Travel medical insurance can make or break your safety net abroad. Think you can save the most by simply picking the cheapest policy? Wait until you see the real impact of your deductible choice. Choosing a higher deductible can slash your premiums by up to 45 percent but that strategy holds risks many travellers never see coming.

Table of Contents

- What Is A Travel Medical Insurance Deductible

- How Deductibles Affect Different Travellers

- Choosing The Right Deductible For Your Needs

- Smart Tips For Saving On Medical Deductibles

Quick Summary

| Takeaway | Explanation |

| Understand your deductible options | The deductible affects your financial responsibility before insurance covers costs. Assess what works for your travel profile. |

| Higher deductibles reduce premiums | Selecting a higher deductible can save you on monthly insurance costs, but ensure you can cover potential out-of-pocket expenses. |

| Tailor deductible choice to travel type | Different traveller categories, such as digital nomads or adventure seekers, require unique deductible strategies based on risk and duration. |

| Maintain an emergency fund | Having accessible savings to cover the deductible is crucial for unexpected medical expenses while travelling. |

| Regularly review your insurance needs | Situations change; periodic assessment of your insurance and deductible ensures your coverage remains aligned with your current travel plans. |

What Is a Travel Medical Insurance Deductible

Understanding the travel medical insurance deductible is crucial for anyone planning international travel or working abroad. A deductible represents the initial out of pocket expense you must pay before your insurance coverage activates.

