TL;DR:

- A reliable travel insurance company possesses strong financial ratings, positive customer reviews, and transparent claims processes. It offers core coverage such as medical expenses, trip cancellation, baggage loss, and personal liability to ensure comprehensive protection. Travelers with pre-existing conditions should disclose all health details accurately and consider specialist policies for better coverage.

A good travel insurance company is defined by its financial reliability, the breadth of its coverage, the quality of its customer support, and the flexibility of its policies. These four qualities separate a provider you can genuinely depend on from one that looks attractive on paper but fails when you need it most. Ratings bodies such as AM Best and Moody’s assess insurer financial strength, while platforms like Trustpilot and NerdWallet aggregate real customer experiences. Whether you are buying single trip travel insurance for a fortnight in Europe or seeking affordable travel insurance options for a longer international stay, knowing what to look for in travel insurance protects both your health and your finances.

What core coverage should a good travel insurance policy offer?

Core travel insurance coverage includes trip cancellation, trip interruption, emergency medical expenses, baggage loss, travel delays, and personal liability. Each of these serves a distinct purpose, and a policy missing any one of them leaves a meaningful gap in your protection.

Here is what each element covers in practice:

- Emergency medical expenses and repatriation. This pays for hospital treatment abroad and, if necessary, the cost of flying you home under medical supervision. Without it, a single hospitalisation in the United States can cost tens of thousands of pounds.

- Trip cancellation and interruption. This reimburses pre-paid, non-refundable costs if you must cancel before departure or cut a trip short due to illness, bereavement, or other covered reasons.

- Baggage loss and travel delay. Compensation for lost, stolen, or damaged luggage, plus daily allowances when flights are significantly delayed.

- Personal liability. Covers legal costs and compensation if you accidentally injure someone or damage their property while travelling.

- Optional add-ons. These include pre-existing medical condition waivers, adventure sports cover, and COVID-19 related benefits. Not every traveller needs every add-on, but their availability signals a provider’s willingness to accommodate diverse needs.

Coverage limits and exclusions matter as much as the headline benefits. A policy with a £5,000,000 medical limit and a £500 baggage limit is not balanced. Read both figures before you buy.

Pro Tip: Always check the excess on each benefit separately. Some policies carry a £100 excess on medical claims and a separate £75 excess on baggage. These add up quickly during a complex claim.

You can learn more about what basic policies include in Unparalleledglobalbenefits’ guide on what basic travel insurance covers.

How do financial strength and reputation affect insurance quality?

A travel insurer’s financial strength rating is the single most objective measure of its ability to pay claims. AM Best and Moody’s both publish ratings that reflect an insurer’s capital reserves, claims history, and long-term stability. A company rated “A” or above by AM Best has demonstrated it holds sufficient reserves to honour large volumes of claims simultaneously, including during a crisis such as a pandemic or natural disaster.

Customer satisfaction scores add a second layer of evidence. NerdWallet’s 2026 criteria for ranking travel insurance companies include coverage depth, customisability, and customer satisfaction ratings drawn from platforms like Trustpilot. These scores reflect real claim experiences, not marketing promises.

A provider may advertise generous coverage limits, but if its claims payment record is poor or its customer service is difficult to reach during an emergency, those limits mean very little. The best measure of a travel insurer is how it behaves when something goes wrong, not how it presents itself when you are buying.

Regulatory compliance is equally telling. A provider licensed and regulated by a recognised financial authority, such as the Financial Conduct Authority in the United Kingdom, is subject to mandatory conduct standards and dispute resolution processes. This gives you legal recourse if a claim is unfairly denied.

Longevity also matters. An insurer that has operated for decades has weathered economic downturns, pandemics, and large-scale natural disasters. That track record is evidence of genuine financial resilience.

How do travellers with pre-existing conditions find the right cover?

Medical screening is critical for any traveller with a pre-existing condition. Insurers require accurate health information before issuing a policy, and failing to disclose a condition correctly can result in a claim being denied entirely, regardless of how reputable the provider is. This is the single most common reason legitimate claims are rejected.

Follow these steps to secure appropriate cover:

- Disclose every condition accurately. List all diagnosed conditions, current medications, and any treatment received in the past 12–24 months. Omitting a condition, even one you consider minor, creates grounds for denial.

- Complete a full medical screening. Most providers offering cover for pre-existing conditions require a telephone or online screening. Answer every question honestly.

- Compare specialist policies. Standard policies often exclude pre-existing conditions entirely. Specialist providers and brokers offer policies with waivers that include these conditions for an additional premium.

