TL;DR:

- Airline insurance covers only flight-related risks such as cancellations, delays, and baggage issues, with limited medical coverage. It does not protect non-flight expenses or offer the higher medical limits provided by comprehensive travel insurance. Travelers should evaluate their trip’s complexity and costs to decide whether airline plans suffice or if broader coverage is necessary.

Airline insurance is a protection plan that covers specific risks tied to your flight, including trip cancellation, delays, baggage loss, and limited emergency medical expenses. The industry term for this product is an “airline protection plan,” and it differs meaningfully from comprehensive travel insurance, which covers your entire trip investment. Airline protection plans carry accident medical coverage between £10,000 and £50,000 and baggage loss limits between £500 and £1,000. Those figures matter because they reveal the core limitation of what does airline insurance cover: it protects your flight, not your whole trip.

What does airline insurance typically cover?

Airline insurance covers a defined set of flight-related risks. The coverage is narrow by design, underwritten by a third party, and sold at the point of ticket purchase for convenience. Understanding each element helps you judge whether the policy is adequate for your trip.

The main areas of cover are:

- Trip cancellation and interruption. You can claim a refund on your airfare if you cancel for a covered reason, such as illness, a death in the family, or severe weather. Cover applies to the flight cost only, not hotels or tours booked separately.

- Flight delay expenses. Travel delay cover activates after a waiting period of 3–12 hours, reimbursing hotel rooms, meals, and local transport during the delay.

- Baggage loss and delay. Baggage delay benefits generally trigger after 12–24 hours of missing luggage. Carriers declare baggage permanently lost only after 14–21 days, which is the point at which a permanent loss claim becomes valid.

- Emergency medical cover. Accident medical coverage sits between £10,000 and £50,000. That range sounds reassuring, but it is often insufficient for serious overseas hospitalisation.

- Accidental death and dismemberment. Most airline plans include a small lump-sum benefit for fatal accidents or serious injury during the flight.

Pro Tip: Read the policy certificate before you buy, not after. The waiting periods for delay cover and the exclusion list for cancellation are buried in the fine print and can significantly reduce what you can actually claim.

Waiting periods are a critical detail. A three-hour delay threshold sounds straightforward, but if your flight is delayed by two hours and fifty minutes, you receive nothing. Knowing these triggers in advance prevents unpleasant surprises at the airport.

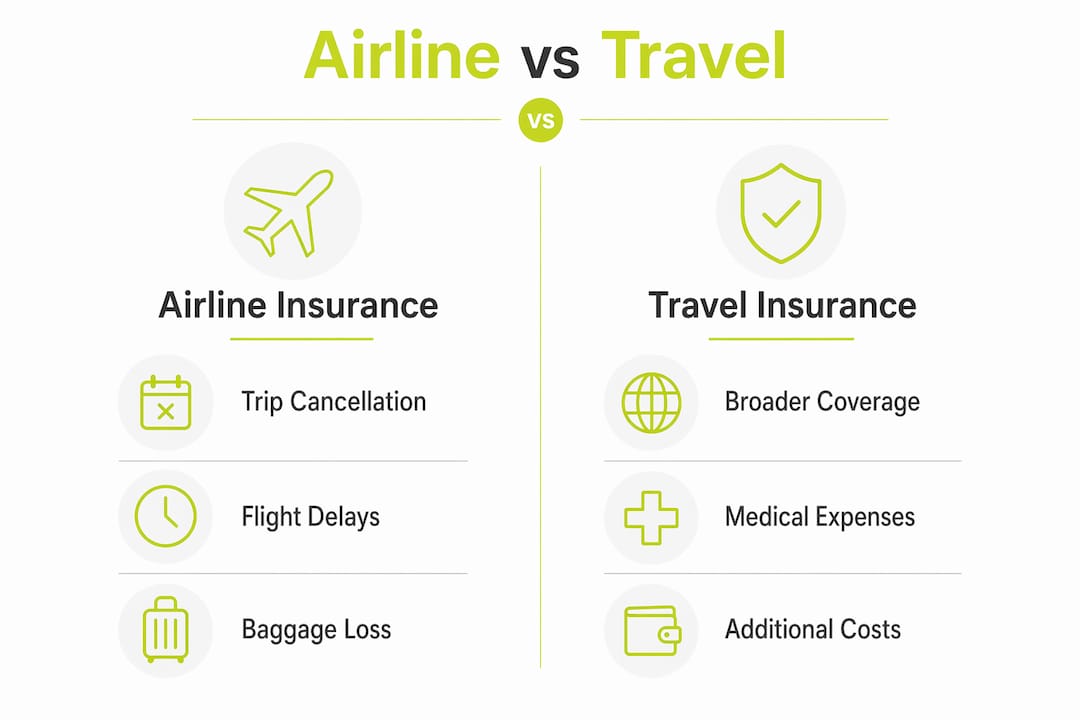

How does airline insurance differ from comprehensive travel insurance?