The Basic Mechanics of Deductibles

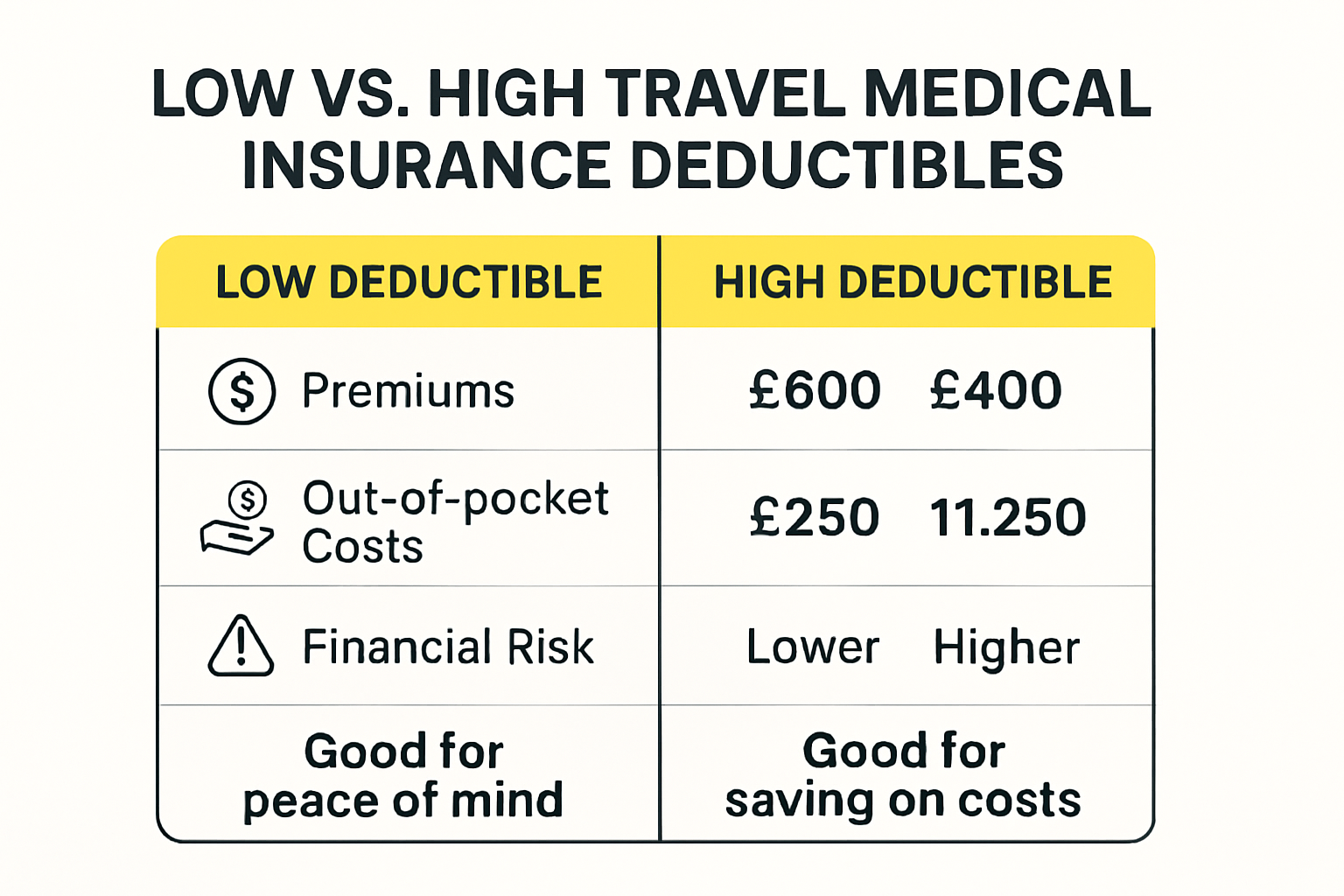

When you purchase a travel medical insurance policy, the deductible acts as a financial threshold determining how much you are responsible for paying before your insurance provider begins covering medical expenses. According to the International Association for Medical Assistance to Travellers, this means if you have a $500 deductible and incur an $8,000 medical bill, you would pay the first $500, with the insurance company covering the remaining $7,500.

The relationship between deductibles and premiums is critically important. Generally, policies with lower deductibles result in higher monthly or annual premium costs, while higher deductibles translate to lower premium expenses. This trade off allows travellers to customize their insurance based on their personal risk tolerance and financial situation.

Choosing the Right Deductible Strategy

Selecting an appropriate deductible requires careful consideration of multiple factors. As the Agency for Healthcare Research and Quality explains, the deductible represents a fixed dollar amount during your benefit period that you are personally responsible for before insurance payments commence.

When evaluating deductible options, consider these key strategic elements:

- Risk Assessment: Evaluate your personal health history and potential medical needs during travel

- Financial Flexibility: Determine how much you can comfortably pay out of pocket in an emergency

- Trip Duration: Longer trips might warrant different deductible strategies compared to shorter journeys

From a broader insurance perspective, Wikipedia notes that deductibles are strategically designed to discourage numerous small claims while focusing coverage on significant medical events. Insurance providers use this mechanism to manage risk and maintain more predictable financial outcomes.

Travellers should view their deductible not as an obstacle but as a strategic financial tool that allows for personalized medical protection. By understanding how deductibles function, you can make informed decisions that balance comprehensive coverage with financial practicality.

Remember that the right travel medical insurance deductible is not a one size fits all solution. It requires thoughtful analysis of your individual travel plans, health considerations, and financial capabilities.

How Deductibles Affect Different Travellers

Travel medical insurance deductibles impact various traveller groups differently, requiring nuanced understanding and strategic planning. Each traveller type encounters unique challenges when selecting appropriate insurance coverage.

To help you understand how deductible choices impact different types of travellers, here’s a comparison of deductible strategies and considerations for each traveller profile discussed:

| Traveller Type | Deductible Strategy | Key Considerations |

| Digital Nomads / Long Term Travellers | Higher deductible for lower premiums | Need strong emergency fund; manage variable income |

| Healthcare Professionals / High Risk | Lower deductible for more comprehensive cover | Lower out-of-pocket costs; broad coverage; rapid claims |

| Adventure Travellers / Short Term | Varies – often lower deductible recommended | Assess personal risk; higher risk = lower deductible advised |

| Budget Explorers | Higher deductible to minimise premium | Weigh risk tolerance; maintain accessible savings |

Digital Nomads and Long Term Travellers

Digital nomads and professionals working internationally face distinctive insurance considerations. The Centers for Disease Control and Prevention recommends that travelers carefully evaluate supplemental medical insurance, particularly when working in remote destinations with limited medical infrastructure.

