TL;DR:

- Choosing the right medical insurance involves calculating total annual costs by combining premiums and expected out-of-pocket expenses based on your health needs. Verifying provider networks by name is essential to avoid coverage surprises, especially for frequent or complex care. Matching your plan type to your health profile helps you balance costs and risk, ensuring better financial protection.

Knowing how to compare medical insurance means evaluating total annual cost against your personal health needs, not just picking the lowest monthly premium. The right plan balances premiums, deductibles, copays, coinsurance, and out-of-pocket maximums against how often you actually use healthcare. A plan that looks cheap in january can cost far more by december if your deductible is high and you need regular care. This guide gives you a clear, step-by-step framework for private medical insurance comparison, so you choose coverage that fits your health profile and your budget.

What key terms must you understand before comparing medical insurance?

Accurate health cover comparison starts with knowing exactly what each cost component means. Without this foundation, you cannot make a fair comparison between any two plans.

| Term | Definition |

|---|---|

| Premium | The fixed monthly amount you pay to keep the plan active, regardless of whether you use healthcare. |

| Deductible | The amount you pay out of pocket each year before the insurer starts sharing costs. |

| Copay | A fixed fee you pay per visit or service, such as £25 per GP appointment. |

| Coinsurance | Your share of costs after meeting the deductible, expressed as a percentage (e.g. 20%). |

| Out-of-pocket maximum | The most you will pay in a year; the insurer covers 100% of costs beyond this point. |

One critical distinction catches many people off guard. Premiums do not count toward your deductible or out-of-pocket maximum. Your true financial exposure in a worst-case year is your total annual premiums plus your out-of-pocket maximum, not one or the other.

Pro Tip: Add your annual premium to your plan’s out-of-pocket maximum. That total is the absolute most you could pay in a bad health year. Compare that figure across plans, not just the monthly premium.

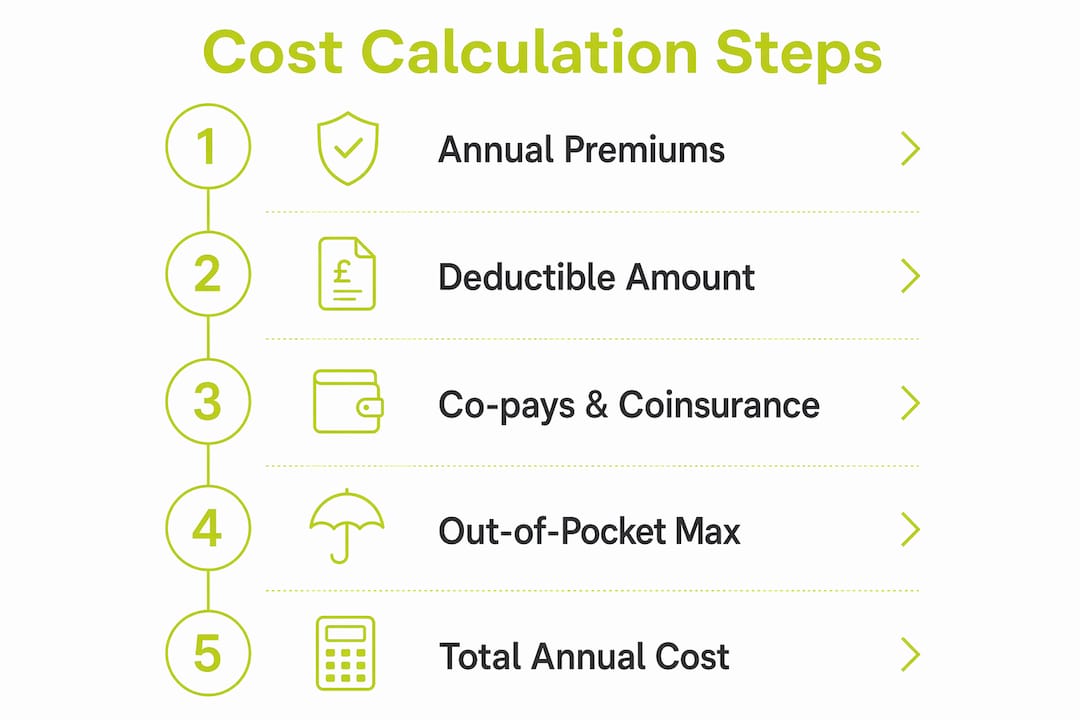

How do you calculate total annual cost when comparing health care plans?

Accurate comparison requires calculating total annual cost by combining yearly premiums with expected out-of-pocket expenses based on your anticipated healthcare use. This is the single most important step in any compare health insurance plans exercise.

Follow these steps to build your total cost estimate:

- Calculate your annual premium. Multiply the monthly premium by 12. For context, a Silver-level plan for a 40-year-old costs around $539 per month in 2026 before subsidies. That figure alone shows why monthly cost is only part of the picture.

