TL;DR:

- Understanding expat insurance terms, such as premiums, deductibles, and exclusions, is essential for making confident coverage decisions abroad.

- Differentiating between international and long-term expat plans helps ensure you select the appropriate coverage, especially regarding portability and routine care.

Moving abroad is exciting, but reading your first expat insurance policy can feel like learning a new language. Terms like “coinsurance”, “IPMI”, and “waiting period” appear without explanation, and a misunderstanding can leave you with a coverage gap at the worst possible time. This guide has expatriate insurance terminology explained in plain language, so you can make confident decisions about your health cover wherever you live. Whether you are relocating for work, retiring overseas, or simply building a life in a new country, understanding the words in your policy is the first step to genuine protection.

Table of Contents

- Key takeaways

- Core expat insurance terms you need to know

- International vs expat insurance: what the terms really mean

- Policy scope, exclusions, and the terms that limit your cover

- Cost-related terms and the trade-offs they represent

- My perspective on mastering expat insurance language

- How Unparalleledglobalbenefits can help you find the right cover

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Know your core terms | Understanding premium, deductible, and coinsurance helps you predict your real costs before a claim arises. |

| Expat vs international cover | Long-term expat plans and short-term international plans differ significantly in scope, routine care, and portability. |

| Exclusions matter greatly | Pre-existing conditions and waiting periods directly affect what your policy will and will not pay for. |

| Deductible choice is strategic | Raising your deductible reduces monthly premiums but increases the amount you pay when you actually need care. |

| Ask questions before signing | Clarifying unfamiliar terms with your insurer upfront prevents costly surprises when you submit a claim. |

Core expat insurance terms you need to know

Getting to grips with expat insurance terms starts with the basics. These are the words that appear on almost every policy document and directly affect how much you pay and how much you receive.

-

Premium. This is the amount you pay to keep your policy active, typically monthly or annually. Premiums are influenced by your age, the coverage limit you choose, and where in the world you live. A 35-year-old living in Southeast Asia will generally pay far less than a 55-year-old who includes the United States in their coverage area.

-

Deductible (also called excess). This is the amount you pay out of your own pocket before your insurer starts covering costs. If your policy has a £1,000 deductible and your hospital bill is £3,500, you pay £1,000 and your insurer covers the remaining £2,500.

-

Copayment. A fixed fee you pay for a specific service, such as £30 for a GP visit, regardless of the total cost of that visit.

-

Coinsurance. After you have met your deductible, coinsurance is the percentage of remaining costs you share with your insurer. An 80/20 split means your insurer pays 80% and you pay 20% until you reach your out-of-pocket maximum.

-

Out-of-pocket maximum. The most you will pay in a given policy year. Once you reach this figure, your insurer covers 100% of eligible costs for the remainder of the year. This term is critical to understand because it defines your financial ceiling in a serious medical situation.

-

Coverage limit. The maximum amount your insurer will pay, either per claim, per year, or over the lifetime of your policy. Basic expat plans start around $50 per month, while comprehensive options with higher limits reach $400 per month.

Pro Tip: Always check whether your coverage limit is annual or lifetime. A plan with a £1 million lifetime cap sounds generous, but a single serious illness can exhaust it far faster than you expect.

