Surprisingly, up to 40% of flight cancellations are excluded from standard flight insurance policies. This gap leaves many international travellers and expatriates vulnerable to significant financial losses when disruptions occur. Understanding exactly what your flight insurance covers, and crucially what it doesn’t, is essential before departing on any international journey. This guide breaks down coverage fundamentals, common exclusions, and special considerations for those living abroad.

Table of Contents

- Introduction To Flight Insurance Coverage

- Understanding Core Coverage Components

- Common Exclusions And Limitations

- Common Misconceptions About Flight Insurance

- Comparative Analysis Of Coverage Options

- Special Considerations For Expatriates

- Claim Processes And Documentation Essentials

- Timing And Purchase Considerations

- Find The Right Flight Insurance For Your Needs

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Coverage scope | Flight insurance addresses specific risks including cancellations, delays, medical emergencies, and baggage loss, but many policies exclude voluntary changes and certain delay causes. |

| Purchase timing | Buying insurance within days of booking is crucial for trip cancellation coverage, as delayed purchases often lead to claim denials. |

| Expatriate needs | Long-term travellers require extended coverage periods, repatriation benefits, and seamless integration with international health insurance. |

| Claim requirements | Successful claims demand thorough documentation including boarding passes, airline notifications, and medical reports submitted within 30 to 60 days. |

| Policy variations | Basic plans offer lower limits and longer delay thresholds, whilst comprehensive options provide higher coverage and broader medical evacuation benefits. |

Introduction to flight insurance coverage

Flight insurance protects against financial loss due to trip cancellations, delays, medical emergencies, and baggage issues. For international travellers and expatriates, this specialised coverage addresses the unpredictability inherent in global mobility. Whether you’re relocating abroad for work or embarking on an extended holiday, flight disruptions can cost thousands of pounds without proper protection.

The insurance landscape offers four main coverage categories tailored to different travel risks. Each category serves a distinct purpose and operates under specific conditions that determine when and how much you’ll receive in reimbursement.

Core coverage types include:

- Trip cancellation and interruption protection: Reimburses non-refundable expenses when you must cancel or cut short your journey for covered reasons

- Flight delay compensation: Provides reimbursement for accommodation, meals, and essential purchases during extended delays

- Medical emergency coverage: Covers urgent healthcare costs, evacuation, and repatriation expenses whilst travelling abroad

- Baggage protection: Compensates for lost, stolen, or significantly delayed luggage, typically with per-item and total claim limits

Understanding these categories forms the foundation for selecting appropriate coverage. Each type addresses specific scenarios you might face during international travel. Knowing which situations trigger coverage versus those that don’t can save you considerable expense and frustration.

For comprehensive guidance on available providers, explore top flight insurance providers to compare coverage options suited to your travel profile.

Understanding core coverage components

Trip cancellation coverage reimburses your non-refundable flight costs, accommodation deposits, and prepaid tour expenses when covered events force you to cancel. Covered reasons typically include serious illness, injury, death of a family member, natural disasters affecting your destination, or mandatory work obligations. The reimbursement percentage varies by policy, with most comprehensive plans covering 100% of eligible expenses up to the policy limit.

Flight delay benefits typically activate after a threshold delay of 3 to 6 hours, depending on the policy terms. Once this threshold passes, you can claim reimbursement for reasonable expenses such as meals, accommodation, and essential toiletries. Basic policies often require six-hour delays before compensation begins, whilst premium options may start coverage after just three hours.

Medical emergency coverage becomes invaluable when facing health crises abroad. This component covers hospitalisation, emergency treatment, prescription medications, and crucially, medical evacuation to appropriate facilities. For expatriates and long-term travellers, repatriation coverage ensures transport back to your home country if local medical facilities cannot provide necessary care. Some policies include coverage exceeding £100,000 for medical evacuation alone.

