips alongside your core annual plan.

- Policy portability: Your cover remains valid across multiple countries with no gaps.

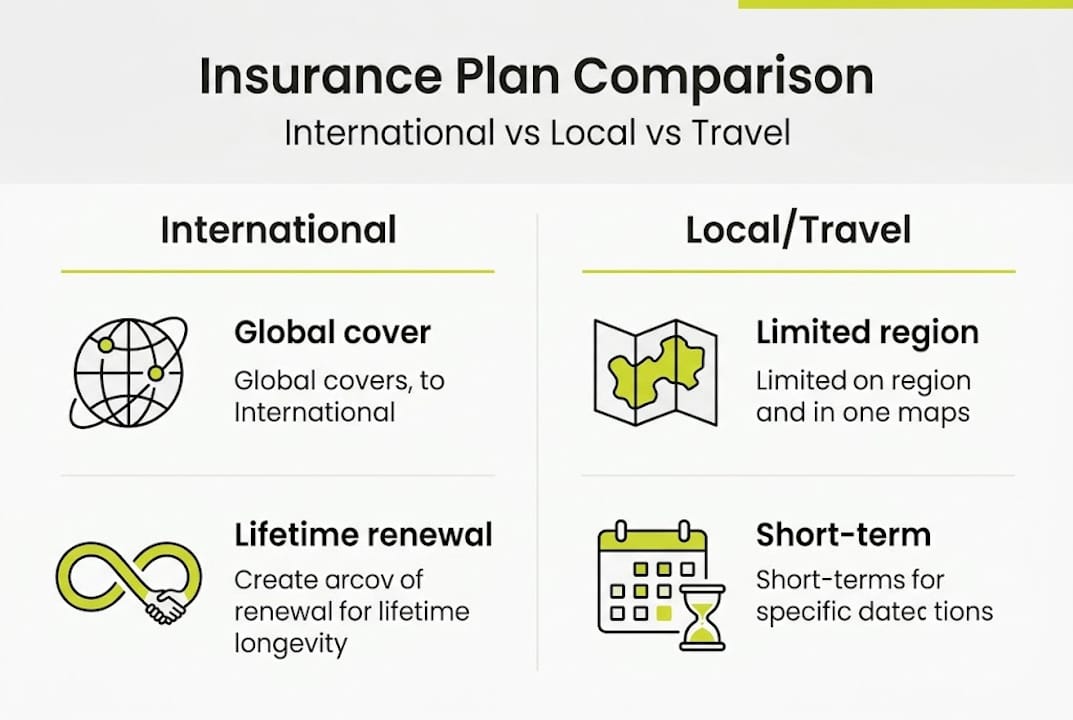

| Feature | International health insurance | Local insurance | Travel insurance (short-term) |

|---|---|---|---|

| Geographic scope | Global | National only | Short trip only |

| Policy portability | Yes | No | No |

| Emergency evacuation | Yes | Usually no | Sometimes |

| Pre-existing conditions | Often covered | Usually excluded | Usually excluded |

| Direct billing network | Yes | Limited | Limited |

| Annual renewability | Yes, lifelong | Age caps apply | Not renewable |

With over 15,000 medical evacuations arranged annually by leading international insurers, and an average claim value of $5,200, the financial case for robust cover is clear. With a clear view of the unique benefits, it is important to directly weigh international health insurance against other options. You can also compare international insurance plans side by side before deciding.

International vs local and travel insurance: a clear comparison

Choosing between international, local, and travel insurance is one of the most consequential decisions you will make as an expat. Getting it wrong does not become obvious until something goes wrong.

International health plans offer higher benefit limits and lifetime renewability compared to local plans, which typically impose age caps and sublimits on specific treatments. This matters enormously if you develop a serious condition while abroad.

| Insurance type | Best for | Cover duration | Pre-existing conditions | Vision and dental options |

|---|---|---|---|---|

| International (i)PMI | Mobile expats, families | Annual, renewable | Often available | Usually available |

| Local plan | Long-term settled residents | Annual | Usually excluded | Limited |

| Travel insurance | Short trips (under 6 months) | Per trip | Usually excluded | Not covered |

Here are the top reasons expats upgrade to international health insurance:

- Their travel policy expired after 180 days and they were left uninsured.

- A local plan refused to cover a pre-existing condition they did not consider significant.

- They needed treatment in a neighbouring country and discovered local cover did not apply.

- A medical evacuation was required that local cover would not fund.

- They relocated again and had to start over with new local insurance.

Additionally, international health insurance is the only product that meets visa and residency requirements in countries like the UAE and Thailand, where proof of approved cover is mandatory. Travel insurance does not satisfy these requirements in most cases.

You can compare expat health cover in detail, or read about how to secure care abroad in plain terms. Claims statistics consistently show that medical emergencies, not cancellations, are the costliest and most frequent events for people living internationally.

Pro tip: If you do not plan to spend time in the United States, excluding USA coverage from your international plan can reduce your premium by 30 to 50%. It is one of the most effective ways to manage cost without sacrificing quality. Now that you can clearly see the differences, let us explore how costs and financial protection compare in real scenarios.

Cost, claims, and the true value of international health insurance

For many expats, the instinctive objection to international health insurance is cost. But the question is not whether it is expensive. The question is what the alternative actually costs you.

Medical emergencies abroad can exceed £80,000 in total costs, with average international claims sitting around $5,200. In markets like Dubai, individual annual premiums reached $5,896 in recent reporting, a figure that sounds significant until you weigh it against a single hospitalisation. Family plans typically cost around $17,670 annually in that same market. You can review international coverage for expats to understand regional cost variations in more detail.

