TL;DR:

- Medical evacuation costs average $50,000 and can reach up to $250,000 for complex international cases, often wiping out travelers’ savings without adequate insurance. Travel insurance typically covers medical emergencies, evacuation, repatriation, and trip cancellation, but gaps in coverage can lead to significant out-of-pocket expenses abroad. Choosing a tailored policy with sufficient medical, evacuation, and activity coverage is essential to prevent financial catastrophe during international travel.

Imagine being rushed to hospital in a foreign country, unable to speak the local language, and then receiving a bill that wipes out your savings. It happens more often than people expect. Medical evacuation costs average $50,000, with complex international cases exceeding $100,000 to $250,000. Many travellers assume their domestic health plan or credit card cover will step in. In reality, those policies frequently leave significant gaps when you are abroad. This article will show you exactly what travel insurance covers, how much you stand to lose without it, and how to choose the right policy for your specific trip.

Table of Contents

- What travel insurance really covers abroad

- The financial impact: claims, payouts and real costs

- Common exclusions and pitfalls to avoid

- Choosing the right policy: tailor your cover to your trip

- Why the cheapest travel insurance often lets you down

- Next steps: finding trusted travel insurance for your trip

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Medical emergencies are costly | Overseas medical care and evacuation can easily cost tens or hundreds of thousands of pounds. |

| Read exclusions carefully | Pre-existing conditions and risky activities often require specialist or upgraded insurance policies. |

| Tailor your policy | Choosing cover based on your travel, health and activities ensures proper protection abroad. |

| Claim denials are common | Up to a third of travel insurance claims fail due to undisclosed medical issues or improper documentation. |

What travel insurance really covers abroad

Most people think of travel insurance as something that reimburses a lost suitcase or a cancelled flight. That is only a small part of the picture. According to the CDC’s guidance on health care abroad, travel insurance primarily covers medical emergencies, evacuation, and repatriation, since domestic health plans often do not cover international care at all.

When you fall ill or are injured overseas, the costs mount in ways that are genuinely difficult to anticipate. First, foreign hospitals may demand upfront payment before treating you. Second, even if your domestic insurer technically reimburses some costs, the process can take months and may only partially cover expenses. Good travel insurance, by contrast, pays the foreign hospital directly and manages the logistics of your care. Understanding basic travel insurance coverage is the first step to knowing whether your existing cover is truly adequate.

Here is a clear breakdown of what is typically included and what is typically excluded:

| Benefit | Typically covered | Typically excluded |

|---|---|---|

| Emergency medical treatment | Yes | Cosmetic procedures |

| Medical evacuation | Yes | Non-emergency transport |

| Repatriation of remains | Yes | Elective travel home |

| Trip cancellation | Yes | Disinclination to travel |

| Lost or delayed baggage | Yes | Unattended belongings |

| Emergency dental | Yes (acute pain only) | Routine dental work |

| Pre-existing conditions | With declaration and waiver | If undisclosed |

| Extreme sports injuries | With specialist add-on | Under standard policies |

One of the most valuable benefits to understand is how insurers assist with coordinating international care, including liaising with hospitals, arranging specialist transfers, and ensuring you receive appropriate treatment in an unfamiliar system.

“Medical evacuation alone averages $50,000 per incident, with complex international cases reaching $100,000 to $250,000. Without insurance, those costs fall entirely on you.”

Key protections a solid travel policy should include:

- Emergency medical and hospitalisation cover for illness or injury while abroad

- Medical evacuation and repatriation, including transport home if required

- Trip cancellation and interruption reimbursement for pre-paid, non-refundable costs

- Baggage and personal belongings protection against loss, theft, or damage

- 24/7 emergency assistance from a dedicated helpline, wherever you are in the world

- Personal liability cover should you accidentally cause injury or property damage

Understanding what is and is not included before you travel is far more empowering than discovering the gaps after something goes wrong.

The financial impact: claims, payouts and real costs

Numbers tell the most honest story here. Medical claims statistics show that medical incidents make up 40 to 42 per cent of all travel insurance claims, with average payouts ranging from $3,500 to $5,200. For senior travellers or those visiting the United States, the average rises to $7,000 or more per claim. These are not rare, catastrophic events. They are ordinary health emergencies, broken bones, cardiac episodes, serious infections, that happen to people every day while travelling.