Baggage coverage addresses two scenarios: permanently lost luggage and significantly delayed bags. Permanently lost items typically receive reimbursement based on depreciated value, with per-item limits ranging from £250 to £1,000. Delayed baggage coverage activates after 12 to 24 hours, providing funds for essential purchases until your belongings arrive. Always photograph valuable items and keep receipts to support potential claims.

Pro tip: Review medical evacuation limits carefully if travelling to remote destinations where emergency transport costs can exceed £50,000.

For broader protection details, consult travel insurance coverage details to understand how different policy components work together.

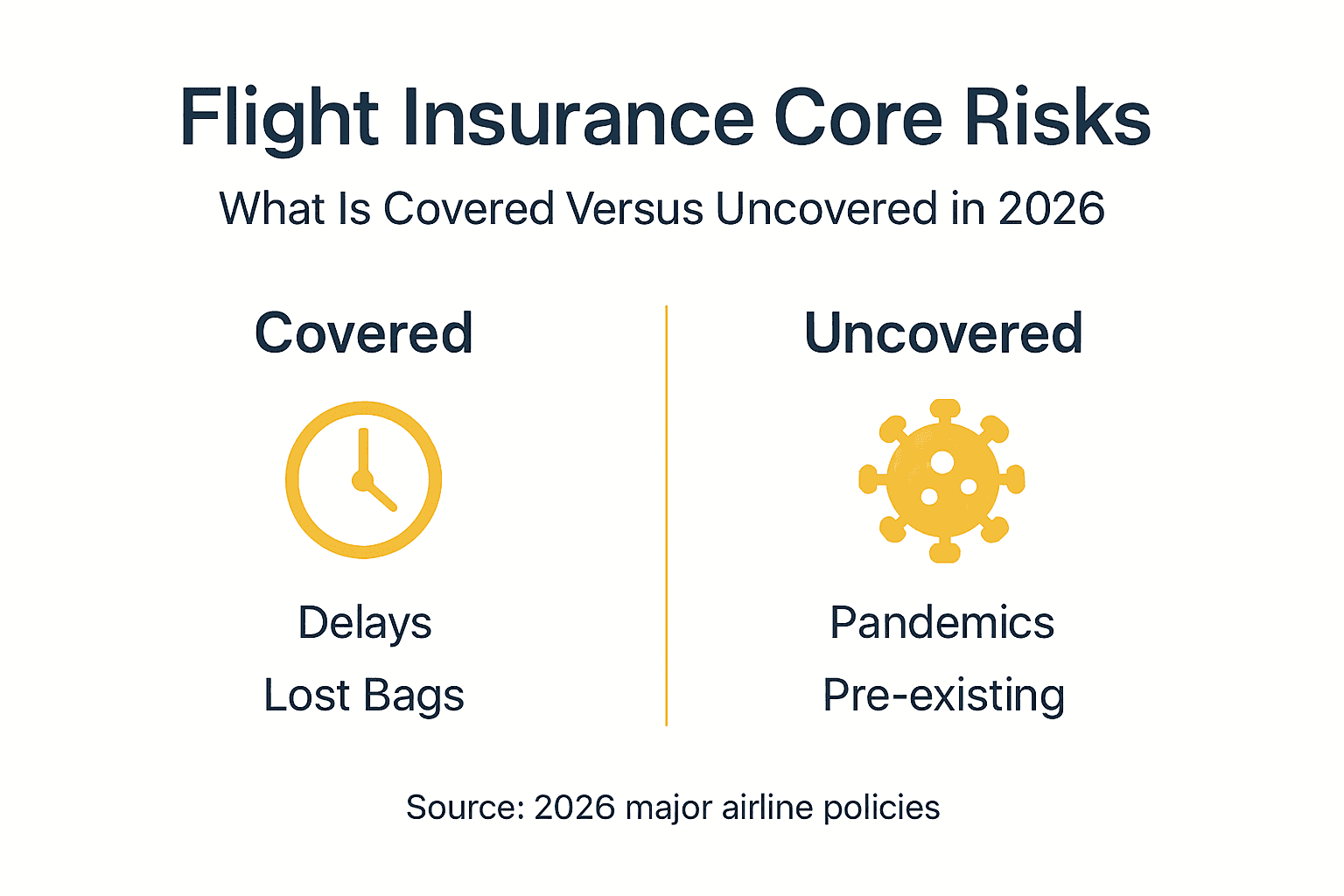

Common exclusions and limitations

Policies often exclude pre-existing medical conditions, pandemics, government restrictions, and voluntary schedule changes. These exclusions represent the most common reasons for claim denials and warrant careful attention before purchasing any policy. Understanding what’s not covered prevents unpleasant surprises when filing claims.

Pre-existing medical conditions typically include any illness, injury, or health issue for which you received treatment, diagnosis, or medication within 60 to 180 days before purchasing insurance. Many insurers offer pre-existing condition waivers if you purchase coverage within 14 to 21 days of making your initial trip deposit. Without this waiver, any claims related to known health issues will be denied regardless of severity.

Pandemic and government restriction exclusions have become increasingly common since 2020. Most standard policies now exclude cancellations or delays caused by disease outbreaks, border closures, or mandatory quarantine requirements. Specialist pandemic coverage exists but requires separate purchase and comes with higher premiums and stricter conditions.

Voluntary changes and traveller errors receive no coverage:

- Deciding to cancel your trip for convenience or preference

- Missing your flight due to late arrival at the airport

- Changing plans because of work schedule conflicts not classified as mandatory emergencies

- Cancelling because of dissatisfaction with accommodation or airline service

