TL;DR:

- Travel insurance provides financial protection by reimbursing travelers for covered losses during trips. Buying early ensures access to full benefits, including pre-existing condition waivers and Cancel for Any Reason options. Proper documentation and understanding policy exclusions are essential to avoid claim denials and unexpected expenses.

Travel insurance is a financial protection plan that reimburses travellers for specific covered losses and emergencies incurred during a trip. Understanding how travel insurance works is the single most important step before booking any international or domestic journey. A comprehensive travel insurance policy typically costs between 4% and 10% of your total prepaid, nonrefundable trip expenses. That figure gives you an immediate sense of the financial stakes involved. Get the coverage right, and you protect hundreds or thousands of pounds in prepaid costs.

How does travel insurance work and what does it cover?

Travel insurance operates on a straightforward principle: you pay a premium before your trip, and the insurer reimburses you if a covered event disrupts or cancels your plans. The policy lists specific “covered reasons,” and only losses that match those reasons qualify for a payout. Think of it as a contract between you and the insurer, not a blank cheque for any misfortune.

Most standard policies bundle several types of protection together. The table below shows the most common coverage categories, what they protect against, and a real-world example for each.

| Coverage type | What it protects | Example |

|---|---|---|

| Trip cancellation | Prepaid, nonrefundable costs if you cancel for a covered reason | Serious illness forces you to cancel a £3,000 holiday |

| Trip interruption | Costs to return home early or rejoin a trip | A family bereavement cuts your trip short |

| Trip delay | Meals, transport, and lodging during a delay of at least six hours | A flight is grounded overnight due to a technical fault |

| Emergency medical | Hospital bills, doctor fees, and treatment abroad | You fracture your wrist skiing in Austria |

| Medical evacuation | Transport to the nearest adequate hospital or home | A remote trekking accident requires helicopter evacuation |

| Baggage loss or delay | Replacement of lost items or essentials during a baggage delay | Your luggage goes missing for 12 hours on arrival |

| Accidental death | Lump sum benefit for fatal accidents during travel | A fatal road accident abroad |

Pro Tip: Emergency medical evacuation can cost tens of thousands of pounds without insurance. If you plan to travel to remote destinations, check that your policy includes medical evacuation as a named benefit, not just emergency medical treatment. The Unparalleledglobalbenefits evacuation coverage guide explains exactly what to look for.

Travel insurance also operates as secondary coverage in many situations. Airlines compensate for luggage loss first, and your travel insurer covers amounts beyond those airline limits. Knowing this hierarchy prevents unpleasant surprises at claim time.

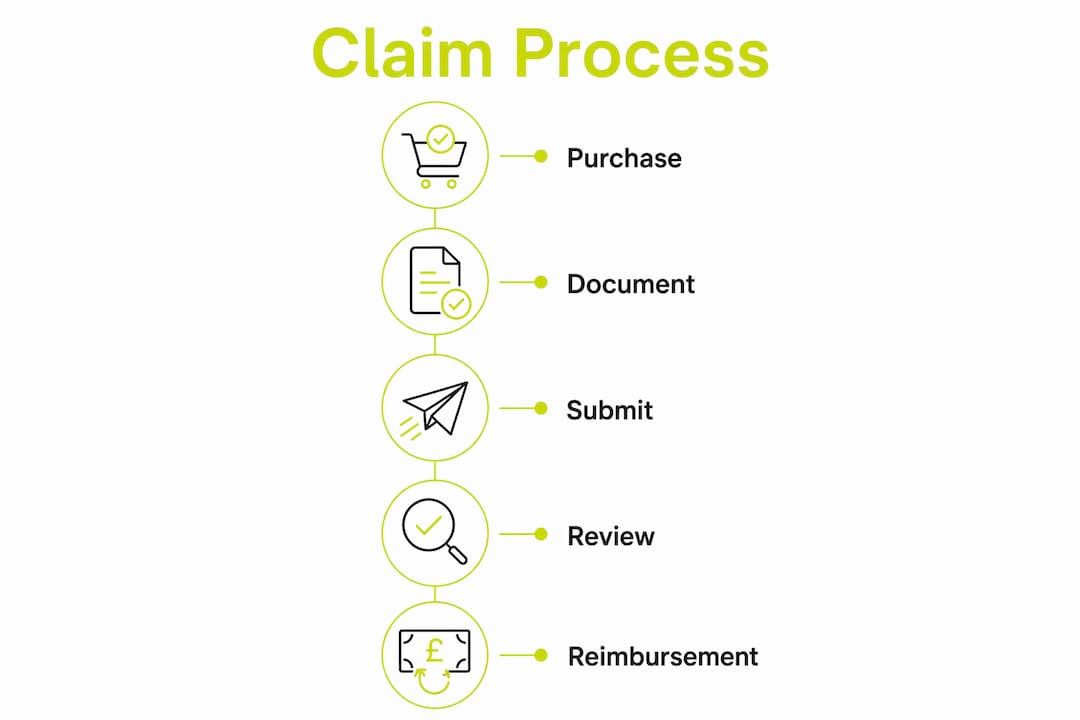

How does the travel insurance claim process work?