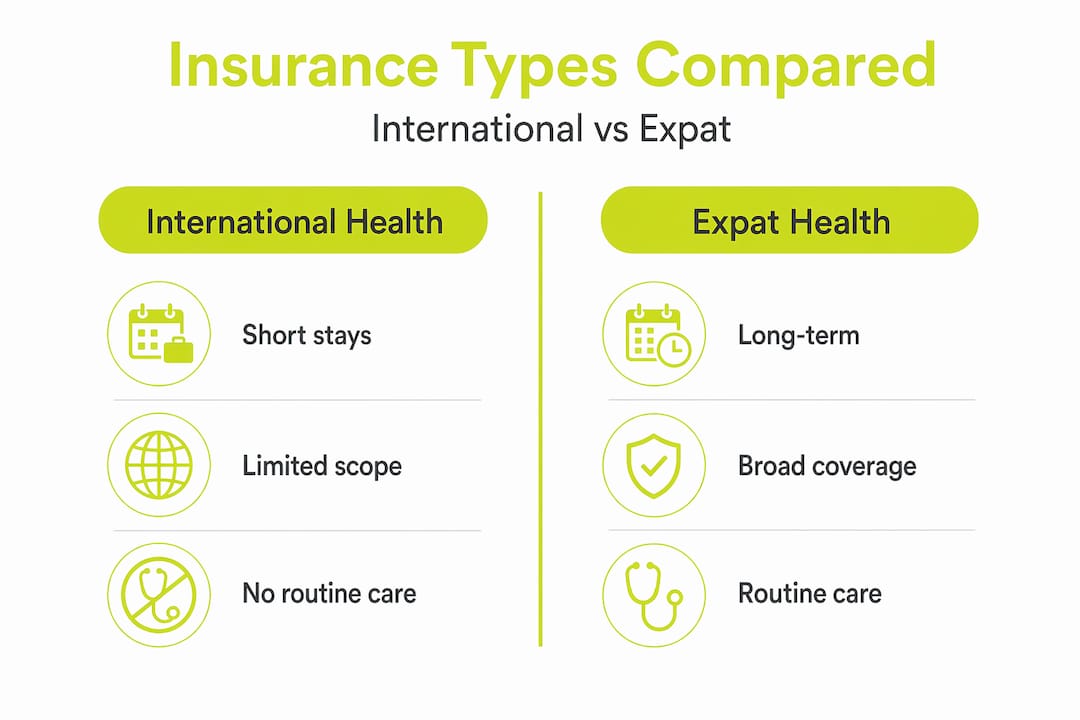

International vs expat insurance: what the terms really mean

Many people use “international health insurance” and “expat health insurance” interchangeably. They are not the same thing, and confusing them is one of the most common mistakes people make when selecting cover abroad.

International health insurance covers short to medium-term stays, typically between 30 and 365 days. It suits people on extended business trips, gap years, or medium-length assignments. Expat health insurance, by contrast, is designed for long-term residence of one year or more and commonly includes routine care, maternity benefits, and cover for chronic conditions.

The distinction also shows up in portability, which refers to whether your policy travels with you across borders. IPMI (International Private Medical Insurance) offers portability across countries, unlike local insurance plans that only cover you within one specific country’s health system. For expats who move between postings or travel frequently, IPMI portability is not a luxury. It is a practical necessity.

The table below summarises the key terminology differences between the two plan types.

| Feature | International health insurance | Expat health insurance |

|---|---|---|

| Typical duration | 30 to 365 days | 1 year or longer |

| Routine care | Usually excluded | Usually included |

| Maternity cover | Rarely included | Often available as add-on |

| Chronic condition cover | Limited or excluded | Commonly included |

| Portability | Limited | Broad, cross-border |

| Visa compliance | Sometimes | Often, with minimum coverage met |

Travel insurance is worth mentioning here too, because it is frequently misunderstood. Travel insurance caps coverage at 30 to 90 days and excludes routine care entirely, making it wholly unsuitable for long-term expatriates. If you are abroad for six months or more and relying on travel insurance, you are carrying a significant coverage gap without realising it.

Pro Tip: If your visa requires health insurance, check whether the plan meets the minimum coverage threshold. Visa programmes commonly require minimum coverage of €30,000 to €50,000, and a standard travel policy will not meet this requirement.

Policy scope, exclusions, and the terms that limit your cover

Understanding what your policy covers is only half the story. The other half is knowing what it does not cover, and why. This is where expatriate policy terminology gets genuinely technical, and where careful reading pays off.

Here are the terms most likely to affect your claim eligibility:

-

Pre-existing condition. Any illness, injury, or medical condition that existed before your policy start date. Most expat plans either exclude pre-existing conditions entirely or impose waiting periods of 6 to 24 months before covering them. If you have a managed condition like diabetes or high blood pressure, this term is central to your plan selection.

-

Waiting period. A set duration after your policy starts during which certain benefits are not yet available. Maternity cover, for example, commonly carries a 10 to 12 month waiting period. Dental and optical benefits often have shorter waiting periods of 3 to 6 months.

-

Rider or add-on. An optional benefit you can attach to your base policy for an additional premium. Common riders include maternity cover, dental cover, optical care, and mental health support. Understanding which riders are available lets you build a plan that matches your actual needs rather than paying for a standard package that does not fit.

-

Exclusion clause. A specific provision within the policy that removes certain conditions or treatments from coverage entirely. Cosmetic procedures, self-inflicted injuries, and experimental treatments are typical examples.

-

Territorial limit. The geographic area within which your policy provides cover. Some plans exclude the United States due to its higher healthcare costs. Others offer worldwide cover but at a significantly higher premium.

Reading the fine print on these terms before you sign is not optional. Ask your insurer directly: “Does this policy cover my pre-existing conditions, and if so, after what waiting period?” A clear answer in writing before your policy starts is far better than a dispute during a claim.

Cost-related terms and the trade-offs they represent

One of the most useful things you can do as an expat is to understand how the financial terms in your policy interact with each other. Choosing the right combination of deductible, premium, and coverage limit is a genuine strategic decision, not just a number-picking exercise.