Delay coverage excludes situations within your control, such as arriving late to the departure gate or failing to allow sufficient connection time between flights. Carrier-caused mechanical issues and weather delays usually qualify for coverage, but you must demonstrate the delay duration met policy thresholds.

Pro tip: Always disclose pre-existing conditions during application, as non-disclosure can void your entire policy, not just condition-related claims.

Common misconceptions about flight insurance

Many travellers mistakenly believe that all flight disruptions automatically trigger insurance payouts. This misconception leads to denied claims and frustration when policies don’t perform as expected. Clearing up these misunderstandings helps set realistic expectations for coverage.

Not all flight disruptions are covered; medical emergencies may require separate insurance; timing of purchase affects eligibility. Here are the most prevalent misunderstandings:

-

Universal delay coverage: Policies don’t cover every delay or cancellation. Delays caused by your actions, such as arriving late or inadequate connection times, receive no compensation. Only delays meeting minimum duration thresholds and caused by qualifying events trigger benefits.

-

Comprehensive medical protection: Flight insurance provides limited emergency medical coverage, often capped at £10,000 to £25,000. This amount may prove insufficient for serious medical emergencies abroad. Comprehensive travel health insurance offers superior medical protection with higher limits and broader coverage.

-

Flexible purchase timing: Waiting too long after booking eliminates eligibility for trip cancellation coverage. Most policies require purchase within 7 to 21 days of your initial trip deposit. Late purchases may still cover delays and baggage issues but won’t reimburse cancellation costs.

-

Interchangeable coverage types: Flight insurance and travel health insurance serve different purposes. Flight coverage focuses on trip-related financial losses, whilst health insurance addresses medical care needs. Expatriates particularly need both types working together for complete protection.

Understanding these distinctions prevents overestimating your coverage and helps you identify gaps requiring additional insurance products. Always read policy terms carefully before purchasing to confirm coverage aligns with your specific travel risks and requirements.

