Securing the right health insurance is a crucial step for any international traveller planning a temporary stay in the United States. Without proper visit visa insurance, visitors risk both their finances and visa approval, as many countries now demand proof of adequate medical coverage before granting entry. Understanding what sets specialised health coverage policies apart will help you meet official requirements and protect yourself from costly medical emergencies while exploring or residing in the USA.

Table of Contents

- Visit Visa Insurance Defined and Explained

- Major Types and Essential Coverage Options

- Legal Requirements for Visa Applicants

- Common Pitfalls and Mistakes to Avoid

- Cost Factors and How to Choose Wisely

Key Takeaways

| Point | Details |

|---|---|

| Visit Visa Insurance is Essential | It is often a mandatory requirement for visa approval, ensuring adequate health coverage during international travel. |

| Coverage Varieties | Policies range from basic plans meeting minimum requirements to comprehensive plans that offer additional protections. |

| Documentation is Crucial | Proper documentation confirming insurance compliance is essential to avoid visa application rejections. |

| Understanding Costs | Insurance premiums vary by age, trip duration, and destination, making it vital to compare policies effectively before selection. |

Visit Visa Insurance Defined and Explained

Visit visa insurance is a specialised health coverage policy designed for international travellers who need temporary medical protection whilst visiting another country. Unlike standard travel insurance, this type of coverage specifically addresses the requirements that many countries impose on visa applicants and visitors.

This insurance serves a dual purpose: it protects your health and finances whilst abroad, and it satisfies official visa requirements. Many countries require proof of adequate health coverage before issuing visit visas. Understanding what this insurance covers helps you make informed decisions about your travels.

What Sets Visit Visa Insurance Apart

Visit visa insurance differs from general travel insurance in several important ways:

- Visa compliance focused – Meets specific country requirements for visa approval

- Medical emergency coverage – Pays for hospitalisation, emergency treatment, and medical evacuation

- Duration flexibility – Covers short-term visits, typically from 7 days to 12 months

- Global or regional options – Available for specific countries or worldwide coverage

- Age inclusivity – Often covers travellers of all ages, including seniors

Visit visa insurance isn’t just about protection; it’s often a mandatory requirement to even receive your visa approval from immigration authorities.

Core Coverage Components

When you purchase visit visa insurance, you’re securing protection across several key areas. Emergency medical expenses form the foundation, covering hospitalisation costs, doctor visits, and prescribed medications. Most policies cover between £30,000 and £1,000,000 depending on your chosen plan.

Repatriation and medical evacuation ensures you can return home if your condition becomes serious. This proves invaluable if you’re visiting remote areas or countries with limited medical facilities.

Additional components typically include:

- Dental treatment for emergency pain relief

- Pharmacy costs for essential medications

- Hospital daily allowances for extended stays

- Emergency evacuation transport

- Pre-existing condition coverage (in some policies)

When you understand visa insurance requirements across different countries, you’ll see that coverage amounts and specific inclusions vary based on destination and visa type.

Why Visit Visa Insurance Matters

Medical emergencies abroad can devastate your finances. A single hospital stay in the United States, Canada, or Australia can cost thousands of pounds. Visit visa insurance protects you from these catastrophic costs whilst ensuring you meet immigration requirements.

Many visitors underestimate how expensive healthcare becomes without insurance. A broken bone requiring surgery might cost £15,000 to £50,000 in private hospitals. Insurance transforms this potential disaster into a manageable situation.

Beyond financial protection, this insurance gives you peace of mind. You can explore your destination knowing that if something goes wrong, you’re covered medically and financially.

Pro tip: Purchase visit visa insurance before your trip begins and verify it meets your destination country’s specific requirements, as immigration standards vary significantly by nation.

Major Types and Essential Coverage Options

Visit visa insurance comes in several distinct types, each designed to meet different travel needs and destination requirements. Understanding these options helps you select the right coverage before you apply for your visa or begin your journey.

