TL;DR:

- Expat insurance commonly excludes pre-existing conditions, war zones, elective procedures, mental health, and disease-specific waiting periods. Understanding these exclusions before purchasing can prevent costly claim denials, especially in conflict zones or for certain health conditions. Fully disclosing health information, reviewing policy details, and working with specialists help expats manage coverage gaps effectively.

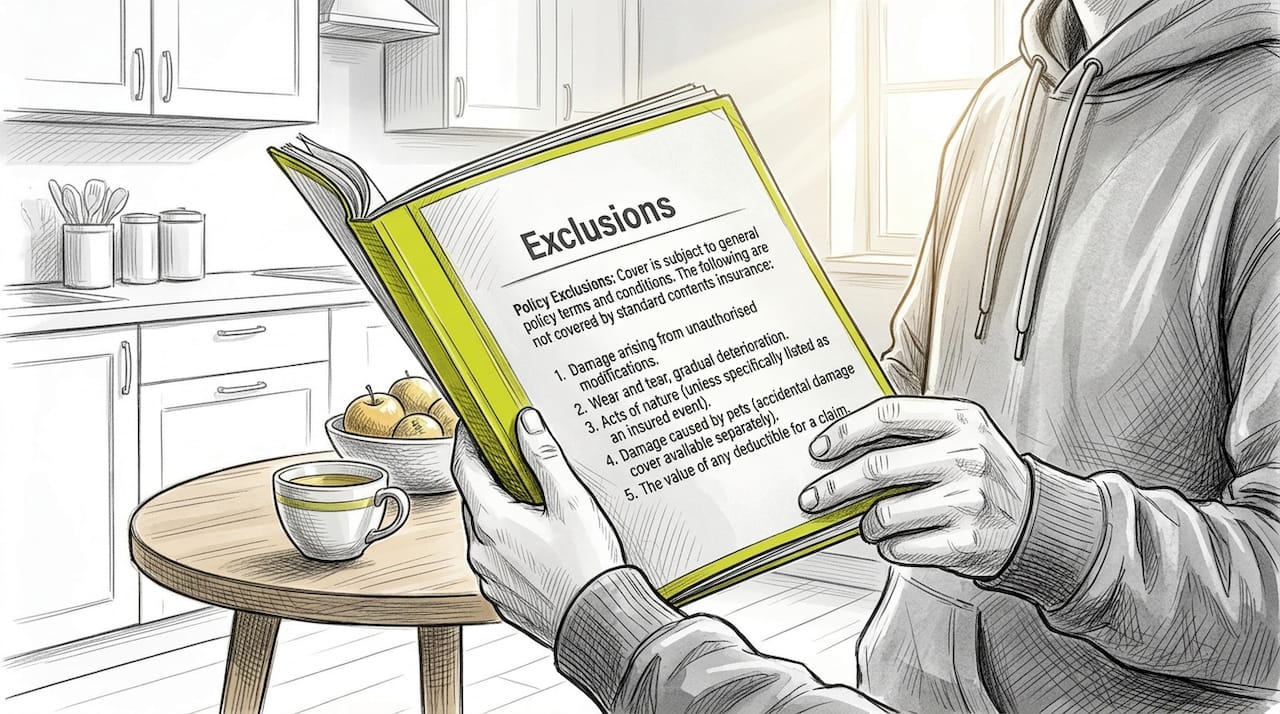

Typical exclusions in expat insurance are the specific conditions, events, and circumstances that international private medical insurance (IPMI) policies routinely refuse to cover, regardless of how comprehensive the plan appears. Knowing these exclusions before you sign is not optional. A claim denial abroad, where you may be far from your support network and facing unfamiliar healthcare systems, can be financially devastating. This article maps the most common exclusion categories across major expat plans, explains how policy language creates hidden gaps, and gives you practical tools to protect yourself before a crisis occurs.

What are the most common exclusions in expat insurance policies?

The most frequent exclusions in expat insurance fall into five clear categories: pre-existing medical conditions, war and armed conflict, chronic and behavioural health conditions, elective and cosmetic treatments, and disease-specific waiting periods. Understanding each one prevents the most common and costly claim surprises.