- Estimate your deductible spend. If you visit a doctor four times a year and need one specialist referral, estimate how much of your deductible you are likely to meet. Low users rarely hit their full deductible; high users often do.

- Add expected copays and coinsurance. Count your typical annual appointments, prescriptions, and any planned procedures. Multiply each by the relevant copay or coinsurance rate.

- Factor in prescription costs. Check which tier your regular medications fall under. Tier 1 generics cost far less than Tier 3 or Tier 4 branded drugs.

- Subtract employer contributions. If your employer contributes to a Health Savings Account (HSA) or Health Reimbursement Arrangement (HRA), deduct that amount from your estimated out-of-pocket spend.

- Compare the totals, not the premiums. A plan with a £150 monthly premium and a £4,000 deductible can cost more annually than a plan with a £220 premium and a £1,500 deductible, depending on your usage.

For a deeper look at how these figures interact across international plans, the guide on understanding true insurance costs at Unparalleledglobalbenefits walks through real calculations with worked examples.

Pro Tip: Run two scenarios: one where you stay healthy all year, and one where you hit your out-of-pocket maximum. The plan that wins in both scenarios is your safest choice.

What role do provider networks and prescription coverage play in comparing plans?

The cost calculation tells you what a plan might cost. The network tells you whether that plan actually works for your life. HMOs carry lower premiums but require referrals and restrict you to in-network providers. PPOs offer more flexibility and out-of-network coverage but charge higher premiums. EPOs sit in between, with no referral requirement but strict network limits.

Before you enrol in any plan, check these network factors:

- Verify your specific doctors by name and identifier. Networks can have sub-networks that shift without notice. Do not assume a hospital is covered because the insurer’s website lists it generally. Call the insurer and confirm your GP, specialist, and preferred hospital are all in-network.

- Check prescription drug tiers. Every plan has a formulary, a list of covered drugs organised by tier. A medication you take daily could be Tier 1 on one plan and Tier 3 on another, changing your annual cost significantly.

- Assess out-of-network rules. If you travel frequently or live between locations, a PPO’s out-of-network coverage may justify its higher premium. An HMO could leave you with no cover if you need care away from your registered area.

- Confirm mental health and specialist access. Some plans require multiple referral steps before you can see a specialist. If you manage a chronic condition, that delay has real consequences.

Pro Tip: Do not rely on the insurer’s online directory alone. Call the provider’s office directly and ask whether they accept your specific plan and plan year. Directories are updated infrequently and errors are common.

How should personal health needs shape your insurance comparison?

There is no universally best plan; the right choice depends entirely on your health usage and financial risk tolerance. Matching your profile to the right plan structure saves money and prevents coverage gaps.

Consider which profile fits you best:

- Low healthcare user. You rarely see a doctor, take no regular medications, and have no chronic conditions. A high-deductible plan with a low premium makes financial sense. You are unlikely to meet the deductible, so you pay less overall.

- Moderate healthcare user. You have one or two ongoing prescriptions, see a GP a few times a year, and occasionally need specialist care. A mid-tier plan with a moderate deductible and reasonable copays usually produces the lowest total annual cost.

- High healthcare user or chronic condition manager. You need regular specialist visits, ongoing prescriptions, or planned procedures. A plan with a higher premium but lower deductible and out-of-pocket maximum protects you from large bills. Choosing a low-premium, high-deductible plan in this situation, sometimes called “deductible myopia,” can be significantly more expensive across the year.

The trade-off is straightforward: lower premiums shift financial risk onto you through higher deductibles and copays. Higher premiums transfer that risk to the insurer. Your job is to decide how much risk you can comfortably absorb. For readers managing pre-existing conditions, the guide on travel insurance with medical conditions at Unparalleledglobalbenefits covers how health history affects plan selection in detail.

What practical steps make the comparison process more effective?

A structured approach to comparing medical plans prevents the most common and costly mistakes. Follow this sequence when you are ready to compare health insurance providers.

- List your non-negotiables first. Write down your current doctors, your regular medications, and any planned procedures. These are your filters. Any plan that does not cover them is off the list before you look at price.

- Use online comparison calculators. Reputable calculators factor in monthly premium, deductible, coinsurance, copays, out-of-pocket maximum, and employer HSA or HRA contributions. They give you a projected annual cost rather than a monthly snapshot.

- Search beyond comparison sites. Third-party comparison sites often feature sponsored results influenced by insurer fees. Broaden your search to include direct insurer websites and independent brokers to avoid recommendations shaped by commission.

- Compare plan categories, not just prices. Use a feature-by-feature review rather than a price-only ranking.

| Feature category | What to check |

|---|---|

| Annual premium | Total yearly cost, not monthly figure |

| Deductible | Individual and family limits |

| Copays and coinsurance | Per visit and per service rates |

| Out-of-pocket maximum | Worst-case annual exposure |

| Network type | HMO, PPO, or EPO and referral rules |

| Prescription formulary | Tier placement of your medications |

| Mental health cover | Parity with physical health benefits |

- Verify everything before you sign. Confirm network participation directly with providers, check the formulary for your specific drug names, and read the summary of benefits document, not just the marketing brochure.

