TL;DR:

- Choosing the right student health insurance involves comparing coverage details, costs, and visa requirements thoroughly. Students must verify that plans meet federal and institutional standards to avoid costly mistakes and ensure compliance. Starting early, reviewing benefit summaries, and confirming network access are crucial steps to secure effective healthcare coverage abroad.

Comparing student health insurance means evaluating coverage adequacy, compliance with visa or university mandates, and overall cost-effectiveness to protect you financially while studying abroad. The right plan is not simply the cheapest one. It is the one that covers hospitalisation, mental health, prescriptions, and emergency evacuation while meeting the specific requirements of your institution or visa category. Students and families who compare health insurance carefully before enrolment avoid the most common and costly mistakes: inadequate networks, surprise bills, and compliance failures that can block registration or affect visa status.

How to compare student health insurance plans effectively

The starting point for any meaningful student health coverage comparison is understanding that not all plans labelled “student insurance” are equivalent. The US Centers for Medicare and Medicaid Services (CMS) notes that student health plans vary significantly in regulatory treatment, meaning you must compare benefits line by line rather than assuming uniformity across providers.

There are four main categories of student health insurance options worth comparing:

- University-sponsored Student Health Insurance Plans (SHIPs): These are typically ACA-compliant and cover the 10 essential health benefits with no annual dollar limits. However, coverage specifics differ depending on whether the plan is fully insured or self-insured, and provider networks are often limited to campus or local facilities.

- Private international student plans: These are designed specifically for students on visas such as F-1 or J-1. Providers in this category often offer waiver-friendly options with tailored coverage that meets both visa and university requirements, sometimes at a lower cost than university plans.

- Travel insurance: For short-term study abroad programmes lasting under six months, travel insurance can supplement or even replace a health plan. It is not suitable as a standalone solution for full academic years because it typically excludes pre-existing conditions and has lower benefit limits.

- Family health plans: Staying on a parent’s domestic plan is possible in some cases, but geographic network restrictions make this impractical for students studying in a different country or even a different state.

Regulatory context matters here. J-1 visa holders, for example, must carry minimum coverage that meets federal standards under 22 CFR 62.14, which specifies amounts for medical benefits, evacuation, and repatriation. A plan that does not meet these thresholds puts your visa status at risk, regardless of how affordable it appears.

Pro Tip: Check whether your university’s international student office publishes a list of pre-approved waiver plans. This list saves significant research time and confirms which private plans already meet institutional requirements.

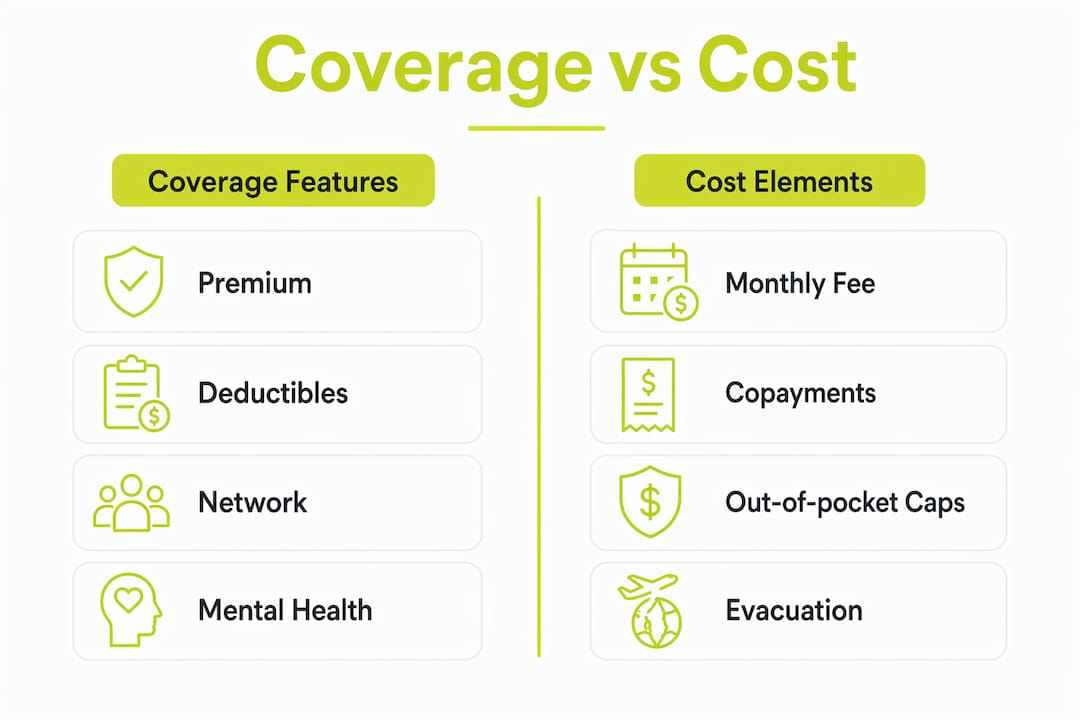

What coverage details and costs should you compare?