The claims process follows a clear sequence, and knowing it in advance saves considerable stress. Travel insurance most commonly operates on a reimbursement model, meaning you pay upfront for emergency medical care or other covered costs, then submit a claim for repayment afterwards. Direct billing at partner hospitals exists but is less common. If your insurer offers a cashless network, use it wherever possible to avoid large out-of-pocket payments.

The standard claim process runs as follows:

- Record everything immediately. Keep all receipts, medical reports, police reports for theft, and written confirmation from airlines for delays or cancellations.

- Notify your insurer promptly. Most policies require you to contact the insurer within a set window, often 24–72 hours of the incident. Missing this deadline can invalidate your claim.

- Complete the claim form. Download or request the official form from your insurer. Fill it in accurately and attach all supporting documents.

- Submit and follow up. Send your claim by the method specified in your policy. Keep copies of everything you submit.

- Await review and payout. Insurers typically review straightforward claims within 5–15 business days. Complex medical claims can take longer.

Deductibles reduce your payout. If your policy carries a £100 deductible and your claim is £400, you receive £300. Policy limits also cap payouts per category, so a policy with a £500 baggage limit will not reimburse a £1,200 camera. Read those limits before you buy.

Pro Tip: File a police report within 24 hours of any theft abroad. Without it, most insurers will reject a baggage or personal effects claim outright. The same applies to written confirmation from your airline for any lost or delayed luggage.

What do travellers most often misunderstand about travel protection?

Several misconceptions about travel protection cost travellers money every year. Understanding these gaps is as important as understanding what a policy covers.

- Credit card travel benefits are narrow. Only 32% of consumer credit cards offer any form of travel insurance benefit, and those benefits are typically limited to narrow scenarios such as lost luggage. They rarely include emergency medical cover, which is the most expensive risk you face abroad.

- Pre-existing condition waivers have strict deadlines. Pre-existing condition waivers require policy purchase within 14–21 days of your first trip payment. Wait longer, and any medical claim linked to a known health condition will likely be denied. This is one of the most costly timing mistakes travellers make.

- “Cancel for any reason” is an upgrade, not a standard feature. A standard policy only pays out for cancellations that match a listed covered reason. Cancel for Any Reason upgrades reimburse 50%–75% of prepaid nonrefundable expenses and must be purchased early after booking. They cost more, but they give you genuine flexibility.

- Dangerous activities are frequently excluded. Medical issues linked to activities such as skydiving, bungee jumping, or off-piste skiing are often excluded from standard policies. If your trip involves adventure sports, you need a specialist policy or a specific activity rider.

- Baggage loss takes time to confirm. Baggage loss is only declared after 14–21 days of persistent searching by the carrier. Baggage delay coverage, by contrast, triggers after just 6–24 hours. These are two separate benefits with different claim processes.

“Insurance reimbursements are only paid for covered reasons. Cancellations for a simple change of mind require a specific Cancel for Any Reason upgrade, which is costlier and provides only partial reimbursement.” — Lonely Planet Travel Insurance Guide

If you have existing medical conditions, the Unparalleledglobalbenefits guide on travel insurance with medical conditions explains how to find policies that cover your specific situation.

How to choose the right travel insurance plan for your trip

The right policy depends on what you stand to lose financially, not just on the premium price. Travel insurance delivers most value when you have significant financial risk, such as a costly international trip with large prepaid, nonrefundable expenses. A weekend domestic trip with no prepaid costs may need only basic medical cover.

Ask yourself these questions before comparing plans:

- How much have I prepaid and cannot recover? Add up flights, hotels, tours, and any other nonrefundable bookings. That total is your financial exposure for trip cancellation cover.

- Does my existing health insurance cover me abroad? Most domestic health plans do not cover treatment in foreign countries. If yours does not, emergency medical cover is non-negotiable. The Unparalleledglobalbenefits article on health insurance abroad explains the gap clearly.

- What activities will I be doing? Standard policies exclude many adventure sports. If you plan to ski, dive, or climb, confirm your policy covers those activities explicitly.

- Am I travelling with a pre-existing condition? If yes, buy your policy within 14–21 days of your first trip payment to qualify for a pre-existing condition waiver.

- Do I want full cancellation flexibility? If your plans might change for personal reasons, consider a Cancel for Any Reason upgrade at the time of purchase.