“The biggest mistake people make when comparing health plans is treating the monthly premium as the total cost. Your real annual exposure is premiums plus your potential out-of-pocket maximum. Run that number for every plan before you decide.”

For a detailed walkthrough of comparing plans abroad, Unparalleledglobalbenefits has a dedicated resource on comparing medical insurance plans abroad that applies these same principles to international coverage.

Key takeaways

Comparing medical insurance plans accurately requires calculating total annual cost, verifying provider networks by name, and matching plan structure to your personal health usage and financial risk tolerance.

| Point | Details |

|---|---|

| Total annual cost is the true metric | Add annual premiums to your out-of-pocket maximum to find your real worst-case exposure. |

| Premiums do not reduce your deductible | Premiums are a sunk cost; your deductible and out-of-pocket maximum are separate financial obligations. |

| Verify networks by name, not by list | Call providers directly to confirm in-network status before enrolling in any plan. |

| Match plan type to your health profile | Low users benefit from high-deductible plans; frequent users save money with lower deductibles despite higher premiums. |

| Comparison sites may carry bias | Sponsored results on aggregator sites can skew recommendations; always cross-check with direct insurer sources. |

Why I think most people compare insurance plans the wrong way

After years of working through international insurance options with clients across dozens of countries, I have seen the same mistake repeated constantly. People open a comparison site, sort by monthly premium, and pick the cheapest option. That approach works fine if you never get ill. It fails badly the moment you actually need care.

The number that matters is not the monthly premium. It is the sum of your annual premiums and your out-of-pocket maximum. That is your true worst-case cost for the year. A plan charging £180 per month with a £5,000 out-of-pocket maximum costs you £7,160 at most. A plan charging £120 per month with an £8,000 maximum costs you £9,440. The “cheaper” plan is £2,280 more expensive if you have a serious health event.

The second mistake I see is assuming networks. People enrol in a plan because their GP’s name appears on a general list, then discover mid-year that the GP is no longer contracted or sits in a sub-network with different cost-sharing rules. Verifying your specific provider by name and identifier before you sign is not optional. It takes ten minutes and can save thousands.

My honest advice: treat the comparison process like a financial calculation, not a shopping exercise. Build your two cost scenarios, verify your networks personally, and only then look at the premium. The plan that survives both scenarios is the one worth buying.

— Coert

How Unparalleledglobalbenefits supports your international health cover needs

Choosing the right plan is complex enough domestically. Add an international move, an expat assignment, or a long-term stay abroad, and the variables multiply quickly.

Unparalleledglobalbenefits specialises in exactly this situation. The platform offers tailored international health insurance solutions for expats, travellers, students, families, and visitors, with plans designed to match your specific health profile and destination. Whether you need essential cover for expats or a plan that covers pre-existing conditions across borders, the team at Unparalleledglobalbenefits can guide you through the options. Request a quote today and get coverage that reflects your real needs, not just the lowest headline price.

Planning a trip for yourself, a resident, or visiting family? UGB + Ekta can arrange travel insurance for seniors up to 100 years old. Just click here: https://ektatraveling.com/?partner_uid=808 and add the promo code “UGB” to receive an additional 10% discount.

Watch this short video for more guidance on choosing the right international health cover:

https://youtu.be/bjzvma7Sh1g

FAQ

What is the most important factor when comparing medical insurance?

Total annual cost is the most important factor. Add your yearly premiums to your plan’s out-of-pocket maximum to find your true worst-case financial exposure before comparing plans.

What is the difference between a deductible and an out-of-pocket maximum?

The deductible is the amount you pay before the insurer shares costs. The out-of-pocket maximum is the most you will pay in a year; costs above that threshold are covered entirely by the insurer.

How do HMO, PPO, and EPO plans differ?

HMOs require referrals and restrict care to in-network providers. PPOs offer out-of-network flexibility at a higher premium. EPOs have no referral requirement but enforce strict network limits.

Should I trust comparison websites for health cover comparison?

Use them as a starting point only. Comparison sites often feature sponsored results influenced by insurer fees, so cross-check findings directly with insurers or independent brokers.

How does a chronic condition affect which plan I should choose?

Chronic conditions typically mean higher healthcare usage. A plan with a higher premium but lower deductible and out-of-pocket maximum usually produces a lower total annual cost for frequent healthcare users than a low-premium, high-deductible alternative.

Recommended

- Private health insurance price comparison: your 2026 guide – Unparalleled Global Benefits

- Compare student health insurance: your 2026 guide – Unparalleled Global Benefits

- Multi-country travel insurance: your 2026 guide – Unparalleled Global Benefits

- Expat health insurance: your complete guide for 2026 – Unparalleled Global Benefits