Once you know which plan types are relevant to your situation, the next step is a structured cost and coverage comparison. The most common mistake students make is focusing only on the monthly premium. The premium is just one part of what you will actually pay.

Here is a practical framework for comparing student health insurance options side by side:

| Coverage feature | What to check |

|---|---|

| Premium | Monthly or annual cost; confirm whether it covers the full academic year |

| Deductible | Amount you pay before insurance contributes; lower is better for frequent care |

| Maximum out-of-pocket | The ceiling on your annual costs; critical for financial protection |

| Hospitalisation | Inpatient and outpatient cover; check for per-admission limits |

| Mental health | Telehealth sessions, counselling visits, and crisis support included |

| Prescriptions | Formulary tiers and co-pay amounts for common medications |

| Evacuation and repatriation | Minimum $50,000 evacuation and $25,000 repatriation for J-1 compliance |

| Network access | In-network providers near your campus or residence |

Cost-sharing components beyond the premium, including deductibles, copayments, and maximum out-of-pocket caps, are what determine your real financial exposure. A plan with a low premium but a $5,000 deductible may cost you far more than a plan with a slightly higher premium and a $500 deductible if you need care during the year.

Network accessibility is a critical factor that students frequently overlook. Out-of-network providers can generate large, unexpected bills even when you hold valid insurance. Before selecting a plan, confirm that hospitals and clinics near your campus or accommodation are listed as in-network providers.

Mental health coverage has become a standard expectation in student plans. Many plans now include telehealth options covering unlimited virtual mental health sessions, which is particularly valuable for students adjusting to life in a new country.

Pro Tip: Request the Summary of Benefits and Coverage (SBC) document for each plan you are comparing. This standardised document makes it straightforward to compare hospitalisation limits, co-pay structures, and exclusions across different providers without wading through full policy documents.

What factors influence the cost of student health insurance?

The price of affordable student health policies is shaped by several variables, and understanding them helps you assess value rather than simply choosing the lowest number.

- Age: Younger students generally pay lower premiums. In ACA-compliant markets, age is one of the primary rating factors.

- Visa type: International students on J-1 or F-1 visas may have access to specific plan categories that domestic students do not, and vice versa. Visa status can restrict or expand your options.

- Plan type (HMO, EPO, PPO): HMO and EPO plans require you to use a defined network and typically cost less. PPO plans offer more flexibility to see out-of-network providers but carry higher premiums. For students in a fixed location near campus, an HMO or EPO often provides the best value.

- Metal tier: Bronze plans carry the lowest premiums but the highest deductibles. Silver plans balance cost and coverage. Gold and Platinum plans have higher premiums but lower out-of-pocket costs when you use care frequently.

- Location: Healthcare costs vary significantly by city and state. A plan in New York City will generally cost more than an equivalent plan in a smaller university town.

- Coverage level: Higher benefit limits, lower deductibles, and broader networks all increase the premium.

University-sponsored plans cost approximately $2,000 to $5,000 annually, with a median around $2,700 per year. This figure gives you a useful benchmark when comparing private alternatives. A private international student plan that costs $1,200 per year may appear cheaper, but you must verify that its benefit limits and network access are genuinely comparable before concluding it represents better value.

How to meet visa and university insurance requirements

Compliance is not simply about having insurance. It means meeting specific requirements for coverage amounts, benefit types, and documentation. Here is a step-by-step process to confirm your chosen plan qualifies:

- Identify your visa requirements. J-1 visa holders must carry a minimum of $100,000 in medical benefits, $50,000 for medical evacuation, and $25,000 for repatriation of remains, with a deductible no higher than $500 per accident or illness. These are federal minimum standards under 22 CFR 62.14, and no exceptions are made.

- Review your university’s insurance mandate. Most universities require students to be enrolled in the university plan or an approved equivalent. Download the institution’s waiver criteria document, which lists the minimum coverage thresholds your alternative plan must meet.

- Obtain a certificate of coverage. When applying for a waiver, you will need official documentation from your insurer confirming your coverage dates, benefit limits, and policy number. Request this document before the waiver deadline.

- Submit your waiver application on time. Waiver windows are typically open for only a few weeks at the start of each semester. Missing the deadline means you are automatically enrolled in the university plan and charged accordingly.

- Confirm refund policies. Some waiver-friendly plans offer a refund if your waiver application is denied, which reduces your financial risk during the application process.