Consider how this compares to the cost of a policy. A standard single-trip travel insurance policy for a two-week European holiday might cost between £30 and £80, depending on your age and the level of cover. A basic emergency hospitalisation in Western Europe can cost thousands of pounds, and in the United States, even a short stay in hospital can run to tens of thousands of dollars. The maths is simple and sobering.

| Scenario | Estimated cost without insurance | Typical policy cost |

|---|---|---|

| Emergency hospitalisation in Europe | £3,000 to £10,000 | £30 to £80 |

| Medical evacuation from Southeast Asia | $40,000 to $80,000 | £50 to £150 |

| Emergency treatment in the United States | $15,000 to $150,000+ | £70 to £200 |

| Trip cancellation (pre-paid holiday) | £1,500 to £5,000 | £30 to £100 |

| Senior traveller medical claim | $7,000+ | £80 to £250 |

For medical insurance for seniors, the stakes are particularly high. Older travellers tend to have longer hospital stays, require more complex interventions, and face higher baseline costs in most countries. There are also practical budget tips for seniors that can help make robust cover affordable without sacrificing the protection that matters most.

Without insurance, expenses that are almost never recoverable without a policy include:

- Emergency surgery and specialist consultations

- Intensive care unit stays

- Air ambulance transport and medical repatriation flights

- Nursing care during recovery abroad

- Interpreter services in foreign hospitals

- Replacement medication when prescriptions are lost or stolen

- Emergency dental treatment following an accident

The gap between what people expect to pay and what they actually face is often what causes the greatest financial shock. Travel insurance is the most effective buffer between an unfortunate incident and a financial catastrophe.

Common exclusions and pitfalls to avoid

Knowing what your policy covers is half the battle. Understanding what it does not cover, and why, is equally important. Pre-existing conditions are one of the most frequent sources of claim denials. Insurers define “pre-existing” broadly, sometimes including any condition for which you have visited a doctor in the past 12 to 24 months. If you do not declare a condition and it contributes to a claim, the insurer may refuse to pay entirely.

Adventure and extreme sports present another major pitfall. Standard policies exclude activities such as off-piste skiing, scuba diving beyond 30 metres, white-water rafting, and bungee jumping. If you plan to take part in any high-risk activity, you must seek a specialist add-on or a dedicated adventure sports policy. Never assume that because your activity feels mainstream to you, it will be viewed the same way by an underwriter.

“Up to one in three travel insurance claims is denied due to undisclosed pre-existing conditions, poor documentation, or activities that fall outside the policy terms.”

Government travel advisories matter enormously here. Travelling against official advice from the FCDO (Foreign, Commonwealth and Development Office) or the US State Department will invalidate most policies outright. If there is a warning in place for your destination and you travel regardless, you may find your entire policy void. Always check the latest advice before booking and before you depart.

Common mistakes that lead to claim denials include:

- Failing to declare a pre-existing medical condition at the time of purchase

- Not seeking pre-authorisation from the insurer before major treatment abroad

- Travelling to a destination covered by an active government travel warning

- Participating in activities specifically listed as excluded in the policy

- Losing receipts, medical reports, or police reports needed to support a claim

- Allowing the policy to lapse before the trip ends or before you return home

- Failing to report a theft or loss to local police within the required timeframe

Taking out insurance for pre-existing conditions through a specialist provider dramatically reduces the risk of a denial. And reviewing essential insurance tips before finalising any policy ensures you are not caught out by details buried in the fine print.

Pro Tip: Before you book any trip, check both the FCDO and your destination country’s own government travel advisories. Even a partial travel warning can affect your cover, and policies vary in how they interpret advisory levels.