Pro Tip: Buy your policy on the same day you make your first trip payment. This is the single action that unlocks the widest range of benefits, including pre-existing condition waivers and Cancel for Any Reason eligibility. Waiting even a few weeks can permanently close those options.

For travellers planning adventure activities, the Unparalleledglobalbenefits winter sports travel insurance guide covers the specific riders and exclusions you need to review.

Key takeaways

Travel insurance works by reimbursing covered losses, and buying your policy within 14–21 days of your first trip payment unlocks the broadest protection available.

| Point | Details |

|---|---|

| Reimbursement model | You pay costs upfront during your trip, then claim repayment from your insurer afterwards. |

| Buy early for full benefits | Purchase within 14–21 days of your first payment to qualify for pre-existing condition waivers. |

| Secondary coverage applies | Airlines and primary carriers pay first; travel insurance covers amounts beyond those limits. |

| Credit cards are not enough | Only 32% of credit cards offer any travel benefit, and those rarely include emergency medical cover. |

| CFAR is an upgrade | Cancel for Any Reason cover reimburses 50%–75% of costs and must be added at purchase, not later. |

What I have learned from years of watching travellers get this wrong

The most common mistake I see is not buying too little insurance. It is buying the right insurance too late. Travellers spend hours comparing premiums and then purchase their policy two days before departure. By that point, the pre-existing condition waiver window has closed, Cancel for Any Reason is off the table, and they are left with a policy that looks complete but has significant gaps.

The second mistake is treating travel insurance as a formality. People buy it because their tour operator asks for it, not because they have genuinely assessed their risk. A traveller with £8,000 in nonrefundable bookings and a heart condition needs a very different policy from a student on a £500 backpacking trip. The premium is almost irrelevant compared to the financial exposure you are protecting.

My honest advice: read the exclusions list before you read the benefits list. The exclusions tell you what the policy will not do. The benefits list tells you what it might do, subject to conditions. Most claim disputes arise from exclusions the policyholder never read. Spend ten minutes on that section and you will avoid the majority of unpleasant surprises.

Finally, keep your documentation obsessively. A claim without receipts, medical reports, or police reports is a claim that will likely be denied. The insurer is not being unreasonable when they ask for evidence. They are following the terms of the contract you agreed to. Treat every expense during a disruption as a potential claim and document it accordingly.

— Coert

Travel insurance plans tailored to your trip, from Unparalleledglobalbenefits

Whether you are travelling internationally for the first time or managing complex coverage needs as a frequent traveller, Unparalleledglobalbenefits offers plans built for real-world travel risks.

From single trip insurance for a one-off holiday to international health insurance for extended stays abroad, the platform matches coverage to your specific destination, trip cost, and health profile. Expert guidance is available to help you read the fine print and choose the right plan before you depart.

Planning a trip for yourself, a resident, or visiting family? UGB + Ekta can arrange travel insurance for seniors up to 100 years old. Just click here: https://ektatraveling.com/?partner_uid=808 and add the promo code “UGB” to receive an additional 10% discount.

FAQ

What does travel insurance cover on a standard policy?

A standard travel insurance policy covers trip cancellation, trip interruption, emergency medical treatment, medical evacuation, baggage loss or delay, and trip delay expenses. Coverage applies only to events listed as “covered reasons” in the policy terms.

How does medical travel insurance work abroad?

Most medical travel insurance operates on a reimbursement model: you pay for treatment upfront and claim repayment afterwards. Some insurers offer direct billing at partner hospitals, which removes the need for upfront payment entirely.

When should I buy travel insurance?

Buy your policy on the same day you make your first trip payment. Purchasing within 14–21 days of that payment qualifies you for pre-existing condition waivers and Cancel for Any Reason upgrades, which are unavailable if you buy closer to departure.

Does credit card travel insurance replace a dedicated policy?

No. Only 32% of consumer credit cards offer any travel insurance benefit, and those benefits are typically limited to narrow scenarios such as lost luggage. Emergency medical cover, the most critical protection for international travel, is rarely included.

What is not covered by travel insurance?

Standard policies exclude cancellations for a change of mind, medical claims linked to undisclosed pre-existing conditions, and injuries from activities classified as dangerous, such as skydiving or off-piste skiing. A Cancel for Any Reason upgrade and specialist activity riders address some of these gaps.

Recommended

- Choosing travel insurance: expert guidance for global trips – Unparalleled Global Benefits

- What is covered in travel insurance: 2026 guide – Unparalleled Global Benefits

- Why travel with insurance: Stay safe abroad in 2026 – Unparalleled Global Benefits

- Multi-country travel insurance: your 2026 guide – Unparalleled Global Benefits