TL;DR:

- Travel insurance one cover combines medical, cancellation, and baggage protection into a single policy, simplifying travel plans. It typically costs 5% to 10% of the trip value and offers digital passes for quick access during emergencies. Choosing the right policy depends on personal risk, trip specifics, and declaring pre-existing conditions to ensure comprehensive coverage.

Travel insurance one cover is a single, all-inclusive policy that protects international travellers against the most common risks of global travel, including emergency medical treatment, trip cancellations, and baggage loss. Rather than buying separate policies for each risk, you consolidate everything into one plan. This approach simplifies your travel preparation and reduces the chance of gaps in protection. For expatriates and frequent travellers, a single consolidated policy also makes claims management far less stressful. Unparalleledglobalbenefits works with international travellers daily, and the question we hear most often is: “Do I really need all this cover?” The answer is almost always yes.

What does travel insurance one cover typically include?

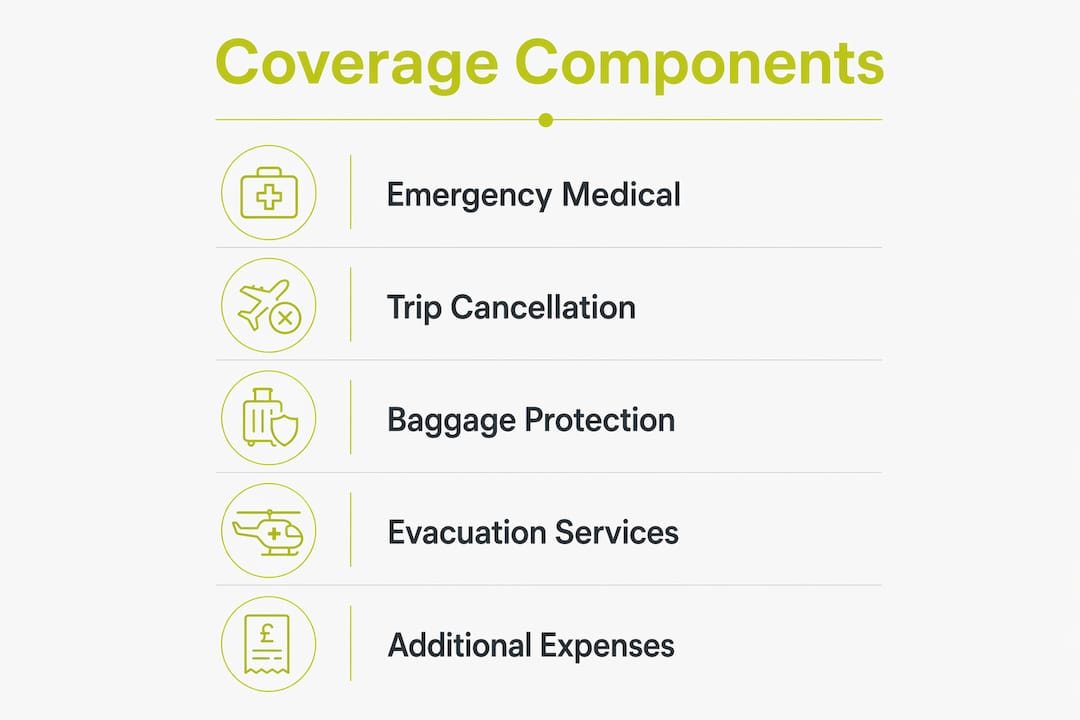

A consolidated travel policy bundles several distinct protections into one document. Travel insurance policies typically cover trip cancellations, lost baggage, additional expenses, and emergency medical assistance. Understanding what each component does helps you assess whether a policy genuinely meets your needs.

Emergency medical treatment and evacuation

Emergency medical evacuation is a vital part of travel insurance for expatriates and international travellers. It covers transport to appropriate healthcare facilities when you suffer a serious illness or injury abroad. Without this cover, an air ambulance from Southeast Asia or South America can cost tens of thousands of pounds out of pocket.

Trip cancellation and interruption

Trip cancellation cover reimburses your pre-paid, non-refundable costs if you must cancel before departure due to illness, bereavement, or other covered events. Trip interruption cover applies when you need to cut a trip short after it has already begun. Both protections are particularly valuable for travellers booking expensive long-haul itineraries.

Baggage, delays, and additional expenses

Lost, stolen, or delayed baggage cover replaces essential items when your luggage goes missing. Additional expenses cover pays for unexpected costs such as emergency accommodation when a flight is cancelled. Some policies also include car rental excess cover, which removes the need to purchase separate protection at the hire desk.