For these mobile professionals, selecting a deductible involves balancing monthly budget constraints with potential medical risks. Higher deductibles can significantly reduce monthly premium expenses, which is attractive for individuals managing variable income streams. However, this approach requires maintaining robust emergency savings to cover potential out of pocket medical expenses.

Healthcare Professionals and High Risk Travelers

Healthcare workers, researchers, and travelers visiting regions with elevated health risks require more comprehensive insurance strategies. Research published in the National Center for Biotechnology Information reveals that individuals perceiving higher health risks are more inclined to select insurance plans with lower deductibles.

Specifically, professionals working in challenging environments such as humanitarian zones, conflict regions, or areas with significant infectious disease prevalence might prioritize plans offering:

- Lower Initial Expenses: Reduced out of pocket costs during medical emergencies

- Broader Coverage: Comprehensive protection across multiple potential scenarios

- Rapid Claim Processing: Faster reimbursement and medical support

Adventure Travelers and Short Term Explorers

Adventure travelers and short term international visitors face different deductible considerations. While budget conscious travelers might gravitate towards higher deductible plans to minimize monthly expenses, they must carefully assess potential risks associated with their specific travel activities.

According to the International Association for Medical Assistance to Travellers, selecting an appropriate deductible involves understanding personal risk tolerance. Adventure travelers engaging in high risk activities like mountain climbing, extreme sports, or wilderness expeditions should consider lower deductible options to mitigate potential financial strain during unexpected medical incidents.

Ultimately, choosing the right travel medical insurance deductible requires thorough personal assessment. Travelers must evaluate their individual health profile, financial resources, destination characteristics, and potential risk exposure. A strategic approach involves not just comparing premium costs but understanding comprehensive protection mechanisms that align with unique travel circumstances.

Choosing the Right Deductible for Your Needs

Selecting the appropriate travel medical insurance deductible requires strategic financial planning and a comprehensive understanding of your personal circumstances. The right choice balances potential risk, financial capability, and long term protection.

Assessing Personal Financial Readiness

Financial preparedness is the cornerstone of selecting an appropriate deductible. The Alberta Motor Association indicates that adding a deductible can reduce insurance premiums by up to 45%. However, this potential savings comes with a critical caveat: you must have immediate access to funds covering your chosen deductible amount.

Key financial considerations include:

- Emergency Savings: Ensure you have sufficient liquid funds to cover the entire deductible

- Income Stability: Evaluate your ability to absorb unexpected medical expenses

- Risk Tolerance: Understand your comfort level with potential out of pocket costs

Strategizing Coverage Based on Travel Profile

Your travel characteristics significantly influence deductible selection. The Associated Press emphasizes the importance of understanding not just the deductible, but additional potential costs like coinsurance.

Consider these strategic approaches based on travel type:

- Frequent International Travelers: Lower deductibles might provide more predictable cost structures

- Budget Conscious Explorers: Higher deductibles can significantly reduce monthly premium expenses

- High Risk Destination Travelers: Comprehensive coverage with manageable out of pocket expenses becomes paramount

Practical Deductible Selection Techniques

According to the International Association for Medical Assistance to Travellers, selecting a deductible involves more than simply choosing the lowest premium. Travelers must conduct a holistic assessment of their medical insurance needs.

Recommended selection techniques include:

- Calculating potential annual savings from different deductible levels

- Comparing total potential expenses (premiums plus potential out of pocket costs)

- Reviewing personal health history and anticipated medical requirements

- Considering destination specific healthcare challenges

The optimal deductible represents a nuanced balance between financial protection and affordable coverage. Travelers should view their insurance not as an expense, but as a strategic investment in personal safety and financial security.