Here is how to think through the main trade-offs:

-

Higher deductible, lower premium. Raising your deductible from $0 to $5,000 can reduce your annual premium by $1,800 to $2,400. This is a meaningful saving if you are generally healthy and unlikely to make frequent claims. However, it also means you absorb the first $5,000 of any medical bill yourself. This approach works well for expats with solid emergency savings who want catastrophic protection without paying for minor claims.

-

Coverage area and premium variation. Including the United States in your coverage area raises your premium substantially, sometimes by 30% to 50%, because US healthcare costs are among the highest in the world. If you do not plan to receive treatment in the US, excluding it from your territorial limit can produce significant savings without affecting the quality of your everyday cover.

-

Annual versus lifetime limits. A plan with a high annual limit but a low lifetime cap may serve you well for years and then leave you exposed after a serious illness. Understanding this distinction helps you avoid being underinsured when you need cover most.

-

Coinsurance and out-of-pocket maximum interaction. The interplay between premiums, deductibles, and coverage limits determines your real financial exposure. A policy with a low premium, 20% coinsurance, and no out-of-pocket maximum could cost you far more than a higher-premium plan with a defined ceiling during a serious health event.

Pro Tip: When comparing plans, calculate your worst-case annual cost: add your premium to your deductible plus your maximum coinsurance liability. That figure tells you the most you will ever pay in a bad year and gives you a far more honest comparison than premium alone.

My perspective on mastering expat insurance language

I have worked with expats across dozens of countries, and I have seen the same pattern repeat itself. People spend weeks researching neighbourhoods, schools, and cost of living, and then sign an insurance policy in 10 minutes without understanding a single key term. The result is almost always a frustrating claim dispute or an unexpected bill.

In my experience, the expats who navigate insurance most confidently are not the ones with the most medical knowledge. They are the ones who took the time to understand exactly what their policy says before they needed it. Knowing what a waiting period means, or why coinsurance matters above the deductible, removes the anxiety from healthcare decisions abroad entirely.

What I have also learnt is that terminology evolves. Insurers update their policy language, add new exclusions, or restructure their rider options each renewal cycle. Reading your renewal documents each year with the same attention you gave your original policy is a habit worth building.

My strongest advice is this: do not accept vague answers from insurers. Ask specific questions. “Does this policy cover outpatient mental health appointments in my country of residence?” is a better question than “Is mental health covered?” The specificity of your question determines the usefulness of the answer you receive.

— Coert

How Unparalleledglobalbenefits can help you find the right cover

Getting to grips with expat health insurance terminology is the foundation, but finding the right plan requires comparing real options against your specific circumstances. Unparalleledglobalbenefits offers detailed guides, expert comparisons, and personalised support to help expats at every stage of the process. Whether you are searching for your first international plan or reviewing your cover at renewal, the team at Unparalleledglobalbenefits can walk you through the terminology, the trade-offs, and the types of expat insurance available to you in 2026.

Watch this short video guide to see how expat health insurance works in practice:

https://youtu.be/bjzvma7Sh1g

Planning a trip for yourself, a resident, or visiting family? UGB + Ekta can arrange travel insurance for seniors up to 100 years old. Just click here: https://ektatraveling.com/?partner_uid=808 and add the promo code “UGB” to receive an additional 10% discount.

FAQ

What does deductible mean in expat insurance?

A deductible is the amount you pay out of pocket before your insurer begins covering costs. Higher deductibles reduce your monthly premium but increase your financial exposure when you make a claim.

What is the difference between expat and travel insurance?

Expat insurance covers long-term international residence, including routine and chronic care, while travel insurance is capped at 30 to 90 days and excludes routine treatment entirely.

What is a pre-existing condition in expat insurance terms?

A pre-existing condition is any health issue that existed before your policy start date. Most expat plans exclude these or apply waiting periods of 6 to 24 months before providing cover.

What does portability mean in expat coverage definitions?

Portability means your insurance cover remains active as you move between countries. IPMI plans typically offer this feature, whereas local health insurance policies do not extend beyond one country’s borders.

How much does expat health insurance typically cost?

Basic expat health plans start at around $50 per month, with comprehensive plans reaching $400 per month depending on age, location, and the coverage level you select.

Recommended

- Understand common expat insurance terms for clarity abroad – Unparalleled Global Benefits

- What expat insurance doesn’t cover: key exclusions explained – Unparalleled Global Benefits

- Types of expatriate insurance: smart cover choices abroad – Unparalleled Global Benefits

- Understanding Travel Insurance for Expats: A Clear Guide – Unparalleled Global Benefits