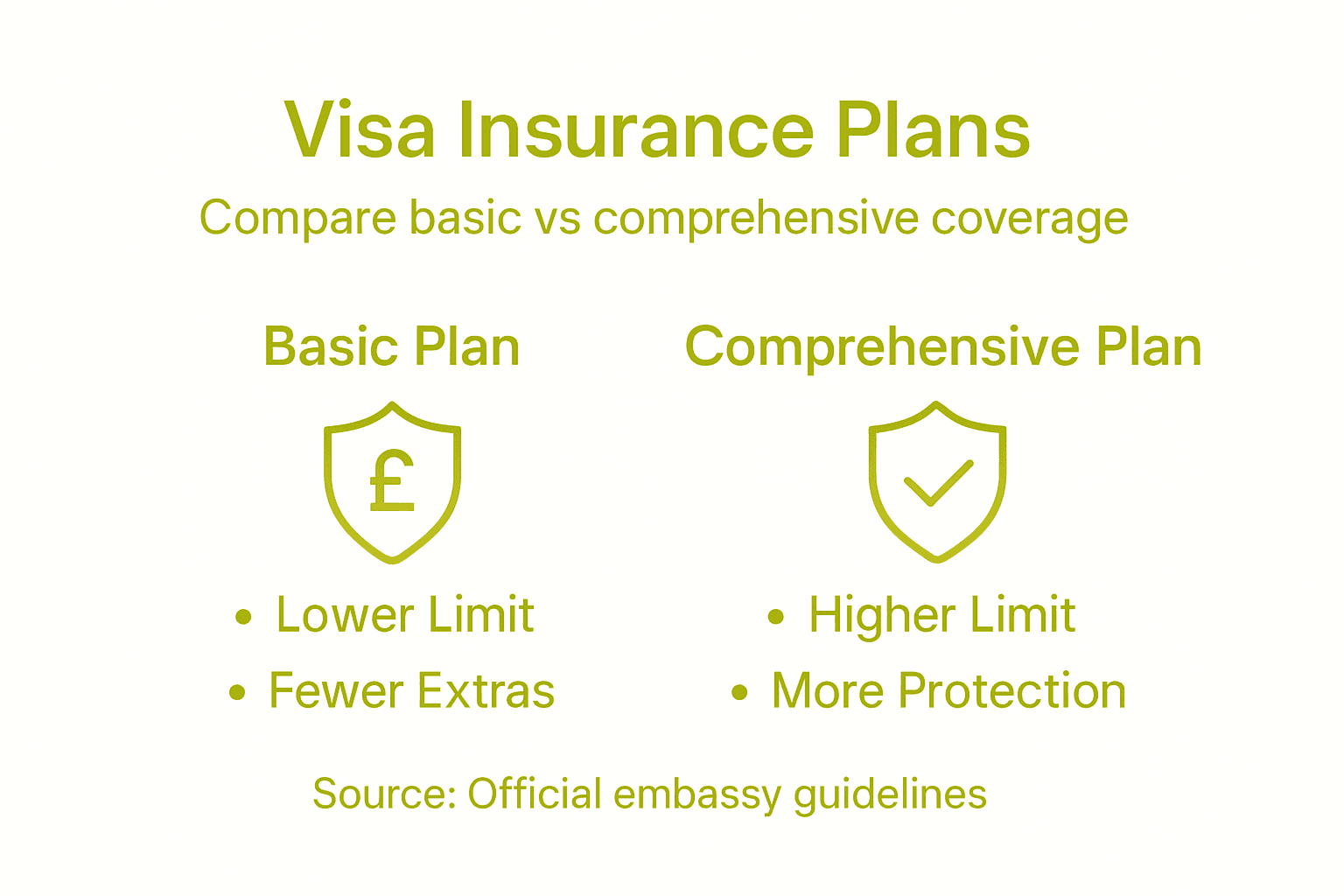

The primary distinction lies between basic plans and comprehensive plans. Basic plans cover the essentials required by immigration authorities, whilst comprehensive plans add optional protections like trip cancellation and baggage cover.

The table below compares basic and comprehensive visit visa insurance plans to help you choose the most suitable option for your needs:

| Feature | Basic Plan | Comprehensive Plan |

|---|---|---|

| Coverage Limit | Meets minimum visa requirement | Often exceeds minimum, higher cover |

| Included Benefits | Essential medical only | Medical plus extras (cancellation, baggage) |

| Cost | Lower, budget-friendly | Higher, offers broader protection |

| Suitable For | Those seeking visa approval only | Travellers wanting added peace of mind |

Core Insurance Types

Most visit visa insurance falls into one of these categories:

- Schengen visa insurance – Required for travel to European Schengen countries with minimum €30,000 coverage

- Single-country visa insurance – Tailored for specific nations like Canada, Australia, or the United States

- Multi-country coverage – Protects you across several countries during a single trip

- Long-term visitor insurance – Designed for extended stays lasting months or over a year

- Senior traveller insurance – Specialised plans covering older visitors up to 100 years old

Essential Coverage Components

Emergency medical treatment and hospitalisation form the foundation of every legitimate visit visa insurance policy. This covers doctor visits, prescribed medications, and overnight hospital stays when you become ill or injured abroad.