Most travellers confuse airline-offered insurance with comprehensive travel insurance. The distinction is not minor. Airline plans focus narrowly on the flight portion of your trip, while comprehensive policies cover the full trip cost, including non-refundable land arrangements.

The table below illustrates the key differences:

| Coverage category | Airline protection plan | Comprehensive travel insurance |

|---|---|---|

| Trip cancellation | Airfare only | Full trip cost including hotels and tours |

| Emergency medical | £10,000–£50,000 | Significantly higher limits, often £1,000,000+ |

| Medical evacuation | Rarely included | Typically included |

| Baggage loss limit | £500–£1,000 | Higher limits, often £2,500+ |

| Non-flight expenses | Not covered | Covered |

| Claim support | Limited | Dedicated claims teams |

The medical cover gap is the most consequential difference. Emergency medical coverage of £10,000–£50,000 is often insufficient for serious overseas hospitalisation, whereas retail plans offer higher limits and evacuation cover. A single night in a US hospital can exceed £10,000, which means an airline plan could leave you personally liable for the remainder.

Pro Tip: If your trip includes prepaid hotels, guided tours, or cruise add-ons, an airline plan will not protect those investments. Calculate the total non-refundable cost of your trip before deciding on cover.

For international or complex trips, the difference between cover types becomes financially significant. A comprehensive policy costs more upfront, but it protects a far larger portion of your total trip investment.

Common misconceptions about airline insurance coverage

The biggest misconception is that airline insurance covers your entire trip. It does not. Airline insurance often does not cover non-flight expenses such as hotels, cruise add-ons, or ski passes, leaving major parts of your trip investment uninsured.

Other frequent misunderstandings include:

- “My medical bills abroad will be covered.” The £10,000–£50,000 medical limit sounds adequate until you face a serious illness or accident overseas. Evacuation alone can cost tens of thousands of pounds and is rarely included in airline plans.

- “I can cancel for any reason.” Standard airline plans cover cancellation only for specific listed reasons. “Cancel for any reason” is a premium upgrade, not a default feature.

- “Baggage cover replaces everything I packed.” Baggage limits of £500–£1,000 rarely reflect the actual value of electronics, clothing, and personal items in a checked bag.

- “The airline will sort it out anyway.” Airlines have their own liability limits under international conventions, but those limits are low and the claims process is separate from your insurance policy.

- “I do not need to read the terms.” Exclusions for pre-existing medical conditions, adventure activities, and self-inflicted situations are standard. Missing them means denied claims.

Travellers planning longer or multi-destination trips face the greatest exposure. A two-week itinerary across several countries with prepaid accommodation, excursions, and internal flights contains far more financial risk than a simple return flight. An airline plan covers only the international leg, leaving everything else unprotected.

When should you choose airline insurance versus comprehensive cover?

The right choice depends on your trip type, the total financial investment at risk, and your personal health situation. Airline protection plans are best for simple, domestic round trips with low-cost add-on coverage for cancellation and delays. Comprehensive travel insurance is better for international and complex trips requiring more extensive coverage.

Use this framework to decide:

- Calculate your total non-refundable spend. Add up flights, hotels, tours, and any prepaid activities. If the total is significant and non-refundable, an airline plan alone leaves most of it exposed.

- Assess your medical risk. If you have a pre-existing condition, are travelling to a country with expensive healthcare, or are planning physically demanding activities, the medical limits of an airline plan are almost certainly inadequate. Review medical coverage abroad options before you commit.

- Check your destination. Domestic trips with refundable bookings carry less financial risk. International trips, especially to the United States, Japan, or Australia, carry high medical cost exposure that airline plans cannot adequately address.

- Review what you already have. Some credit cards include trip cancellation and baggage cover. If your card already covers flight disruptions, paying for an airline plan duplicates that cover without adding value.

- Consider your trip complexity. A direct return flight to a single city is a simple trip. A multi-stop itinerary with connecting flights, cruises, and guided tours is complex. Complexity increases the number of things that can go wrong and the financial consequences of each.