Pre-existing conditions typically trigger waiting periods of 6 to 24 months or complete exclusion from coverage. This means a condition you were diagnosed with or treated for before your policy start date may not be covered for a significant period, even if you disclosed it honestly on your application.

Cosmetic surgery, fertility treatments, and elective procedures are excluded across virtually all standard IPMI plans. These are treatments chosen for personal preference rather than medical necessity, and insurers draw a firm line between the two. Dental and optical care are also frequently excluded unless you purchase specific add-on modules.

Here is a summary of the most common exclusion categories and how they typically appear across popular expat plans:

| Exclusion category | Typical treatment in policies |

|---|---|

| Pre-existing conditions | Excluded permanently or subject to 6–24 month waiting periods |

| War and armed conflict | Excluded universally; specialist add-ons available at extra cost |

| Cosmetic and elective procedures | Excluded across all standard plans |

| Mental health and behavioural conditions | Limited or excluded; some plans offer optional add-ons |

| Disease-specific conditions (e.g., hernia, cataracts) | Waiting periods of 1–2 years apply regardless of health history |

Pro Tip: Read the exclusions section of your policy document first, not last. Insurers are legally required to list all exclusions clearly, and this section tells you more about a plan’s real value than the marketing summary ever will.

How do war, government advisories, and conflict zones affect cover?

Standard expat policies exclude losses related to war, armed conflict, terrorism, and civil unrest as a universal baseline. This is not a minor footnote. It is a structural feature of the global insurance market, driven by the fact that major insurers rely on reinsurers who standardly exclude war from their own coverage obligations.

The phrase “covered worldwide” is one of the most misunderstood claims in expat insurance marketing. “Covered worldwide” rarely equates to coverage during active hostilities. Policy language requires detailed scrutiny to understand where geographic coverage ends and conflict exclusions begin.

Government travel advisories add another layer of complexity. UK FCDO Level 4 advisories (“Do Not Travel”) generally invalidate expat travel insurance cover for cancellations or disruptions in the affected region. If you remain in or travel to a country under such an advisory, your insurer may treat any resulting claim as a “known event” and refuse it entirely.

The conflicts in Ukraine and across the Middle East have made this issue concrete for thousands of expats. Many discovered that their policies covered routine medical care in those regions but excluded any claim with a direct or indirect link to conflict activity. War exclusion wording is typically broad, covering direct and indirect consequences including airline cancellations, hotel costs, and medical claims linked to conflict zones.

Specialist war risk add-ons do exist and can cover injuries from shelling, missile strikes, drone attacks, and acts of terrorism for civilians not involved in combat. However, these products are costly, limited in scope, and not offered by all providers. If you live or work in a high-risk region, verify whether your insurer offers a passive war risk add-on and read its terms with the same scrutiny you would apply to the base policy.

Key points to verify before travelling to or residing in a conflict-adjacent region:

- Whether your policy contains a “force majeure” clause that voids cover during declared emergencies

- The specific wording of the war exclusion, particularly whether “indirect consequences” are included

- Whether your government has issued a travel advisory for your destination and at what level

- Whether a specialist war risk or kidnap and ransom product is available and appropriate for your situation

What are disease-specific and pre-existing condition waiting periods?

These two waiting period types are frequently confused, and the distinction matters significantly for your claims timeline. A pre-existing condition (PED) waiting period is personal. It applies to conditions you had before your policy started and is triggered by your individual health history. A disease-specific waiting period, by contrast, applies to all policyholders regardless of their personal health history, simply because the condition appears on the insurer’s named list.

Disease-specific waiting periods for conditions like cataracts, hernias, gallstones, and joint replacements typically range from one to two years across most IPMI providers. You could be in perfect health with no prior diagnosis and still face a 12-month wait before a hernia repair is covered.

When both waiting period types apply to the same condition, the longer period governs. This overlap can delay legitimate claims by two years or more, which is a significant gap if you need treatment shortly after relocating abroad.