Medical evacuation and repatriation ensures you can return home for treatment if your condition becomes severe. These services prove invaluable in remote locations or countries with limited healthcare infrastructure.

Additional essential components include:

- Emergency dental treatment for pain relief

- Prescribed pharmacy costs for essential medications

- Hospital daily allowances during extended treatment

- Medical repatriation of remains if the worst occurs

- 24-hour medical assistance and helpline support

Your coverage must remain valid throughout your entire visa duration and across all countries within your travel zone, or immigration authorities may reject your application.

Optional Add-On Coverage

Beyond the essentials, you can enhance your protection with optional extras. Trip cancellation insurance reimburses prepaid costs if you must cancel before departure due to illness or family emergencies.

Baggage and personal belongings cover protects you if luggage gets lost or delayed during travel. This prevents the stress of replacing essential items during your trip.

Other useful add-ons include:

- Lost passport replacement assistance

- Travel delay compensation

- Personal liability cover for accidental damage

- Sports and hazardous activity coverage (if you disclose participation)

When comparing different travel insurance cover options, check whether your destination country accepts optional add-ons or requires basic-only coverage for visa approval.

Coverage Limits and Compliance

Coverage amounts vary significantly by destination. Schengen countries typically require minimum €30,000 coverage, whilst other nations demand higher amounts. Always verify your destination country’s specific requirements before purchasing.

Your policy must be valid for the entire duration of your stay and cover all countries you’ll visit. Partial coverage or gaps in protection can result in visa rejection or leave you exposed financially during your travels.

Pro tip: Obtain a cover letter or certificate from your insurer confirming your policy meets your destination country’s visa requirements, as immigration authorities often request this documentation with your application.

Legal Requirements for Visa Applicants

Visa insurance isn’t optional for most international travellers. Immigration authorities in dozens of countries legally require proof of adequate health coverage before they’ll issue your visa. Understanding these legal requirements prevents costly application rejections and delays.

Each destination country sets its own standards. Some require minimum coverage amounts, whilst others specify which types of treatment must be included. Submitting inadequate insurance documentation is one of the most common reasons visa applications get rejected.

Schengen Countries’ Strict Standards

If you’re travelling to Europe, you’ll encounter some of the world’s strictest insurance requirements. Since 2004, Schengen visa applicants must present travel medical insurance covering at least €30,000 of medical expenses and repatriation costs.

This isn’t a guideline—it’s a legal requirement. Your policy must cover the entire duration of your stay across all Schengen countries. Immigration officials will reject your application if your insurance expires before your visa does.

The €30,000 minimum covers:

- Emergency medical treatment and hospitalisation

- Doctor visits and prescribed medications

- Medical evacuation and repatriation home

- Hospital stays and surgical procedures

- Emergency dental treatment for pain relief

Gaps in coverage or policies that don’t span your entire visit can result in automatic visa rejection, regardless of your other qualifications.

Non-Schengen Country Requirements

Countries outside Europe often demand different coverage amounts. Canada, Australia, and the United States typically require between £1 million and £2 million in medical coverage. Some Asian countries accept lower minimums around £50,000 to £100,000.

Your insurance must be valid throughout your entire stay. Short-term policies that expire mid-trip won’t satisfy immigration requirements. Check your destination country’s official immigration website for current requirements before purchasing.

Common legal requirements include:

- Minimum coverage amounts specified in local currency

- Coverage valid across all regions you’ll visit

- Protection for all visa duration dates

- Medical evacuation and repatriation cover included

- Policy issued by approved insurance providers

Documentation and Proof Requirements

Immigration authorities need official documentation confirming your coverage meets their standards. Simply owning a policy isn’t enough—you must provide proof during your visa application.

