TL;DR:

- Proper preparation and timely action are essential to ensure continuous expat health coverage.

- Review, update, and compare policies carefully before renewing to avoid gaps and unexpected costs.

- Treat renewal as an active process, not a passive obligation, to maintain adequate and ongoing protection.

Renewing your expat medical insurance can feel surprisingly stressful. You are living or working abroad, managing a busy schedule, and suddenly your policy renewal date is looming. Miss it, and you could face a gap in cover that leaves you exposed to significant medical costs with no safety net. The stakes are real: a single hospitalisation abroad without active cover can cost tens of thousands of pounds. This article walks you through exactly what to check before renewing, how to complete the process step by step, how to troubleshoot common problems, and what to do once your new policy year begins.

Table of Contents

- What to check before renewing your expat medical insurance

- Step-by-step guide to renewing expat medical insurance

- Troubleshooting common renewal challenges

- What to expect after renewal: coverage verification and next steps

- The uncomfortable truth: why most expats underestimate the renewal process

- Renew with confidence: explore expert resources for expats

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Prepare ahead | Start the renewal process early to prevent gaps in your cover and ensure all eligibility requirements are met. |

| Compare and reassess | Use renewal as a chance to review providers, benefits, and exclusions for the best fit for your current needs. |

| Understand cancellation rules | Know your insurer’s cooling-off and refund policy before committing to a renewed term. |

| Verify your cover | Always check your new policy documents and activation status immediately after renewal. |

What to check before renewing your expat medical insurance

Preparation is everything when it comes to renewing your international health policy. Many expats treat renewal as a formality, but taking a few focused hours beforehand can save you from costly surprises or gaps in protection.

Gather your key documents first. Before you log in to your insurer’s portal, pull together your current policy documents, your passport or national ID, and any updates to your medical history from the past year. If you have had a new diagnosis, started a new medication, or undergone surgery, your insurer needs to know. Failing to disclose changes can invalidate a future claim.

Next, check your eligibility. Understanding annual renewal basics is essential, because policies are renewable indefinitely if premiums are paid on time, though some insurers impose age limits for new applicants, typically at 65 or 70. If you are already insured, you are generally protected from these cut-offs at renewal, but it is worth confirming with your provider.

Reassess your coverage needs honestly. Has your family situation changed? Are you now living in a different country, or travelling to regions not covered by your current plan? Did you use your mental health or dental benefits last year? These questions matter because your lifestyle in 2026 may look quite different from when you first took out the policy.

Finally, consider whether you want to stay with your current provider or switch. Switching is possible, but it carries a real risk: you may lose continuity on pre-existing condition exclusions that your current insurer had agreed to waive.

Here is a summary of what most major insurers require at renewal:

| Requirement | Details |

|---|---|

| Valid ID | Passport or national ID |

| Medical history update | Any new diagnoses or treatments |

| Current policy number | Found on your existing policy documents |

| Premium payment method | Credit card, bank transfer, or direct debit |

| Residency confirmation | Proof of current country of residence |

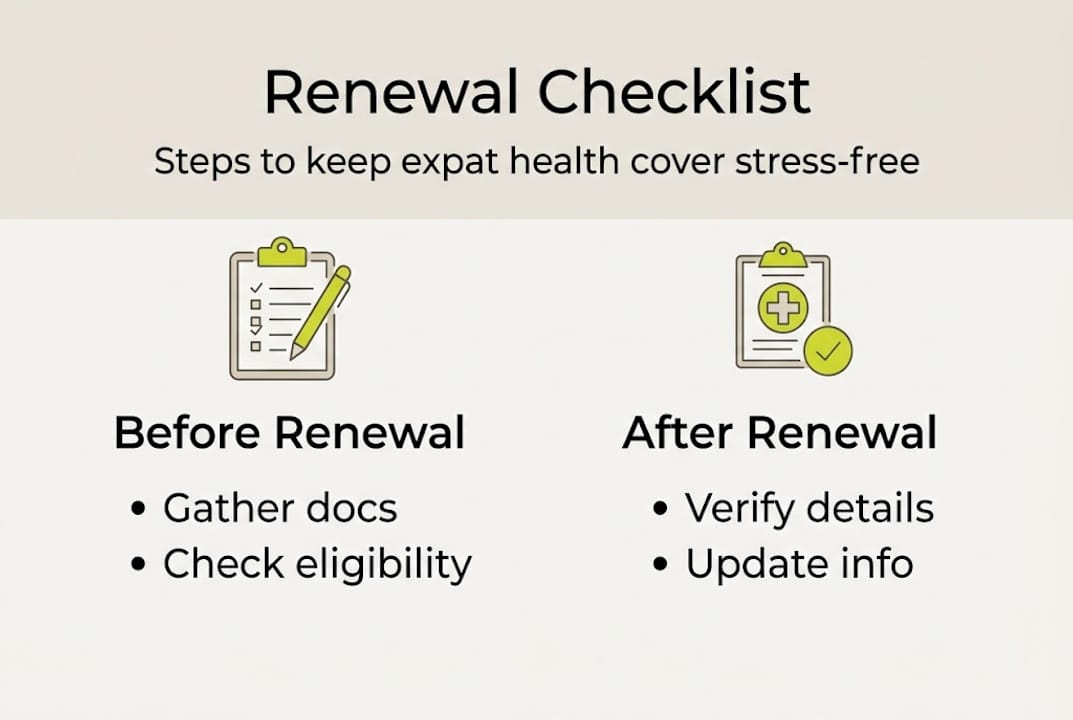

Key items to prepare before renewal:

- Current policy documents and ID

- Updated medical history and prescription list

- Confirmation of countries you will live in or visit

- Family details if adding or removing dependants

- Bank or payment details for premium settlement

Pro Tip: Set a calendar reminder at least four weeks before your renewal date. This gives you enough time to gather documents, compare options, and avoid any last-minute rush that could result in a lapsed policy.

Step-by-step guide to renewing expat medical insurance

Once you have checked your documentation and assessed your needs, completing the renewal itself is straightforward if you follow a clear process.

- Log in to your insurer’s online portal. Most major providers, including Cigna, Allianz Care, and Aetna, have dedicated renewal sections. Review the renewal offer carefully before accepting anything.

- Update your personal and health details. If anything has changed since last year, update it now. This protects you if you need to make a claim later in the policy year.

- Review the renewal quote. Premiums often increase at renewal, sometimes significantly. Compare your quote with at least two other providers before committing. Exploring types of expat insurance can help you understand what alternatives are available.

- Compare with other providers if needed. Use a specialist broker or a trusted resource for comparing international plans to ensure you are getting fair value.

- Accept the offer and pay your premium. Once satisfied, confirm your renewal and pay. Save your payment receipt and confirmation email immediately.

- Check your new policy documents. Confirm the start and end dates, your coverage limits, and any changes to exclusions or benefits.

One critical detail many expats overlook is the cooling-off period. Cooling-off periods range from 14 to 30 days for a full refund if no claims have been made, with Cigna offering 14 days and Allianz Care offering 30 days. After this initial window, mid-term cancellations rarely result in a pro-rata refund.

| Insurer | Cooling-off period | Refund policy |

|---|---|---|

| Cigna Global | 14 days | Full refund, no claims made |

| Allianz Care | 30 days | Full refund, no claims made |

| Aetna International | 14 days | Full refund, no claims made |

| Bupa Global | 14 days | Full refund, no claims made |

Important: Never allow your cover to lapse, even for a single day. A gap in coverage means any medical event during that period is entirely your financial responsibility, and some conditions arising during a lapse may be treated as pre-existing when you re-enrol.

Troubleshooting common renewal challenges

Even with careful preparation, expats frequently encounter problems during renewal. Knowing what to expect means you can resolve issues quickly rather than letting them escalate.

Delayed or missing renewal communications are more common than you might think. Insurers send renewal notices by email, post, or both, but messages get lost in spam folders or sent to outdated addresses. Always log in directly to your provider’s portal around 60 days before expiry to check your renewal status rather than waiting passively for a letter.

Premium increases can be a shock. Insurers adjust premiums based on your age, claims history, and regional healthcare cost inflation. If your quote has risen sharply, do not accept it automatically. Contact your insurer to ask for a breakdown and consider adjusting your excess (the amount you pay before the insurer covers costs) to bring the premium down.

Age-related restrictions can affect renewal terms, even for existing policyholders. Some insurers introduce additional exclusions or sub-limits once you reach certain age brackets. Read your renewal offer letter carefully for any such changes.

Switching providers is always an option, but the risks are real. Changing insurer at renewal may cause you to lose continuity on exclusions your current provider had agreed to waive over time. Before making the move, read the new insurer’s terms on pre-existing conditions very carefully. Resources for choosing a new provider and reviewing expat insurance comparisons can make this decision much clearer.

Pro Tip: Never let your cover lapse, even for a single day. If you are between providers, consider a short-term travel health policy to bridge the gap.