Comparative analysis of coverage options

Basic flight insurance offers lower limits and shorter delay thresholds, whereas comprehensive plans provide higher coverage limits and broad medical evacuation benefits. This comparison helps you understand the value differences between policy tiers and select appropriate coverage.

| Coverage feature | Basic plans | Comprehensive plans |

|---|---|---|

| Trip cancellation limit | Up to £5,000 | Up to £50,000 |

| Delay compensation threshold | 6 hours | 3 hours |

| Medical emergency coverage | £10,000 to £25,000 | £100,000 to £500,000 |

| Medical evacuation | Not included or limited | £100,000+ included |

| Baggage loss limit | £500 to £1,000 | £2,500 to £5,000 |

| Pre-existing condition waiver | Rarely available | Often available with timely purchase |

| Policy duration | Up to 30 days | Up to 12 months |

Basic plans suit short trips with modest non-refundable expenses where you accept higher risk thresholds. These policies cost 3% to 5% of trip value but provide minimal protection for serious situations. The six-hour delay threshold means you’ll cover most short delays out of pocket.

Comprehensive plans become essential for:

- Trips with significant non-refundable deposits exceeding £5,000

- Travel to destinations with limited medical facilities

- Extended journeys lasting several months

- Situations where medical evacuation might prove necessary

For expatriates, policy duration and repatriation options matter most. Long-term coverage prevents gaps that could leave you unprotected during extended stays abroad. Repatriation benefits ensure you can return home for treatment if local facilities cannot provide adequate care for serious conditions.

Explore comprehensive travel insurance options designed specifically for extended international stays and expatriate needs.

Special considerations for expatriates

Expatriates often require extended coverage durations, repatriation benefits, and seamless integration with international health insurance plans. Living and working abroad creates unique insurance needs that differ significantly from typical holiday travel coverage.

Longer policy periods accommodate extended international assignments ranging from several months to multiple years. Standard 30-day travel policies prove inadequate for expatriate situations. Look for annual or multi-year policies that cover unlimited trips or continuous residence abroad. These policies typically renew automatically and adjust coverage as your circumstances evolve.

Repatriation and medical evacuation become critical for expatriates facing serious health emergencies. Local medical facilities may lack equipment, specialists, or treatment protocols available in your home country. Comprehensive evacuation coverage ensures transport to appropriate care facilities regardless of cost. This benefit alone can exceed £250,000 for evacuations from remote locations or developing countries.

Key expatriate requirements include:

- Flexible coverage that adapts to changing travel patterns and residency status

- Coordination between flight insurance and primary international health coverage to prevent gaps

- Family coverage options when relocating with dependents

- Emergency assistance services available 24/7 in multiple languages

Integration with existing health plans prevents duplicate coverage whilst ensuring no protection gaps. Your flight insurance should complement rather than overlap with your primary health insurance. Review both policies together to understand how they interact during emergencies.

Explore comprehensive guides including international travel medical insurance for expats, travel insurance for expats explained, and single trip insurance for expats for detailed expatriate coverage information.

Claim processes and documentation essentials

Successful claim filing requires proof of delay or cancellation, medical records, and meeting submission deadlines. Understanding the claims process before you need it streamlines reimbursement and prevents common mistakes that lead to denials.

Required documentation varies by claim type but typically includes:

-

Flight disruption claims: Original boarding passes, airline delay or cancellation notifications, receipts for expenses incurred during delays, and written explanation of circumstances from the carrier.

-

Medical emergency claims: Complete medical records, itemised bills, prescription receipts, doctor’s notes explaining treatment necessity, and proof of payment.

-

Baggage claims: Property irregularity reports from airlines, receipts for delayed baggage purchases, proof of ownership for lost items, and photographs documenting damage.

-

Cancellation claims: Booking confirmations, cancellation notices, documentation proving the covered reason such as death certificates or medical certificates, and receipts showing non-refundable expenses.

Submission deadlines typically range from 30 to 60 days after the incident. Missing deadlines almost guarantees claim denial regardless of validity. Submit claims promptly and keep copies of all documentation for your records. Most insurers now accept electronic submissions, speeding up processing times.