Require from your insurer:

- Cover letter confirming minimum coverage amounts

- Policy summary with effective dates

- Details of covered territories and regions

- Certificate of insurance on official letterhead

- 24-hour emergency contact information

Keep digital and printed copies of all documentation. Submit them with your visa application to prevent processing delays or rejection.

Pro tip: Contact your destination country’s visa office before purchasing insurance to confirm current legal requirements, as minimums and coverage types change periodically and vary significantly between nations.

Common Pitfalls and Mistakes to Avoid

Many visa applicants rush through insurance selection and make costly mistakes. These errors delay your application, drain your finances, or result in outright rejection. Knowing what to avoid saves time, money, and stress.

The most common pitfalls stem from poor timing, insufficient coverage, and inadequate documentation. Understanding these mistakes helps you navigate the process smoothly.

Timing and Purchasing Errors

Purchasing insurance too late creates unnecessary pressure and missed opportunities. Ideally, you should buy coverage at least two weeks before submitting your visa application. This allows time to gather documentation and address any issues your embassy raises.

Don’t wait until the last minute. Delayed applications mean delayed visa processing, and some countries reject applications with incomplete insurance documentation regardless of other qualifications.

Timing mistakes include:

- Buying insurance after submitting your visa application

- Selecting policies with expiry dates before your visa ends

- Purchasing short-term coverage that gaps mid-travel

- Forgetting that processing takes time before your trip begins

Coverage Limit and Type Mistakes

Many travellers select policies with insufficient coverage limits or those excluding certain medical treatments required by visa authorities. Buying the cheapest policy available often leaves dangerous gaps in protection.

If your policy doesn’t meet your destination’s minimum coverage amount, immigration officials will reject your application outright. Choosing €20,000 coverage when Schengen countries require €30,000 guarantees rejection.

Common coverage mistakes include:

- Underestimating required minimum coverage amounts

- Excluding emergency evacuation protection

- Skipping repatriation cover for remains

- Omitting dental treatment for pain relief

- Selecting plans without 24-hour medical assistance

Inadequate coverage isn’t a minor issue—it’s grounds for automatic visa rejection, even if your application is otherwise perfect.

Documentation and Verification Failures

Failing to confirm your insurance is accepted by the embassy creates a critical problem. Not all policies meet every country’s requirements. Some insurers aren’t recognised by specific embassies, rendering your policy useless for visa purposes.

Contact your destination country’s visa office and verify your chosen policy meets their standards. Request written confirmation from your insurer that the policy complies with local requirements.

Documentation problems include:

- Missing cover letters from your insurer

- Policies without English translations

- Insufficient proof of coverage validity dates

- No confirmation that all destinations are covered

- Missing emergency contact information

Coverage Territory and Duration Problems

Neglecting to check that your policy covers all planned destination countries causes unexpected gaps. If you’re visiting multiple countries and your policy only covers some, you’re not properly protected.

Your coverage must extend for the entire duration of your visa. Calculate your exact travel dates, then verify your policy begins before arrival and ends after departure.

Pro tip: Request a detailed cover letter from your insurer listing all covered countries, minimum coverage amounts, and exact policy dates before submitting your visa application to prevent rejection delays.

Cost Factors and How to Choose Wisely

Visit visa insurance premiums vary considerably depending on your personal circumstances and travel details. Understanding what drives costs helps you find affordable coverage that meets your visa requirements without overpaying.

Price isn’t everything. The cheapest policy might leave dangerous gaps in coverage, whilst a well-chosen plan protects you financially and satisfies immigration authorities. Smart selection balances cost with genuine protection.

Key Cost Drivers

The cost of visit visa insurance depends on factors such as age, duration of the trip, coverage limits, and the destination region. Older travellers typically pay significantly higher premiums than younger visitors.

A 65-year-old might pay three times more than a 30-year-old for identical coverage. Duration matters enormously too—a three-month policy costs far less than a year-long plan, but the daily rate actually increases for longer trips.

