TL;DR:

- Cancel for Any Reason (CFAR) is an optional upgrade to standard travel insurance that offers partial reimbursement for trip cancellations for any reason. It must be purchased within 10–21 days of your first payment and insures 100% of non-refundable costs, providing 50%–80% coverage. CFAR offers flexible cancellation protection for costly, uncertain, or last-minute trips, but relies on timely, full-cost policy inclusion.

Trip insurance for any reason is an optional upgrade to a standard travel policy that allows you to cancel your trip for any cause whatsoever and receive partial reimbursement of your non-refundable, prepaid expenses. Known in the industry as Cancel For Any Reason (CFAR) coverage, this add-on fills the gap left by standard trip cancellation insurance, which only pays out for specific, documented emergencies. Providers such as Allianz offer reimbursement rates up to 80% of non-refundable costs, while most plans sit in the 50%–75% range. CFAR is not a standalone product. It must be purchased as an upgrade to an existing base policy, and the purchase window is strict.

What is cancel for any reason (CFAR) coverage and how does it work?

CFAR coverage reimburses a percentage of your prepaid, non-refundable trip costs when you cancel for a reason not covered by your standard policy. The reimbursement rate is typically 50%–75%, with select premium plans reaching 80%. That means if you paid £4,000 for a non-refundable holiday and cancel under a 75% CFAR plan, you recover £3,000.

CFAR is an optional add-on, not a standalone product. You must first purchase a base travel insurance policy, then add CFAR as an upgrade at the time of purchase. The purchase window is 10–21 days from your first trip payment. Miss that window and CFAR is simply unavailable to you, regardless of how far in advance your trip is.

Here is how the claims process works in practice:

- Cancel your trip for any reason you choose, whether that is anxiety about flying, a change of plans, or concern about political unrest at your destination.

- Notify your insurer at least 48–72 hours before your scheduled departure. Same-day cancellations do not qualify for CFAR reimbursement.

- Collect any refunds or vouchers from airlines, hotels, or tour operators first. Your insurer deducts prior refunds before calculating your CFAR payout.

- Submit your claim with documentation of your non-refundable costs and any supplier credits already received.

- Receive your partial reimbursement based on the percentage stated in your policy.

Common scenarios where CFAR proves its worth include pre-trip anxiety, a family member’s change of circumstances not meeting the “covered reason” threshold, or simply deciding a destination no longer appeals after a news event. Standard policies would pay nothing in these situations. CFAR pays you back a meaningful portion of what you spent.

Pro Tip: Read your policy’s definition of “non-refundable costs” carefully. Some insurers exclude costs you could have recovered from a supplier but chose not to pursue.

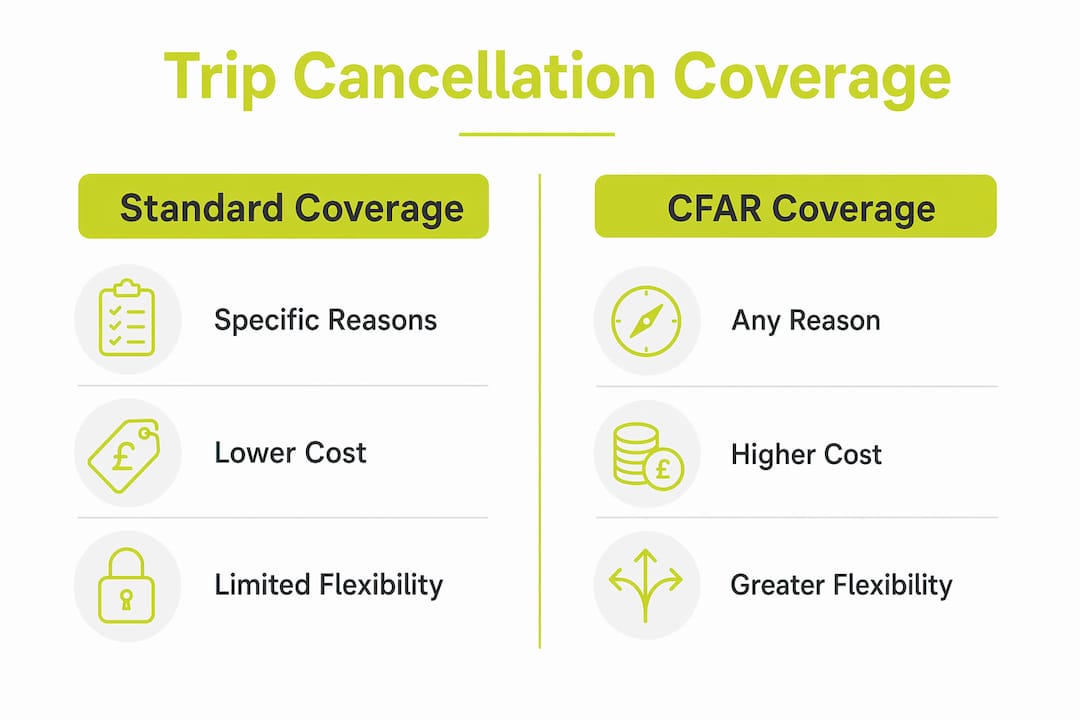

How does CFAR compare to standard trip cancellation coverage?