Common conditions and their typical waiting periods across major plans:

- Cataracts: 12 to 24 months

- Hernia repair: 12 to 24 months

- Gallstone removal: 12 months

- Joint replacement (hip, knee): 24 months

- Tonsillectomy: 12 months

- Varicose vein treatment: 12 months

Some insurers offer a waiting period buy-down option, allowing you to pay an additional premium to reduce or eliminate specific waiting periods. This is worth considering if you have a known condition that falls on the disease-specific list, particularly if you are purchasing cover later in life when premiums already rise steeply with age.

Pro Tip: Purchase your expat insurance before you need it. Waiting periods run from your policy start date, so the earlier you begin cover, the sooner those periods expire. Buying a plan six months before a planned procedure is almost always too late.

What other limitations should expats watch for?

Beyond the headline exclusions, several less obvious limitations catch expats off guard when they submit claims. Outpatient prescriptions are a common example. Routine prescriptions abroad are often paid out-of-pocket because coverage is limited to inpatient treatment or requires an optional outpatient add-on that many policyholders do not purchase.

Mental health coverage is frequently limited or excluded in standard expat insurance policies. Many plans either cap the number of covered sessions, exclude certain diagnoses entirely, or require a specialist referral before any mental health claim is accepted. Given that expatriation itself is a significant life stressor, this is an exclusion worth addressing directly when selecting a plan.

Non-medical travel disruptions represent another category where expats discover gaps. Standard IPMI plans exclude travel cancellations, delays, and baggage loss entirely. These events require a separate travel insurance policy, and the two products are not interchangeable. Many expats assume their health plan covers the full spectrum of travel-related risks, which it does not.

Prior authorisation failures are a less obvious but equally costly exclusion trigger. Most IPMI plans require you to obtain approval from your insurer before undergoing planned procedures. If you proceed without authorisation, the insurer may reduce or refuse the claim, even if the treatment itself would otherwise be covered. Always confirm the prior authorisation requirement in writing before scheduling non-emergency treatment.

Additional limitations worth reviewing in any policy:

- Exclusions for self-inflicted injuries or conditions arising from alcohol or substance use

- Restrictions on scheduling medical appointments at non-network facilities

- Caps on physiotherapy, specialist consultations, or diagnostic imaging per year

- Exclusions for treatment in your home country if the policy is structured as “away from home country” cover

How can expats manage and negotiate around policy exclusions?

Managing exclusions in expat insurance starts with honest and complete disclosure on your application. Failing to declare a pre-existing condition does not make it disappear. It creates grounds for the insurer to void your policy entirely if the omission is discovered, even for unrelated claims. Full disclosure is the foundation of a valid policy.

Follow these steps to reduce the impact of typical exclusions on your coverage:

- Read the policy exclusions section before purchasing. Compare the exclusions list across at least three plans using a resource like the best plans comparison to identify which plan has the fewest gaps for your specific health profile.

- Ask about optional riders. Many insurers offer add-ons for mental health, outpatient prescriptions, dental, optical, and in some cases chronic condition management. These riders cost more but close significant gaps.

- Consider layering products. Pair your IPMI plan with a separate travel insurance policy to cover trip cancellations, baggage loss, and travel disruptions. The two products are designed to complement each other, not duplicate coverage.

- Verify geographic coverage explicitly. If you live in or travel to regions with elevated geopolitical risk, confirm in writing whether your policy covers medical treatment there and whether any conflict-related exclusions apply.

- Work with a specialist broker. An adviser who focuses on international health insurance for expats can identify exclusions that a general broker might overlook and negotiate terms on your behalf.

Pro Tip: Ask your insurer or broker to provide a written summary of all exclusions that apply to your specific application, not just the standard policy wording. This personalised exclusion schedule is the document you need to review before every claim.