- Check the assessment criteria. Age, the nature of the condition, and how recently it was treated all affect eligibility. Some providers set upper age limits or restrict cover for conditions diagnosed within the past two years.

- Review the exclusion list. Even a specialist policy may exclude specific complications. Read the policy wording, not just the summary.

Age is a significant variable in both eligibility and trip duration limits. Older travellers frequently face mandatory medical screening and shorter maximum trip lengths. Some providers offer no upper age limit plans, but travellers over 70 may find their maximum covered trip length capped at 31 days.

Pro Tip: If you are travelling to Portugal or another EU destination with a complex medical history, check local healthcare access rules before you buy. Unparalleledglobalbenefits’ partner guide on travel insurance in Portugal explains what inbound visitors need to know.

Unparalleledglobalbenefits has a detailed resource on cover for medical conditions that explains the screening process and how to find policies that genuinely include your health history.

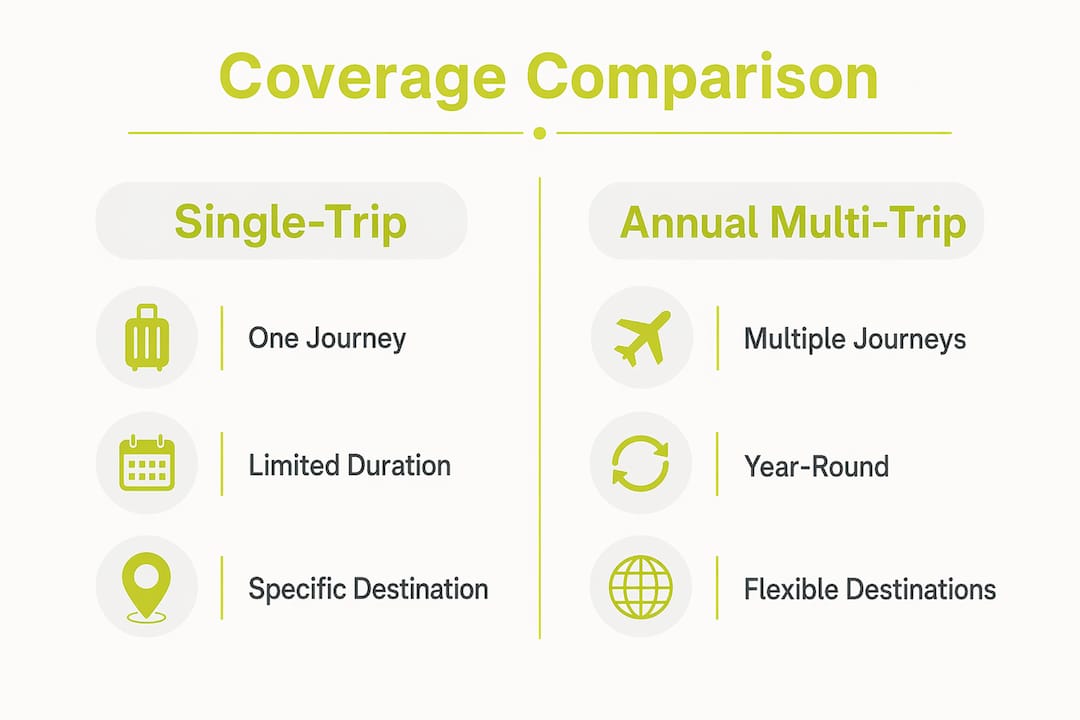

Single-trip vs annual multi-trip: which policy suits you?

The choice between single trip travel insurance and an annual multi-trip policy depends on how often you travel and for how long. Neither is universally better. The right answer depends on your specific plans.

Single-trip policies cover one continuous journey and can be purchased up to 18 months before departure, with coverage beginning from the purchase date. This means trip cancellation protection starts immediately, not just when you board a plane. Durations range from one night to 365 days, making one trip travel insurance suitable for everything from a weekend city break to a year-long sabbatical.

| Factor | Single-trip policy | Annual multi-trip policy |

|---|---|---|

| Number of trips covered | One continuous journey | Multiple trips within 12 months |

| Best suited to | Occasional travellers, long trips | Frequent travellers, short breaks |

| Cost efficiency | Lower upfront cost for one trip | More cost-effective for 3+ trips per year |

| Maximum trip duration | Up to 365 days per trip | Typically 31–90 days per individual trip |

| Flexibility | Tailored to one specific journey | Fixed annual renewal date |

Policies generally cannot be extended once a trip has started. If you plan to extend your stay, you must arrange this before your departure date. This is a common oversight that leaves travellers uninsured for the additional days.

