Many expats make the same costly assumption before relocating for work: that their existing travel policy will cover them. It will not. Travel insurance is short-term and emergency-only, designed for holidays and brief trips, not for the realities of living and working in another country. If you are preparing to move abroad for a job, a contract, or a long-term professional opportunity, you need cover that matches the full scope of your new life. This guide walks you through every step, from understanding your options to avoiding the mistakes that leave expats exposed.

Table of Contents

- Why insurance for working abroad is essential

- Understanding your international insurance options

- What to look for in a good policy: essential features and extras

- How much does international insurance cost? Breaking down the price

- Navigating pre-existing conditions and exclusions

- Insider tips for securing and maintaining the right cover

- Find your perfect insurance plan for working abroad

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Travel cover is not enough | You need proper expat insurance with full cover for international work. |

| Shop early and compare | Start comparing plans at least 30 days before your move for best results. |

| Know your needs | Consider your health, family, and destination when choosing features and limits. |

| Disclose pre-existing conditions | Tell your insurer everything to avoid claim denials and policy issues. |

| Avoid common mistakes | Don’t rely on myths—cover visa rules and actual medical needs for safe work abroad. |

Why insurance for working abroad is essential

Relying on travel insurance when you work abroad is one of the most common and expensive mistakes expats make. Most travel policies cap out at 30 to 90 days, exclude work-related activities, and will not pay for routine care, specialist consultations, or ongoing treatment. The difference between health and travel insurance is significant, and misunderstanding it can leave you with bills running into tens of thousands of pounds.

The risks of being underinsured abroad are real and varied:

- Denied care: Some hospitals in popular expat destinations require proof of valid insurance before admitting non-emergency patients.

- Out-of-pocket costs: A single hospitalisation in the United States or Singapore can cost more than £50,000 without adequate cover.

- Visa complications: Many countries now require proof of comprehensive health insurance as part of the work permit or visa application process.

- No repatriation cover: Travel policies rarely include medical evacuation or repatriation, which can cost £20,000 or more.

“Travel insurance is not a substitute for the comprehensive expat health insurance that working abroad genuinely demands.”

As the international health insurance insights from industry experts confirm, expat policies are built for work and life abroad, covering far more than emergencies. Understanding the travel insurance vs health insurance distinction is the first step to protecting yourself properly. For a broader overview of your options, the expat travel health insurance guide is an excellent starting point.

Understanding your international insurance options

Not all international policies are the same, and choosing the wrong type can be just as problematic as having no cover at all. The main categories you will encounter are:

- International Private Medical Insurance (IPMI): The gold standard for working expats. These plans provide comprehensive cover for in-patient and out-patient care, emergency treatment, and often dental and vision, across multiple countries.

- Local health insurance: Purchased in your destination country. Can be cost-effective but may not cover you if you travel regionally or return home.

- Travel insurance: Suitable only for short visits. Not appropriate for anyone working abroad for more than a few weeks.

The right choice depends on your situation. A corporate assignee on a two-year contract needs something very different from a freelance digital nomad or a family relocating permanently. Reviewing the types of expat insurance available helps you match your circumstances to the right plan.

| Plan type | Best for | Flexibility | Typical coverage |

|---|---|---|---|

| IPMI | Long-term workers, families | High | Comprehensive |

| Local plan | Single-country residents | Low | Moderate |

| Travel insurance | Short trips only | Medium | Emergency only |

| Digital nomad plan | Freelancers, remote workers | High | Core medical |

Top providers in this space include Cigna Global, Allianz Care, Aetna International, BUPA Global, and SafetyWing for digital nomads, each with distinct strengths. For a detailed breakdown, the international expat health insurance resource covers what separates leading plans. You can also consult the international health insurance guide for a wider market perspective.

What to look for in a good policy: essential features and extras

Once you know which type of plan suits you, the next step is evaluating individual policies. Some features are non-negotiable; others are valuable extras worth paying for.