Key takeaways

Understanding typical exclusions in expat insurance is the single most important step you can take to avoid unexpected claim denials and financial exposure abroad.

| Point | Details |

|---|---|

| Pre-existing conditions | Expect waiting periods of 6–24 months or full exclusion; always disclose fully. |

| War and conflict exclusions | “Covered worldwide” does not mean covered in active conflict zones; verify explicitly. |

| Disease-specific waiting periods | Apply to all policyholders for named conditions; the longer period governs when both apply. |

| Mental health and prescriptions | Frequently limited or excluded; add-on modules are available but must be purchased separately. |

| Prior authorisation | Skipping this step can void an otherwise valid claim; always confirm in writing first. |

The exclusions conversation nobody wants to have

After years of working with expats across multiple continents, I have noticed a consistent pattern. People spend considerable time comparing premium prices and hospital networks, and almost no time reading the exclusions section. That is the wrong order of priorities.

The exclusions list is where the real policy lives. A plan with a lower premium and a longer exclusions list is almost always worse value than a slightly more expensive plan with fewer restrictions, particularly once you factor in the cost of a single denied claim. I have seen expats face five-figure medical bills because they assumed a condition was covered when it was explicitly excluded in plain language on page twelve of their policy document.

The geopolitical dimension has become more pressing in recent years. Conflicts in Ukraine and the Middle East have exposed how broadly war exclusion clauses are written and how quickly “covered worldwide” policies can become worthless in practice. If your role or lifestyle takes you near regions of instability, specialist war risk products are not a luxury. They are a necessity.

My honest recommendation is this: treat the exclusions conversation with your broker as the most important part of the purchasing process. Ask direct questions. Get written answers. And if a broker cannot explain every exclusion on your policy in plain language, find one who can.

— Coert

How Unparalleledglobalbenefits helps you find cover that fits

Choosing expat insurance without fully understanding its exclusions is a risk you do not need to take. Unparalleledglobalbenefits specialises in international insurance solutions for expatriates, travellers, and families living abroad, with a focus on matching clients to plans that address their specific health profiles and geographic circumstances.

Whether you need clarity on pre-existing condition terms, war risk coverage, or the right combination of health and travel products, the team at Unparalleledglobalbenefits can guide you through the options. Explore the full range of expat health insurance plans or request a personalised quote to find cover that works for your situation, not against it.

Planning a trip for yourself, a resident, or visiting family? UGB + Ekta can arrange travel insurance for seniors up to 100 years old. Just click here: https://ektatraveling.com/?partner_uid=808 and add the promo code “UGB” to receive an additional 10% discount.

For a helpful overview of what expat insurance covers and where the gaps typically appear, watch this short video:

https://youtu.be/bjzvma7Sh1g

FAQ

What are the most common exclusions in expat insurance?

The most common exclusions in expat insurance are pre-existing medical conditions, war and armed conflict, cosmetic and elective procedures, mental health limitations, and disease-specific waiting periods for conditions such as cataracts, hernias, and gallstones.

Does “covered worldwide” mean I am covered in conflict zones?

No. “Covered worldwide” is a marketing term that does not override war and armed conflict exclusions. Active conflict zones are almost universally excluded from standard IPMI plans, and specialist war risk add-ons are required for meaningful coverage in those areas.

How long are typical waiting periods for pre-existing conditions?

Pre-existing condition waiting periods typically range from 6 to 24 months depending on the insurer and the condition. Some conditions may be permanently excluded, particularly if they are chronic or require ongoing treatment.

Are mental health conditions covered by expat insurance?

Mental health coverage is frequently limited or excluded in standard expat insurance policies. Many plans cap the number of covered sessions or require optional add-ons to access any mental health benefits at all.

What is the difference between a disease-specific and a pre-existing condition waiting period?

A disease-specific waiting period applies to all policyholders for named conditions regardless of personal health history, while a pre-existing condition waiting period applies only to individuals with a prior diagnosis. When both apply to the same condition, the longer waiting period governs the claim timeline.

Recommended

- What expat insurance doesn’t cover: key exclusions explained – Unparalleled Global Benefits

- Essential expat insurance tips: Protect your health abroad – Unparalleled Global Benefits

- Why expats need travel insurance: Essential protection – Unparalleled Global Benefits

- Expat insurance vs local insurance: Which cover suits you? – Unparalleled Global Benefits