Pro Tip: If you want the convenience of an airline plan but need broader protection, check whether the airline plan can sit alongside a supplemental travel medical policy. The two together can cover flight disruptions and higher medical costs without paying for a full comprehensive plan.

Airline policies also include a ‘free look’ period of typically 15 days, allowing a full refund before departure or before any claims begin. Use that window to compare the policy against a comprehensive alternative before committing.

Key takeaways

Airline insurance covers flight-related disruptions only, with medical limits of £10,000–£50,000 and baggage limits of £500–£1,000, making comprehensive travel insurance the stronger choice for international or high-value trips.

| Point | Details |

|---|---|

| Airline plans cover flights only | Trip cancellation, delays, and baggage apply to the flight portion, not hotels or tours. |

| Medical limits are low | Cover of £10,000–£50,000 is often insufficient for serious overseas treatment or evacuation. |

| Baggage claims have strict timelines | Delay benefits trigger after 12–24 hours; permanent loss claims require 14–21 days. |

| Comprehensive cover protects more | Full travel insurance covers the entire trip cost, including non-flight expenses and higher medical limits. |

| Use the free look period | Most airline plans allow a 15-day cancellation window for a full refund before departure. |

My honest view on airline insurance and what travellers get wrong

I have reviewed a great many travel insurance policies over the years, and the pattern I see most often is this: travellers buy airline insurance because it appears at checkout, it is cheap, and it feels like the responsible thing to do. Then something goes wrong, and they discover the policy does not cover what they assumed it would.

The free look period is one of the most underused consumer protections in travel. Most travellers never read the policy at all, let alone within 15 days of purchase. If you did read it, you would almost always find reasons to either upgrade or replace it with a comprehensive plan.

The medical coverage gap is the issue I find most concerning. Travelling to the United States, for example, with only £50,000 of medical cover is a genuine financial risk. A serious accident or illness requiring hospitalisation and repatriation can easily exceed that figure. Comprehensive plans with travel medical cover offer significantly higher limits and include evacuation, which airline plans rarely do.

My recommendation is straightforward. For a simple domestic return flight with refundable bookings, an airline plan is adequate. For anything international, multi-stop, or involving significant prepaid costs, buy a comprehensive policy. The price difference is modest compared to the financial exposure you are accepting without it.

— Coert

Travel protection that goes beyond your flight

Airline insurance is a starting point, not a complete solution. If your trip involves international travel, prepaid accommodation, or any health concerns, you need cover that matches the full scope of your plans.

Unparalleledglobalbenefits specialises in international insurance solutions for travellers, expats, students, and families. Whether you need a single-trip policy with high medical limits or a plan that covers complex multi-destination itineraries, the team can match you to the right level of protection. Explore your options with the travel insurance guide or review comprehensive travel insurance options to find a plan that covers your entire trip, not just your flight.

Planning a trip for yourself, a resident, or visiting family? UGB + Ekta can arrange travel insurance for seniors up to 100 years old. Just click here: https://ektatraveling.com/?partner_uid=808 and add the promo code “UGB” to receive an additional 10% discount.

Watch this short overview to understand how travel insurance works in practice:

https://youtu.be/bjzvma7Sh1g

FAQ

What does airline insurance cover?

Airline insurance covers trip cancellation, flight delays, baggage loss or delay, and limited emergency medical expenses. Coverage applies to the flight portion of your trip only, not hotels, tours, or other prepaid expenses.

Is airline insurance the same as travel insurance?

No. Airline plans focus narrowly on the flight and have lower coverage limits, while comprehensive travel insurance covers the full trip cost, higher medical limits, and non-flight expenses.

How much medical cover does airline insurance provide?

Airline protection plans typically provide accident medical coverage of £10,000–£50,000. That amount is often insufficient for serious overseas hospitalisation or medical evacuation, which comprehensive plans cover at significantly higher limits.

When does baggage delay cover activate?

Baggage delay benefits generally trigger after 12–24 hours of missing luggage. Carriers declare baggage permanently lost only after 14–21 days, which is when a permanent loss claim becomes valid under most policies.

Can I cancel an airline insurance policy after buying it?

Most airline insurance policies include a free look period of approximately 15 days, allowing a full refund if you cancel before your departure date and before making any claims.

Recommended

- What is covered in travel insurance: 2026 guide – Unparalleled Global Benefits

- Flight insurance coverage 2026: Protect against 40% uncovered risks – Unparalleled Global Benefits

- How does travel insurance work: your 2026 guide – Unparalleled Global Benefits

- What does travel health insurance cover: your 2026 guide – Unparalleled Global Benefits