Common reasons expats lose continuity of cover:

- Missing the renewal deadline due to outdated contact details

- Failing to update payment information before the premium is due

- Assuming renewal is automatic without active confirmation

- Switching providers without checking exclusion continuity terms

- Not reading the renewal offer for benefit or exclusion changes

Most of these problems are entirely avoidable with a simple renewal checklist and a proactive approach. The expats who struggle most at renewal are those who treat it as a passive process rather than an active one.

What to expect after renewal: coverage verification and next steps

With renewal complete, confirming that your cover is genuinely active is your immediate priority. Do not assume everything is in order simply because you have paid.

Verify your policy is active. Log in to your insurer’s app or portal and confirm your new policy start date, membership number, and coverage limits. Save your emergency assistance number in your phone. This is the number you call if you need urgent medical care abroad, and having it readily accessible could be critical.

Review what has changed in your new policy year. Insurers adjust benefits, exclusions, and coverage limits annually. Policies renew indefinitely for existing policyholders who keep premiums current, but the terms can shift. Read the renewal schedule of benefits carefully, paying attention to any new sub-limits on specialist consultations, mental health, or dental care.

Here are the steps to take immediately after renewal:

- Download and save your new policy documents to a secure cloud folder.

- Confirm your new policy number matches what appears in the insurer’s app.

- Update your emergency contact card with the new membership number.

- Check the understanding your product section of your insurer’s website for any benefit changes.

- Set a reminder for 60 days before your next renewal date.

| Verification step | What to check | How to do it |

|---|---|---|

| Policy start date | Matches your renewal confirmation | Check portal or app |

| Membership number | Correct on all documents | Cross-reference email and portal |

| Coverage limits | No unexpected reductions | Read schedule of benefits |

| Exclusions | Any new conditions added | Review renewal letter carefully |

| Emergency number | Saved and accessible | Store in phone and wallet card |

If you spot an error, contact your insurer immediately in writing. Keep a record of all correspondence. Most errors can be corrected quickly, but delays in reporting them can complicate matters if a claim arises.

The uncomfortable truth: why most expats underestimate the renewal process

Here is something we have observed consistently: experienced expats, people who have lived abroad for years and navigated complex visa systems, often treat insurance renewal as the least important item on their to-do list. They assume it is automatic. It is not.

Renewal is the single best opportunity you have each year to improve your plan, correct outdated information, and review exclusions before a health change catches you unprepared. Waiting until the last week before expiry means you have no time to compare providers, negotiate terms, or correct errors. A rushed renewal is a poor renewal.

Our view is straightforward: treat your renewal date the way you treat a passport expiry. Mark it early, act on it deliberately, and use it as a prompt to review whether your current cover still fits your life. The full health insurance guide we have put together covers this in greater depth, but the principle is simple. Your health cover is not a set-and-forget arrangement. It is a living document that should grow with your circumstances.

Renew with confidence: explore expert resources for expats

Renewing your expat medical insurance does not need to be stressful, but it does require the right support and information. Specialist guidance makes a genuine difference, particularly when you are weighing up whether to stay with your current provider or explore alternatives.

At Unparalleled Global Benefits, we have built resources specifically for expats navigating these decisions. Whether you are looking to understand your wellness abroad, explore options for protecting your health abroad, or compare offerings from top insurers, our platform gives you the clarity you need to make a confident, well-informed renewal decision. Your health cover deserves more than a quick click.

Frequently asked questions

Can I renew my expat medical insurance if I’m over 65?

Many insurers do not offer new policies to those over 65 or 70, but if you are already covered, renewal remains possible provided premiums are paid on time. Always confirm the age terms in your specific policy.

What happens if I change insurer at renewal?

Switching providers at renewal may cause you to lose continuity for pre-existing condition exclusions, so review the new insurer’s terms on this point carefully before committing.

Is there a refund if I cancel my policy right after renewal?

Most major insurers offer a 14 to 30 day cooling-off period during which you can receive a full refund, provided no claims have been submitted.

How can I prevent a gap in my expat health coverage?

Set calendar reminders at least 60 days before your renewal date, verify your provider’s communications regularly, and aim to complete renewal at least two weeks before your policy expires to avoid any gap in cover.

Recommended

- Expat health insurance: your complete guide for 2026 – Unparalleled Global Benefits

- International Expat Health Insurance: Protecting Your Wellness Abroad – Unparalleled Global Benefits

- Affordable Expat Insurance: Flexible Solutions for Every Global Lifestyle

- Types of expat insurance: protect health abroad in 2026 – Unparalleled Global Benefits

- How to Handle Expatriate Tax Returns | Filing Expatriate Tax Returns