Expatriates face additional documentation challenges when claiming from abroad. Language barriers can complicate obtaining proper medical documentation. Time zone differences may delay communication with claims departments. Consider working with local insurance representatives or assistance services who can help navigate documentation requirements in foreign healthcare systems.

Pro tip: Photograph all receipts immediately and store digital copies in cloud storage to prevent loss if your devices are stolen or damaged.

Timing and purchase considerations

Many policies require purchase within days of booking for cancellation coverage to be valid, making timing crucial for maximising protection. When you buy insurance affects not just coverage availability but also benefits you can access and conditions you must meet.

Optimal purchase windows open immediately after making your initial trip deposit. Most insurers require insurance purchase within 7 to 21 days of your first trip payment to qualify for full trip cancellation coverage and pre-existing condition waivers. This narrow window exists because insurers want to prevent people from purchasing coverage only after learning about potential disruptions.

Risks of delayed purchase include:

- Complete exclusion from trip cancellation and interruption benefits

- Inability to obtain pre-existing condition waivers regardless of health status

- Reduced coverage for known events that emerge between booking and insurance purchase

- Higher premiums if purchasing closer to departure dates

Continuous coverage importance for expatriates cannot be overstated. Gaps between policies leave you vulnerable during transitions. When one policy expires, ensure the next begins immediately without interruption. Some insurers offer automatic renewal to prevent accidental coverage lapses.

Synchronising insurance timing with itinerary changes requires proactive communication with your insurer. If you modify travel dates, destinations, or trip costs after purchasing insurance, notify your insurer immediately. Most policies allow adjustments with corresponding premium changes. Failing to update your policy can result in coverage gaps or claim denials.

For guidance on extending coverage during travel, review extend travel insurance options to understand modification procedures and requirements.

Find the right flight insurance for your needs

Protecting your international travel investment starts with selecting coverage tailored to your specific journey and circumstances. Whether you’re planning a brief holiday or relocating abroad for work, the right insurance prevents financial catastrophe when disruptions occur.

Our platform specialises in customised flight insurance solutions for international travellers and expatriates facing unique protection challenges. Compare policies designed for different travel profiles, from single trips to multi-year expatriate assignments. Integration with broader international health insurance creates comprehensive protection addressing both travel and health needs simultaneously.

Expatriates benefit from specialised insurance for working abroad that coordinates flight coverage with long-term health plans and liability protection. Don’t wait until after booking to explore options. Reviewing top flight insurance providers before purchasing flights ensures you understand coverage options and can time your insurance purchase optimally for maximum benefit eligibility.

Frequently asked questions

What does flight insurance typically cover?

Coverage includes trip cancellation reimbursement for non-refundable expenses, compensation for flight delays exceeding policy thresholds, medical emergency treatment and evacuation, and baggage loss or delay protection. Limits and conditions vary widely between basic and comprehensive policies. Most policies require specific covered reasons for cancellation such as illness, injury, or mandatory work obligations.

Are medical emergencies always covered by flight insurance?

Not necessarily, as many flight insurance policies provide only limited emergency medical coverage capped at £10,000 to £25,000. Some policies cover medical evacuation but exclude routine treatment costs. Comprehensive travel health insurance is recommended for full medical protection abroad, particularly for expatriates requiring extended coverage and higher limits.

How soon should I buy flight insurance after booking my flight?

Purchase within 7 to 21 days of making your initial trip deposit to ensure eligibility for trip cancellation coverage and pre-existing condition waivers. Delays beyond this window often exclude cancellation benefits entirely. Early purchase protects against unforeseen events that might necessitate cancelling your journey.

What unique flight insurance needs do expatriates have?

Expatriates require extended policy periods covering months or years rather than standard 30-day limits. Repatriation benefits become essential for returning home when local medical facilities cannot provide adequate care. Policies must integrate seamlessly with international health insurance to prevent coverage gaps whilst avoiding duplicate protection.