Coverage summary table

| Coverage component | What it protects | Typical limit range |

|---|---|---|

| Emergency medical treatment | Hospital and doctor fees abroad | £1,000,000+ |

| Medical evacuation | Air ambulance and repatriation | £500,000+ |

| Trip cancellation | Pre-paid, non-refundable costs | Up to total trip cost |

| Baggage loss or theft | Replacement of personal belongings | £1,500–£3,000 |

| Travel delay | Accommodation and meals | £200–£500 |

| Car rental excess | Damage excess waiver | £1,500–£3,000 |

Coverage limits and exclusions vary between providers, so reading the policy schedule carefully is non-negotiable.

Pro Tip: Always check the single-item limit within baggage cover. Many policies cap individual items at £250–£500, which may not cover a laptop or camera. Declare high-value items separately if needed.

How are travel insurance one cover policy costs calculated?

Comprehensive travel insurance typically costs between 5% and 10% of the total trip cost. That means a £4,000 holiday could carry a premium of £200–£400 for full cover. The range reflects how much individual circumstances affect pricing.

The four main variables that drive your premium are:

- Total trip cost: Higher pre-paid costs mean greater cancellation exposure for the insurer.

- Traveller age: Older travellers carry higher medical risk, which increases premiums.

- Trip duration: Longer trips extend the window of potential claims.

- Coverage amount chosen: Higher limits and lower excesses raise the premium.

Medical-only plans cost significantly less than consolidated policies, but they leave you exposed on cancellations, baggage, and delays. For most international travellers, the additional cost of full cover is modest relative to the financial risk it removes.

Annual multi-trip policies are often more cost-effective for frequent travellers than purchasing single-trip policies repeatedly. A yearly plan provides ongoing emergency medical, evacuation, and delay coverage across multiple trips within 12 months. If you travel more than twice a year, the maths almost always favour an annual plan.

Pro Tip: When comparing quotes, do not focus solely on the headline premium. Check the medical excess, the cancellation sub-limit, and whether pre-existing conditions are included. A cheaper policy with a £500 medical excess can cost far more in practice.

What technological innovations improve the one cover experience?

Modern travel insurance providers now offer digital insurance passes that travellers can add directly to smartphone wallets for instant access to policy information and emergency contacts. This development removes the need to carry physical documents or search through emails during a crisis. The shift mirrors the broader digitalisation of travel documents, where boarding passes and hotel bookings already live in the same wallet.

The practical benefits during a medical emergency are significant. Hospitals overseas may require confirmation of insurance or upfront payment before treatment. Ready access to digital policy details on your phone prevents delays and gives medical staff the information they need immediately. That speed can matter enormously when you are unwell and far from home.

Digital passes also centralise claims links and assistance contacts in one place. Rather than calling an international number from memory or hunting for a policy number, you tap once and reach the right team. 1Cover’s digital travel insurance pass is one example of this feature being integrated into a consumer product.

“The integration of insurance passes into digital wallets reflects travel technology trends and improves crisis responsiveness.” — Travel Monitor

Secure digital access to insurance documents is increasingly integrated with boarding passes and hotel bookings in travellers’ smartphone wallets. This trend confirms that the industry is moving towards frictionless, mobile-first insurance management. Travellers who have not yet adopted this approach are carrying unnecessary administrative risk.

How to choose the right one cover policy for your trip

Choosing the right policy requires matching your personal circumstances to the right coverage structure. The correct coverage depends on your health, travel duration, and destination risks. A traveller heading to the United States needs far higher medical limits than someone visiting Europe, where reciprocal health agreements may provide partial state cover.

Follow these steps to select the best policy:

- Assess your personal risk profile. Consider your age, any existing health conditions, and the activities you plan to undertake. Adventure sports such as skiing or diving typically require add-on cover or a specialist policy.

- Compare benefits, exclusions, and coverage limits. Do not compare premiums alone. A policy with a low premium but a high medical excess or a sub-standard cancellation limit may leave you significantly out of pocket.

- Check the provider’s claims reputation. Read independent reviews and check how quickly the insurer processes claims. A policy is only as good as the company behind it.

- Disclose pre-existing medical conditions. Pre-existing conditions may require specialised coverage or disclosure to ensure valid protection. Failing to declare a condition can void your entire policy at the point of claim.

- Consider annual cover if you travel frequently. Expatriates and business travellers who take multiple trips per year should evaluate annual multi-trip plans. The per-trip cost is almost always lower, and the ongoing protection removes the risk of travelling uninsured between purchases.