Standard trip cancellation insurance covers specific, documented reasons such as serious illness, death of a family member, jury duty, or a natural disaster at your destination. When one of those covered events occurs, you receive a full reimbursement of your non-refundable costs. CFAR covers everything else, but only partially.

The table below shows the core differences at a glance.

| Feature | Standard Trip Cancellation | CFAR Add-On |

|---|---|---|

| Covered reasons | Specific listed events only | Any reason whatsoever |

| Reimbursement rate | Up to 100% | Typically 50%–75%, up to 80% |

| Purchase timing | Flexible | Within 10–21 days of first payment |

| Standalone product | Yes | No, add-on only |

| Premium cost | Base policy cost | Adds 40%–60% to base premium |

The key point is that CFAR does not replace your base policy. It expands it. If your reason for cancelling is already covered by your standard policy, you claim under that provision and receive full reimbursement. You would not use CFAR for a covered event, and doing so would not give you a higher payout anyway.

A few additional points worth knowing:

- CFAR adds roughly 40%–60% to your base premium, which translates to approximately 3% of your total trip cost.

- You cannot claim the same cancelled expense twice. CFAR is secondary to any standard cancellation benefit that applies.

- A strong base policy is the foundation. CFAR is only as useful as the policy it sits on top of.

Pro Tip: Before adding CFAR, check whether your credit card already provides trip cancellation benefits. Some premium cards cover specific cancellation reasons, which reduces the gap CFAR needs to fill.

What are the eligibility requirements and time windows for CFAR?

CFAR has some of the strictest eligibility rules in travel insurance. Understanding them before you book is the difference between having protection and thinking you have it.

The critical requirements are:

- Purchase within 10–21 days of your first trip payment. This is a firm deadline with no exceptions. If you pay a deposit in January and try to add CFAR in March, you will be declined.

- Insure 100% of your non-refundable trip costs. Partial coverage voids your CFAR eligibility entirely. If your trip costs £6,000 in non-refundable expenses, your insured amount must reflect that full figure.

- Cancel at least 48–72 hours before departure. Cancelling the morning of your flight does not qualify. The notice period is non-negotiable.

- Hold a qualifying base policy. CFAR cannot be purchased without an underlying travel insurance plan that meets the insurer’s requirements.

Why do these rules exist? Insurers set them to prevent adverse selection, which is the tendency for people to buy CFAR only when they already know they are likely to cancel. The tight purchase window and full-cost requirement are the industry’s way of keeping the product financially viable.

The most common mistake travellers make is waiting too long to buy. You book a holiday, feel uncertain about it a month later, and then discover CFAR was only available in the first two weeks after your deposit. By that point, there is nothing to be done. The solution is straightforward: add CFAR on the same day you make your first trip payment, or within a day or two at most.

Is cancel for any reason trip insurance worth the extra cost?

CFAR costs roughly 3% of your total trip value, adding 40%–60% to your base insurance premium. On a £5,000 trip, that is approximately £150 in additional premium. Whether that is worth it depends on your specific circumstances.

CFAR makes the most financial sense in these situations:

- Expensive, non-refundable trips. The higher your sunk costs, the more a partial reimbursement matters. A £10,000 safari with 75% CFAR returns £7,500 if you cancel. Without it, you lose everything.

- Trips booked far in advance. The longer the gap between booking and travel, the more time there is for circumstances to change in ways no standard policy covers.

- Travellers with volatile schedules. Work commitments, family situations, or health concerns that do not meet the clinical threshold for a standard cancellation claim are exactly what CFAR addresses.

- Destinations with political or social uncertainty. Fear of travel and changing political circumstances are not covered by standard policies. CFAR is.

- Travellers with pre-existing health concerns. If your condition is managed but unpredictable, CFAR provides a safety net that standard medical cancellation cover may not. You can explore travel insurance for health conditions for context on how these policies interact.

Meghan Walch, a travel insurance expert, describes CFAR as an “insurance policy against anxiety”, protecting against fears or unforeseen situations that fall outside traditional policy definitions. That framing is accurate. CFAR is not primarily about catastrophic events. It is about preserving your financial position when life simply changes.

Pro Tip: Compare CFAR reimbursement percentages across insurers before buying. The difference between a 50% and a 75% plan can be significant on a large trip, and the premium difference is often smaller than you expect.

How to select and purchase the right flexible travel insurance

Choosing the right CFAR plan requires more than picking the cheapest option. The quality of the underlying base policy matters as much as the CFAR percentage itself.

Follow these steps to purchase effectively:

- Book your trip and note the date of your first payment. Your CFAR eligibility clock starts immediately. Do not wait.

- Calculate your total non-refundable costs. Include flights, accommodation, tours, and any other prepaid, non-refundable expenses. Your insured amount must match this figure exactly.