Factors affecting your premium include:

To aid your decision, here is an overview of key factors that influence visit visa insurance costs:

| Cost Factor | Impact on Premium | Explanation |

|---|---|---|

| Age of Traveller | Significant increase after 55 years | Older applicants represent higher risk |

| Trip Duration | Longer stays cost more overall | Daily rates decrease with length |

| Destination Region | Higher for USA, Canada, Australia | Medical costs vary by country |

| Coverage Amount | Higher limits raise price | More expensive policies offer more cover |

| Pre-existing Conditions | May incur surcharges | Additional risk assessment required |

- Age – Rates increase substantially after age 55 and again after 70

- Trip duration – Longer stays mean higher total costs but better daily rates

- Coverage limits – Higher minimums (£1 million versus £100,000) increase premiums

- Destination region – Schengen countries cost less than North America or Australia

- Pre-existing conditions – Declaring medical history may increase costs or require exclusions

Comparing Policies Effectively

Comparing quotes requires more than looking at prices. Two policies at different price points might offer vastly different protection. You need a systematic approach to evaluate what you’re actually getting.

Create a comparison table listing coverage amounts, exclusions, excess amounts, and emergency contact details. Many travellers skip this step and regret it when claims get denied due to exclusions they didn’t notice.

Key comparison points:

- Minimum coverage amounts meet visa requirements

- Medical evacuation included and adequately covered

- Pre-existing condition coverage or exclusions

- Excess amounts and deductible costs

- Policy exclusions and what’s NOT covered

Selecting based solely on price often results in inadequate coverage that leaves you vulnerable financially or causes visa rejection.

Making Your Final Selection

Once you’ve narrowed down options, verify each policy meets your destination’s specific visa requirements. Contact the embassy to confirm the insurer is recognised and that coverage amounts are acceptable.

Request written confirmation from your chosen insurer that their policy complies with visa requirements. This document becomes part of your application and prevents rejection delays.

Your selection should include:

- Proof that coverage meets destination requirements

- Clear documentation of all covered treatments

- Emergency contact numbers for 24-hour assistance

- Confirmation of policy validity dates

- Details of what happens if you need to extend coverage

Age-Specific Considerations

Seniors face higher premiums but shouldn’t compromise on coverage. Many standard policies exclude older travellers entirely, making specialist senior plans essential. Fortunately, reputable insurers offer comprehensive coverage for visitors up to 100 years old.

Younger travellers can access more affordable premiums but shouldn’t automatically choose basic coverage. A slightly higher premium for comprehensive protection provides peace of mind during your travels.

Pro tip: Get quotes from multiple insurers and request detailed comparisons showing exactly what each policy covers, then select the option offering best value for your specific visa requirements rather than simply choosing the lowest price.

Secure Your Visit Visa with Confident Insurance Solutions

Navigating the complex requirements of visit visa insurance can be daunting. The article highlights critical challenges such as meeting minimum coverage amounts, ensuring coverage validity throughout your travel, and avoiding costly mistakes like insufficient documentation or policy exclusions. These pain points often cause frustrating visa rejections or expose travellers to unexpected medical expenses abroad. Whether you need Schengen visa insurance, coverage for North America, or long-term visitor plans, it is essential to find tailored policies that satisfy immigration standards while offering comprehensive medical protection.

Take control of your journey today by exploring personalised visit visa insurance plans at Unparalleled Global Benefits. Benefit from detailed guidance, verified coverage options, and documents designed to meet embassy requirements. Don’t wait until the last moment with your visa application. Act now to secure peace of mind and financial safety with trusted international insurance solutions specifically crafted for travellers like you. Visit our top insurers page to compare plans and request your quote with confidence.

Frequently Asked Questions

What is visit visa insurance?

Visit visa insurance is a specialised health coverage policy for international travellers that provides temporary medical protection and meets visa requirements.

How does visit visa insurance differ from standard travel insurance?

Visit visa insurance is specifically designed to comply with visa application requirements and generally focuses on emergency medical coverage, while standard travel insurance may include broader protections for cancellations and lost baggage.

What are the core components covered by visit visa insurance?

Core components typically include emergency medical expenses, repatriation and medical evacuation, dental treatment for emergency relief, pharmacy costs, and hospital daily allowances.

Why is visit visa insurance mandatory for visa applications?

Many countries require proof of adequate health coverage as a legal requirement for visa approval to protect travellers from high medical costs and ensure they can receive appropriate care while abroad.

Recommended

- Visa Card Travel Insurance – Essential Facts for Expats – Unparalleled Global Benefits

- Visa Travel Insurance: Why It Matters For Visa Holders – Unparalleled Global Benefits

- Travel Insurance for Visa: Complete Expert Guide – Unparalleled Global Benefits

- Visa Insurance Explained: Meeting Global Travel Rules – Unparalleled Global Benefits