Core features every working expat needs:

- In-patient hospitalisation and surgery

- Out-patient consultations and diagnostics

- Emergency medical treatment and evacuation

- Repatriation cover

- Prescription medication

Desirable extras to consider:

- Dental and vision care

- Maternity cover (especially important for families)

- Mental health support

- Wellness and preventive care

Pay close attention to policy limits, sub-limits, and exclusions. A plan may advertise £1 million in annual cover but cap out-patient care at £5,000 per year. That gap matters. Also check whether your destination country or visa category requires a minimum level of cover, as many do. The best insurance for working abroad comparison can help you assess plans side by side.

Premiums are shaped by several factors: your age, your health history, the region you are moving to, and the deductible (excess) you choose. As premium factors show, getting quotes 30 to 45 days before departure gives you time to compare properly and gather any required documents. The guide on how to navigate medical coverage abroad confidently offers further practical advice on this process.

Pro Tip: Always read the exclusions section before signing. A policy that excludes your most likely health risks is not a bargain, regardless of the premium.

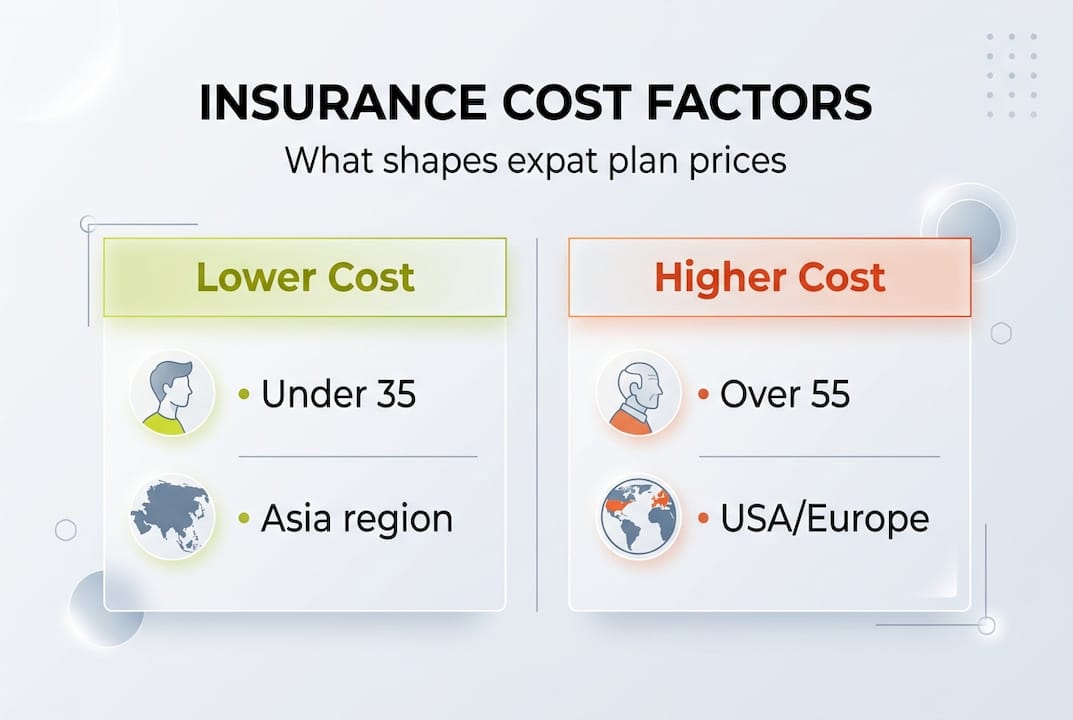

How much does international insurance cost? Breaking down the price

International health insurance for expats typically costs between $150 and $600 per month, depending on age, coverage area, deductible, and plan type. That is a wide range, and where you fall within it depends on several variables.

| Factor | Lower cost | Higher cost |

|---|---|---|

| Age | Under 35 | Over 55 |

| Region | South-East Asia | USA or Western Europe |

| Deductible | High excess | Low or zero excess |

| Coverage scope | Core only | Comprehensive with extras |

| Pre-existing conditions | None | Multiple conditions |

Digital nomads and younger professionals often find affordable options in the $150 to $250 range with plans from providers like SafetyWing or Cigna’s modular offerings. Families and older expats moving to high-cost regions should budget closer to $400 to $600 monthly. Choosing the cheapest plan without checking what it actually covers is a false economy. Use the compare health care insurance for expats tool to weigh cost against genuine value, and review the international insurance plans for expats comparison for a structured overview.