Non-compliance carries real consequences. A student whose plan does not meet J-1 requirements risks a visa violation. A student who misses the university waiver deadline pays for two plans simultaneously. Starting this process at least six weeks before the semester begins gives you enough time to gather documentation, compare options, and submit paperwork without pressure.

For students concerned about evacuation and repatriation cover, this benefit is not a luxury. It is a legal requirement for certain visa categories and a practical necessity for anyone studying far from home.

Key takeaways

Choosing the right student health insurance abroad requires comparing coverage details, costs, and compliance requirements together, not in isolation.

| Point | Details |

|---|---|

| Compare beyond the premium | Deductibles, out-of-pocket caps, and network access determine your real cost. |

| Know your visa minimums | J-1 holders need at least $100,000 medical, $50,000 evacuation, and $25,000 repatriation cover. |

| Start the waiver process early | Waiver windows close quickly; begin comparing plans at least six weeks before term starts. |

| Match plan type to your location | HMO and EPO plans suit students in a fixed campus location; PPO suits those who travel frequently. |

| Verify network access locally | Confirm that hospitals and clinics near your campus are in-network before committing to a plan. |

What I have learnt from years of watching students choose the wrong plan

Most students who end up underinsured did not make a careless decision. They made a rushed one. They saw a low premium, assumed the plan was adequate, and did not read the Summary of Benefits until they were sitting in an urgent care centre trying to understand why their claim was being denied.

The single most important shift in how you approach this process is treating student insurance as layered coverage. One layer satisfies your legal and institutional obligations. The second layer provides practical, on-the-ground protection for the healthcare system you are actually living in. A plan can pass a university waiver check and still leave you with a $3,000 bill because the nearest in-network hospital is 40 miles from campus.

I also see families underestimate how quickly urgent care costs accumulate. Emergency room visits can cost several thousand dollars for a single visit, while urgent care co-pays typically run $30 to $50. Knowing which facilities your plan covers at the lower rate is not a minor detail. It is a decision that can save you thousands over an academic year.

Start your comparison early. Use the SBC documents. Check the network map for your specific campus postcode. And if you are on a J-1 visa, treat the federal minimums as your floor, not your ceiling.

— Coert

Find the right international student plan with Unparalleledglobalbenefits

Sorting through student health insurance options across multiple providers, visa categories, and university requirements is genuinely complex. Unparalleledglobalbenefits specialises in international student insurance solutions that are designed to meet both visa compliance standards and practical healthcare needs abroad. Whether you need a plan that qualifies for a university waiver, includes evacuation cover, or provides access to a broad provider network near your campus, the team at Unparalleledglobalbenefits can guide you to the right fit. Explore tailored coverage options and get a quote that reflects your actual situation, not a generic student profile.

Planning a trip for yourself, a resident, or visiting family? UGB + Ekta can arrange travel insurance for seniors up to 100 years old. Just click here: https://ektatraveling.com/?partner_uid=808 and add the promo code “UGB” to receive an additional 10% discount.

Watch this short overview to understand how international student health insurance works in practice:

https://youtu.be/bjzvma7Sh1g

FAQ

What is the difference between a SHIP and a private student plan?

A Student Health Insurance Plan (SHIP) is a university-sponsored plan that is typically ACA-compliant and covers the 10 essential health benefits. A private international student plan is purchased independently and may offer lower premiums and waiver-friendly terms, but you must verify it meets your university’s minimum coverage thresholds.

How much does student health insurance cost per year?

University-sponsored plans cost approximately $2,000 to $5,000 annually, with a median around $2,700. Private international student plans can cost significantly less, but benefit limits and network access must be compared carefully before assuming they represent better value.

What coverage does a J-1 visa require?

J-1 visa holders must carry a minimum of $100,000 in medical benefits, $50,000 for medical evacuation, and $25,000 for repatriation of remains, with a deductible no greater than $500 per accident or illness. These are federal requirements under 22 CFR 62.14 and are non-negotiable.

Can I stay on my parents’ health insurance while studying abroad?

You may remain on a parent’s domestic plan in some circumstances, but geographic network restrictions typically make this impractical for students studying in a foreign country or a different state. Out-of-network care abroad is rarely covered at meaningful benefit levels.

What is a health insurance waiver and how do I apply?

A waiver is a formal request to opt out of your university’s mandatory health plan because you already hold qualifying alternative coverage. You submit documentation including a certificate of coverage to your university’s student health office within a defined window, typically at the start of each semester. Some private plans offer refunds if your waiver application is denied, reducing your financial risk during the process.

Recommended

- Expat health insurance: your complete guide for 2026 – Unparalleled Global Benefits

- Multi-country travel insurance: your 2026 guide – Unparalleled Global Benefits

- Complete Guide to International Health Insurance for Students – Unparalleled Global Benefits

- 7 Best International Health Insurance Tips for Students Abroad – Unparalleled Global Benefits