Selecting a travel medical insurance deductible involves several practical steps. The following table outlines a simple checklist of what to assess for making an informed choice:

| Selection Step | Description | Ready? |

| Evaluate Emergency Savings | Confirm access to funds for deductible | |

| Review Health & Risk Profile | Assess personal and destination risk factors | |

| Compare Premium and Deductible | Check premium savings vs. potential out-of-pocket | |

| Assess Income Stability | Ensure regular income or backup funds | |

| Research Coverage Limitations | Identify coverage gaps and policy restrictions | |

| Plan Periodic Policy Reviews | Set reminders to re-evaluate insurance needs |

Remember that no universal deductible solution exists. Your ideal approach depends on individual circumstances, travel patterns, health considerations, and personal risk management strategies. Periodic review and adjustment of your travel medical insurance deductible ensures continued alignment with your evolving lifestyle and protection needs.

Smart Tips for Saving on Medical Deductibles

Reducing medical deductible expenses requires strategic planning and proactive financial management. Travelers can implement multiple approaches to minimise their out of pocket healthcare costs while maintaining comprehensive medical coverage.

Understanding Insurance Claim Dynamics

Research from the National Center for Biotechnology Information reveals fascinating insights into insurance claim mechanisms. The study demonstrates that higher deductibles correlate with decreased insurance claims, suggesting travelers can leverage strategic deductible selection to manage overall healthcare expenses.

Key strategies for optimising insurance claims include:

- Preventive Care: Prioritise routine health screenings

- Documentation: Maintain comprehensive medical records

- Claims Awareness: Understand precise claim submission processes

Comprehensive Coverage Planning

The Centers for Disease Control and Prevention emphasises the critical importance of understanding insurance coverage gaps. Travelers must carefully review their existing health insurance policies to identify potential international medical coverage limitations.

Recommended planning approaches:

- Policy Comparison: Evaluate multiple insurance options

- Supplemental Coverage: Consider additional travel health insurance

- Emergency Fund: Maintain liquid savings for unexpected medical expenses

Proactive Financial Management

The International Association for Medical Assistance to Travellers highlights the significance of immediate financial preparedness. While higher deductibles can reduce premium costs, travelers must ensure they can access funds quickly during medical emergencies.

Practical financial strategies include:

- Creating dedicated emergency medical savings accounts

- Exploring flexible payment options with healthcare providers

- Investigating medical cost negotiation techniques

- Understanding international medical billing processes

Successful medical deductible management transcends simple cost reduction. It represents a holistic approach to personal health risk management, combining financial planning, comprehensive insurance understanding, and proactive healthcare decision making.

Travelers should view their medical insurance deductible not as a financial burden, but as a strategic tool for managing potential healthcare risks. Regular policy review, continuous financial preparation, and a thorough understanding of coverage details can transform the deductible from a potential financial challenge into an effective risk mitigation strategy.

Frequently Asked Questions

What is a travel medical insurance deductible?

A travel medical insurance deductible is the amount you must pay out of pocket for medical expenses before your insurance coverage kicks in.

How does the deductible affect my travel insurance premiums?

Generally, selecting a higher deductible can significantly reduce your insurance premiums, possibly by up to 45%. However, it’s crucial to ensure you can afford the deductible amount in case of an emergency.

How do I choose the right deductible for my travel profile?

Choosing the right deductible involves assessing your personal financial readiness, understanding your travel type, and evaluating health risks. Long-term travellers might prefer higher deductibles to save on premiums, while those in high-risk categories may benefit from lower deductibles.

What should I consider regarding my emergency savings and deductible?

It’s essential to maintain an emergency fund that can cover your deductible amount, ensuring you can handle unexpected medical expenses while travelling without financial strain.

Get Travel Medical Insurance That Truly Matches Your Needs

You have just learned how selecting the right travel medical insurance deductible is more than a number. Coping with unpredictable healthcare costs abroad demands more than guesswork. Many travellers worry about their financial readiness for medical emergencies, especially when higher deductibles seem tempting for saving on premiums. At Unparalleled Global Benefits, we know how vital it is to secure the right protection while keeping your finances stable. Our bespoke expat medical and travel insurance solutions help you balance risk, destination requirements and personal safety so you are never caught off guard.

Tailor your coverage to suit your travel plans and build confidence before your next journey. Explore our expert travel and expat medical insurance options and see how our experience can guide you through every deductible decision. If you want support choosing between premium costs, practical coverage and out-of-pocket limits, visit our website now and take the first step towards greater peace of mind.