The price of single trip travel insurance depends on your age, destination, trip length, and medical history. Policies are typically tiered, for example bronze, silver, and gold levels, with varying excesses and limits. Choosing a higher tier costs more upfront but reduces out-of-pocket costs during a claim.

For travellers who take three or more trips a year, an annual policy usually offers better value. For those taking one significant trip, the best single trip travel insurance gives targeted protection without paying for cover you will not use.

Key takeaways

A good travel insurance company combines strong financial ratings, transparent claims processes, and coverage that matches your specific travel needs, including any pre-existing medical conditions.

| Point | Details |

|---|---|

| Financial strength matters | Choose insurers rated by AM Best or Moody’s to confirm they can pay claims reliably. |

| Coverage must match your trip | Verify medical limits, baggage cover, and cancellation terms before purchasing any policy. |

| Disclose all medical conditions | Non-disclosure is the leading cause of claim denial, regardless of insurer quality. |

| Match policy type to travel frequency | Single-trip cover suits occasional travellers; annual policies suit those taking three or more trips per year. |

| Check age-related restrictions | Travellers over 70 may face shorter maximum trip durations and mandatory medical screening. |

What I have learned about trusting a travel insurer

Over the years, I have seen travellers make the same mistake repeatedly. They compare policies on price alone, pick the cheapest option, and assume the cover is broadly similar across providers. It rarely is.

The detail that catches people out most often is not the headline medical limit. It is the exclusions buried in the policy wording. A policy that excludes “any condition for which you have received treatment in the past 24 months” can effectively exclude a large portion of travellers over 50. That clause does not appear in the summary. You find it on page 14 of the full policy document.

My honest advice is to treat the claims process as the product. Before you buy, search the insurer’s name alongside the word “claim” on Trustpilot or a similar platform. Read the negative reviews specifically. Are the complaints about genuine coverage gaps, or are they about administration delays? The former is a red flag. The latter is manageable.

I also think travellers underestimate the value of a specialist broker for complicated medical histories. A broker who works with multiple underwriters can match your specific health profile to the right policy, rather than asking you to fit your health history into a standard online form. Unparalleledglobalbenefits takes exactly this approach, which is why I recommend starting there if your situation is anything other than straightforward.

For a broader look at how emergency medical evacuation cover works within a travel policy, that guide is worth reading before you finalise any purchase.

— Coert

Travel insurance arranged for your specific needs

Choosing the right policy is straightforward when you have the right guidance behind you. Unparalleledglobalbenefits specialises in arranging travel insurance for travellers with complex needs, including those with pre-existing medical conditions and seniors up to 100 years old.

Whether you need single trip insurance cover for one specific journey or want to understand your broader international health options, Unparalleledglobalbenefits can help you find a policy that fits your health profile, destination, and budget. Explore the travel insurance guide to understand exactly how your cover works before you travel.

Planning a trip for yourself, a resident, or visiting family? UGB + Ekta can arrange travel insurance for seniors up to 100 years old. Just click here: https://ektatraveling.com/?partner_uid=808 and add the promo code “UGB” to receive an additional 10% discount.

FAQ

What makes a travel insurance company reliable?

A reliable travel insurer holds strong financial strength ratings from bodies such as AM Best or Moody’s, maintains positive customer satisfaction scores on platforms like Trustpilot, and has a transparent claims payment record. Regulatory compliance with a recognised authority, such as the Financial Conduct Authority, provides an additional layer of accountability.

What does single trip travel insurance cover?

Single trip travel insurance covers one continuous journey and typically includes emergency medical expenses, trip cancellation, baggage loss, travel delays, and personal liability. Optional add-ons such as pre-existing condition waivers and adventure sports cover can be added for an additional premium.

Can I extend my travel insurance once my trip has started?

Travel insurance policies generally cannot be extended after a trip has begun. You must arrange any extension before your departure date to maintain continuous cover.

How does age affect travel insurance eligibility?

Age directly affects both eligibility and maximum trip duration. Some providers cap covered trip lengths at 31 days for travellers over 70, and mandatory medical screening becomes more common with age. Specialist providers, including those working with Unparalleledglobalbenefits, offer plans with no upper age limit for travellers who meet the screening criteria.

Is budget travel insurance for seniors worth considering?

Budget travel insurance for seniors can provide adequate cover for straightforward trips, but older travellers with pre-existing conditions should prioritise coverage quality over price. A low-cost policy that excludes your medical history offers no real protection when you need it most.