- Compare base policies first. Look for strong standard cancellation, medical evacuation, and baggage cover. CFAR is only as good as the policy beneath it. Unparalleledglobalbenefits provides a useful overview of how travel insurance works to help you assess base policy quality.

- Check the CFAR reimbursement percentage. Aim for 75% or higher where available. Allianz, for example, offers plans reaching 80% reimbursement.

- Read the cancellation notice requirement. Confirm whether your insurer requires 48 or 72 hours’ notice before departure, and set a reminder.

- Purchase the combined policy within your eligibility window. Ideally, do this on the same day as your first trip payment.

- Keep all booking receipts and payment records. You will need these to substantiate your non-refundable costs if you claim.

One point that catches many travellers off guard: CFAR cannot be added after the fact. If you are comparing best trip insurance cancel for any reason options, do so before you commit to a booking, not after. The purchase window is the single most important constraint in the entire product.

Key takeaways

Cancel For Any Reason coverage is the only travel insurance product that reimburses you for cancellations outside standard covered events, making it the most flexible trip cancellation option available.

| Point | Details |

|---|---|

| CFAR is an add-on, not standalone | You must purchase a base travel policy first; CFAR cannot be bought independently. |

| Strict purchase window applies | Buy within 10–21 days of your first trip payment or lose eligibility permanently. |

| Insure 100% of non-refundable costs | Partial coverage voids your CFAR claim, regardless of cancellation timing. |

| Reimbursement is partial | Expect 50%–75% back, with premium plans such as Allianz reaching 80%. |

| Cost adds 40%–60% to base premium | On a £5,000 trip, CFAR adds roughly £150 in extra premium for significant protection. |

Why CFAR is the most underestimated product in travel insurance

I have spent years reviewing international insurance policies for travellers, expats, and families relocating abroad. CFAR consistently surprises people, and not always pleasantly. The surprise is rarely about the product itself. It is about the rules.

Most travellers who enquire about CFAR after booking discover they have already missed the purchase window. They paid a deposit six weeks ago, something has changed, and now they want the flexibility they did not know they needed. That is the fundamental problem. CFAR requires you to anticipate uncertainty at the moment of booking, which is precisely when most people feel most optimistic about their plans.

The second misunderstanding I see regularly is around the 100% insured cost requirement. A traveller insures £3,000 of a £5,000 trip to save on premium, then cancels and expects a payout. The claim is denied. The rule is absolute, and it catches people who try to be clever about reducing their premium.

My honest view is that CFAR is worth the cost for any trip above £3,000 with significant non-refundable components, particularly if you are travelling internationally or booking more than three months in advance. The peace of mind is real, and the financial protection is meaningful. But it only works if you buy it correctly, on time, and for the full amount. Treat it as a day-one purchase decision, not an afterthought.

— Coert

Protect your trip with flexible cover from Unparalleledglobalbenefits

Planning an international trip and wondering whether CFAR is right for you? Unparalleledglobalbenefits specialises in travel and expat insurance solutions that go beyond the basics.

Whether you are travelling for leisure, relocating abroad, or visiting family internationally, Unparalleledglobalbenefits can help you identify plans that include Cancel For Any Reason upgrades alongside strong base coverage. The team works with a range of reputable international insurers to match your specific travel profile with the right level of protection. Explore the international insurance plans available, or review the travel insurance guide to understand your full range of options before you book.

Planning a trip for yourself, a resident, or visiting family? UGB + Ekta can arrange travel insurance for seniors up to 100 years old. Just click here: https://ektatraveling.com/?partner_uid=808 and add the promo code “UGB” to receive an additional 10% discount.

FAQ

What does cancel for any reason travel insurance cover?

CFAR covers trip cancellations for any reason not included in your standard policy, such as anxiety, a change of plans, or travel fears. It reimburses 50%–75% of your non-refundable prepaid costs, with some plans reaching 80%.

How long do i have to add CFAR to my travel policy?

You must purchase CFAR within 10–21 days of your first trip payment. After that window closes, the add-on is no longer available regardless of how far in advance your trip is.

Does CFAR pay out if i cancel the day before departure?

No. Most CFAR policies require you to cancel at least 48–72 hours before your scheduled departure. Same-day or last-minute cancellations do not qualify for reimbursement.

Can i insure only part of my trip costs to save on premium?

No. CFAR requires you to insure 100% of your non-refundable trip costs. Insuring a partial amount voids your eligibility for a CFAR claim entirely.

Is CFAR worth buying for a short or inexpensive trip?

CFAR adds roughly 3% of your trip cost to your premium. For trips under £1,500 with mostly refundable bookings, the cost may outweigh the benefit. It delivers the most value on expensive, non-refundable international trips booked well in advance.

Recommended

- Best trip insurance: cancel for any reason in 2026 – Unparalleled Global Benefits

- Trip protection: your complete 2026 travel guide – Unparalleled Global Benefits

- Travel Insurance Cancel for Any Reason: Secure Your Trip – Unparalleled Global Benefits

- What does trip cancellation insurance cover: a 2026 guide – Unparalleled Global Benefits