“The gap between what expats expect and what they actually receive is where the real risk lives.”

The numbers confirm this concern. 39% of expats expect international cover through their employer or existing arrangement, but only 32% actually receive it, leaving a meaningful proportion exposed without knowing it. That 7% gap represents thousands of people facing potential financial hardship.

Common financial risks of being underinsured abroad:

- Emergency surgery and hospital stays in private facilities.

- Medical repatriation flights, which can cost tens of thousands alone.

- Long-term specialist care for conditions developed while abroad.

- Lost income during extended recovery without adequate support.

The benefits of expat cover go beyond just paying bills. They include access to better facilities, faster treatment, and the peace of mind that comes from knowing exactly what you are covered for before something happens. With a full understanding of costs and protection, let us apply this to your unique expat journey.

How to choose international health insurance: practical steps

With so many options available, finding the right plan requires a structured approach. Here is how to evaluate your situation clearly.

- Define your mobility profile. Are you settled in one country, or do you move regularly? Mobile expats and digital nomads almost always benefit from international (i)PMI, while those in stable, low-cost healthcare markets may consider local options.

- Review your health profile. Include any chronic conditions, medications, or pending treatments when comparing plans. Always declare everything honestly.

- Consider regional exclusions. Do you need USA coverage? Or are you focused on Europe, Asia, or Latin America? This shapes your premium significantly.

- Check visa requirements. Some countries mandate specific levels of health cover. Match your policy to those requirements.

- Plan for transitions. If you started as a frequent traveller, research shows the best time to transition to international cover is within 6 to 12 months of becoming a long-term expat.

Key questions to ask before purchasing any plan:

- Does the policy renew annually with no lifetime cap on benefits?

- Are pre-existing conditions covered, and under what underwriting terms?

- Is emergency evacuation and repatriation included as standard?

- Can I use the policy across multiple countries if I relocate again?

- Does the insurer offer direct billing in my host country?

Pro tip: Set a reminder to review your cover every year, particularly after major life changes such as marriage, a new child, a serious illness, or a change in country of residence. Cover that was adequate last year may leave significant gaps today.

For tailored guidance on the best insurance for working abroad, you can compare leading plans from established providers and compare local and international cover side by side. Let us conclude with an expert perspective on what most expats still get wrong, even after reading the facts.

What most expats get wrong about health insurance abroad

After working with expats across dozens of markets, we have seen the same pattern repeat itself. People wait until a crisis to discover their cover was never adequate. By then, the financial and emotional cost is already compounded.

Many expats believe that local insurance will suffice because the healthcare system in their host country appears strong. But as evidence shows, local plans can work for certain settled expats, yet most overestimate system strengths and underestimate their own mobility needs. A single relocation, an unexpected trip for family reasons, or a diagnosis requiring specialist care abroad exposes the limits of a locally bound policy immediately.

The real cost of underinsurance is not just money. It is the stress of navigating an unfamiliar health system without support, the delay in receiving appropriate care, and the burden of decisions made under pressure in a foreign country.

Global mobility requires resilient protection, not a patchwork of short-term policies. If your expat situation changes, your cover must change with it. Review the essentials of expat protection every time your circumstances shift, not just at renewal.

Pro tip: Always reassess your insurance whenever your expat situation shifts, whether it is a new country, a new employer, or a new stage of life. The policy that served you well at 35 may be entirely inadequate at 45.

Find the right international health insurance for your needs

You now have a clear picture of why international health insurance is the most reliable form of protection for expats and frequent international travellers. The next step is finding the plan that fits your specific situation.

At _(u)nparalleled Global Benefits_**, we make it straightforward to understand, compare, and secure the right level of cover. Whether you are exploring your options for the first time or looking to upgrade from a local plan, our resources and specialist guidance are here to help. Browse the full range of types of expat insurance or review our curated selection of top insurers to take your next step with confidence.

frequently asked questions

Is international health insurance required for all expats?

Many countries now require proof of international health insurance for visa or residency approval, though requirements vary by destination. Countries such as the UAE and Thailand, for example, mandate approved health cover as part of the visa application process.

How much does international health insurance typically cost?

Premiums for individuals typically range from $3,000 to $10,000 a year depending on coverage region and age. In markets like Dubai, individual premiums reached $5,896 annually, while family plans averaged $17,670.

What is the difference between travel insurance and international health insurance?

Travel insurance covers emergencies on short trips and expires quickly, while international health insurance provides year-round, renewable cover including routine care, chronic illness management, and policy portability across multiple countries.

Can I switch from local to international insurance after moving abroad?

Yes, and many expats do exactly that. Research shows that transitioning to international cover within 6 to 12 months of becoming a long-term expat tends to provide the smoothest transition and broadest protection.

Does international health insurance cover pre-existing conditions?

Cover for pre-existing conditions depends on the provider and the underwriting terms applied. International plans tend to be more flexible than local plans and can often include declared conditions, particularly for expats with clean medical histories.

Recommended

- Global health insurance explained: cover worldwide in 2026 – Unparalleled Global Benefits

- Why International Health Insurance is Essential for Every Global Traveler

- International Health Insurance Explained: Complete Guide – Unparalleled Global Benefits

- What does international health insurance cover? 2026 guide – Unparalleled Global Benefits

- Navigating Workers’ Compensation Insurance for Travelers with DiamondBack Insurance: Instant, Efficient, and Comprehensive – Diamondback Insurance – Solutions with Instant Online Quotes