Navigating pre-existing conditions and exclusions

Pre-existing conditions are one of the most misunderstood areas of expat insurance. Insurers define them broadly: any illness, injury, or treatment you have experienced before your policy start date qualifies. How they handle these conditions varies considerably.

The three main approaches are:

- Full exclusion: The condition is permanently excluded from your cover. You pay all related costs out of pocket.

- Moratorium underwriting: The condition is excluded initially but may be covered after a set period (usually two years) without symptoms or treatment.

- Full medical underwriting: You disclose everything upfront, and the insurer decides whether to cover, exclude, or load (charge extra for) the condition.

As coverage options for pre-existing conditions confirm, full medical underwriting gives you the clearest picture of what you are actually covered for. Always disclose your full medical history. Omitting information, even unintentionally, can void your policy at the worst possible moment. Review the international insurance plans for expats comparison to see how different providers approach this.

Pro Tip: Before applying, compile a complete list of any medications, diagnoses, or treatments from the past five years. Having this ready speeds up the application and reduces the risk of accidental omission.

Insider tips for securing and maintaining the right cover

Timing and preparation make a significant difference when applying for international insurance. Common mistakes expats make include relying on travel insurance, overlooking pre-existing condition cover, and failing to check visa insurance requirements before departure. Avoiding these errors starts with a clear plan.

Key steps to follow before you move:

- Apply 30 to 45 days before your departure date to allow time for underwriting and document collection.

- Gather your full medical records, a list of current prescriptions, and any specialist letters.

- Confirm your destination country’s visa insurance requirements and ensure your policy meets the minimum thresholds.

- Check whether your employer provides any group cover and what gaps remain.

- Set a calendar reminder for your renewal date and review your policy annually, especially if your family situation or health changes.

Pro Tip: If your visa requires proof of insurance, request a formal coverage letter from your insurer. Many embassies and consulates will not accept a policy document alone. The guide on how to navigate medical coverage abroad confidently covers exactly what documentation you will need.

Find your perfect insurance plan for working abroad

You now have a clear picture of what working abroad insurance involves, what it costs, and how to choose wisely. The next step is finding a plan that fits your specific circumstances, whether you are a solo professional, a family relocating together, or a digital nomad moving between countries.

At Unparalleled Global Benefits, we specialise in matching expats and international professionals with the right cover for their unique situations. Explore our international expat health insurance options, read our detailed expat health insurance guide for practical guidance, and browse the full range of types of expat insurance we support. Request a personalised quote today and move abroad with genuine confidence.

Frequently asked questions

Do I really need more than travel insurance if I’m working abroad?

Yes. Travel insurance is emergency-only and designed for short trips, not for the ongoing medical, legal, and visa demands of working abroad. Comprehensive expat health insurance is essential.

How soon before my move should I apply for international insurance?

Apply 30 to 45 days before departure. This window allows time for underwriting, document collection, and resolving any queries before you leave, as pre-departure timing guidance recommends.

What’s the average cost of insurance for expats or professionals?

Plans typically cost between $150 and $600 per month. Your age, health, destination country, and chosen level of cover all influence where your premium falls within that range.

How are pre-existing conditions handled?

Providers use three main approaches: full exclusion, moratorium underwriting, or full medical underwriting. Always disclose your complete history, as pre-existing condition options vary significantly between insurers.

What mistakes do expats make with insurance?

Common expat errors include relying on travel insurance for long stays, failing to disclose pre-existing conditions, and not verifying that their policy meets the insurance requirements of their destination country’s visa.

Recommended

- Working Holiday Travel Insurance: Essential Protection Abroad – Unparalleled Global Benefits

- Best Insurance for Working Abroad – Expert Comparison 2025 – Unparalleled Global Benefits

- Evaluate StaySure expat insurance: comprehensive cover abroad – Unparalleled Global Benefits

- Insurance for Living Abroad – Ensuring Global Security – Unparalleled Global Benefits

- Warum Reiseversicherungen für Disneyreisen unverzichtbar sind – 2000-reisen