Pro Tip: Buy your policy as soon as you book your trip, not just before departure. Cancellation cover only applies from the date of purchase, so early purchase protects your deposit from day one.

Planning a trip for yourself, a resident, or visiting family? UGB + Ekta can arrange travel insurance for seniors up to 100 years old. Just click here: https://ektatraveling.com/?partner_uid=808 and add the promo code “UGB” to receive an additional 10% discount.

For a broader view of what digital nomads and long-term travellers need from their cover, the digital nomad insurance guide from Tools for Expats offers useful context on international access and policy flexibility.

Key takeaways

A single consolidated travel policy delivers the broadest protection at the lowest administrative burden, making it the most practical choice for international travellers and expatriates.

| Point | Details |

|---|---|

| Consolidated cover reduces gaps | One policy covering medical, cancellation, and baggage removes the risk of overlapping exclusions. |

| Cost is 5%–10% of trip value | Budget this amount when planning any international trip to avoid underinsurance. |

| Annual plans suit frequent travellers | Multi-trip yearly policies cost less per trip and provide continuous protection. |

| Digital passes speed up emergencies | Smartphone wallet access to policy details prevents treatment delays at overseas hospitals. |

| Declare pre-existing conditions | Non-disclosure can void a claim entirely, regardless of how much you paid for the policy. |

Why I always recommend buying cover before you pack

After years of advising international travellers and expatriates on insurance decisions, the pattern I see most often is this: people underestimate risk until something goes wrong. A traveller who skips comprehensive cover to save £80 on a premium can face a £15,000 hospital bill in the United States or a £6,000 repatriation flight from a remote destination. The maths are not close.

What surprises most travellers is how often trip cancellation cover proves its worth before the trip even begins. A sudden illness, a family bereavement, or an unexpected work obligation can wipe out thousands in non-refundable bookings. Buying cover the same day you book your flights protects that investment from the start.

I also see too many travellers rely on fragmented cover: one policy for medical, another for baggage, and a credit card benefit for cancellations. The problem is that each policy has its own exclusions, and when a claim spans two categories, each insurer points to the other. A single consolidated policy removes that ambiguity entirely.

The digital pass development is one of the most genuinely useful advances I have seen in travel insurance. Having your policy number, emergency contact, and claims link in your phone wallet is not a gimmick. When you are unwell abroad and your hands are shaking, the last thing you need is to search through your email inbox.

My consistent advice: buy early, buy comprehensive, and make sure your policy lives on your phone.

— Coert

Unparalleledglobalbenefits: expert guidance for international travellers

Finding the right policy across dozens of providers is time-consuming and easy to get wrong. Unparalleledglobalbenefits specialises in international insurance solutions for expatriates, frequent travellers, and families living or working abroad.

Whether you need single trip cover for expats or a fully tailored annual plan, the team at Unparalleledglobalbenefits can match your circumstances to the right policy. For expatriates weighing up their long-term options, the guide to selecting the right expat insurance provider is a practical starting point. Unparalleledglobalbenefits also arranges cover for seniors up to 100 years old through its partnership with Ekta. Use the promo code “UGB” at ektatraveling.com for an additional 10% discount.

FAQ

What is travel insurance one cover?

Travel insurance one cover is a single policy that combines emergency medical, trip cancellation, baggage, and travel delay protection into one plan. It removes the need to purchase and manage multiple separate policies.

How much does a one cover travel policy cost?

Comprehensive travel insurance typically costs between 5% and 10% of your total trip cost, depending on your age, trip duration, and the coverage limits you choose.

Does one cover travel insurance include pre-existing conditions?

Pre-existing medical conditions may require specialised coverage or disclosure. Always declare any conditions when purchasing your policy, as non-disclosure can void a claim.

Is an annual multi-trip plan better value than single-trip cover?

Annual multi-trip policies are often more cost-effective for travellers who take more than two trips per year, as they provide continuous protection across all trips within 12 months.

What happens if I need emergency treatment abroad without my documents?

Digital insurance passes stored in your smartphone wallet give you instant access to your policy number and emergency contacts, preventing delays at overseas hospitals where proof of cover may be required before treatment begins.

Recommended

- Multi-country travel insurance: your 2026 guide – Unparalleled Global Benefits

- What does travel health insurance cover: your 2026 guide – Unparalleled Global Benefits

- What is covered in travel insurance: 2026 guide – Unparalleled Global Benefits

- Choosing travel insurance: expert guidance for global trips – Unparalleled Global Benefits