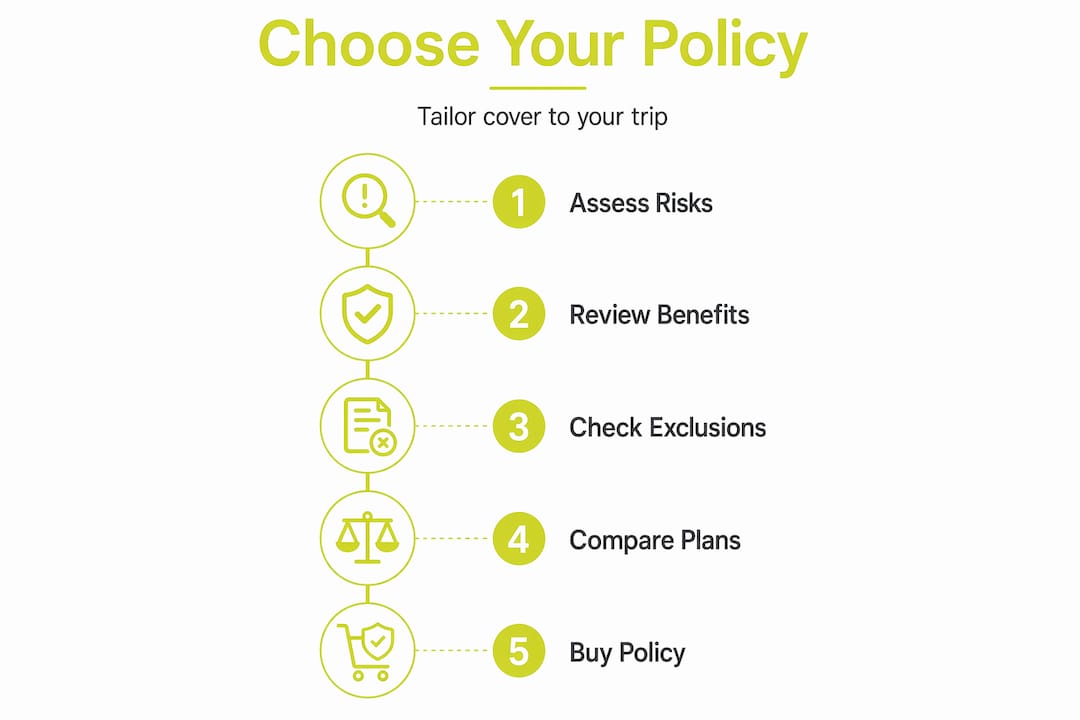

Choosing the right policy: tailor your cover to your trip

No two trips are alike, and your insurance policy should reflect that. A weekend city break to Paris carries very different risks from a three-month backpacking journey through Central America or a diving expedition in the Maldives. The key to choosing the right policy is matching the level and type of cover to your actual risk profile.

For high-risk trips, including remote destinations, cruises, senior travellers, and pregnant women, you should prioritise evacuation limits of at least $100,000, along with specialist providers who understand the complexities of those scenarios. A policy with a $10,000 evacuation limit sounds reasonable until you realise that a helicopter transfer alone can cost that much.

Credit card insurance is often secondary cover, meaning it only pays after your primary insurance has been exhausted. It frequently lacks robust medical or evacuation benefits and may exclude pre-existing conditions and adventure activities entirely. Relying on it as your main protection is a significant risk.

When reviewing policies, consider these key criteria:

- Medical and hospitalisation limit: Look for a minimum of £500,000 for Europe and £1 million or more for trips to the United States

- Evacuation and repatriation limit: A minimum of $100,000 is advisable; higher for remote or high-risk destinations

- Pre-existing condition cover: Ensure you declare all conditions and confirm that the insurer accepts them

- Activity cover: Check that all planned activities are included, and add riders or upgrade to an adventure policy if needed

- Trip cancellation limit: Should reflect the full value of your pre-paid, non-refundable trip costs

- 24/7 emergency helpline: Essential for real-time support in any language, at any hour

- Policy excess: Understand what you will pay out-of-pocket before the insurer contributes

For those travelling on a single trip, reviewing single trip cover options gives you a clear starting point. For older travellers, senior travel insurance with appropriate medical limits deserves particular attention.

Pro Tip: Prioritise your evacuation and medical benefit over lost-luggage cover. You can replace a suitcase; you cannot replace your health, and the costs of medical care abroad are almost always far higher than the value of any belongings.

Why the cheapest travel insurance often lets you down

We understand why price is a significant factor when choosing cover. Travel itself is expensive, and it is tempting to select the lowest-cost policy to reduce upfront spending. But in our experience working with international travellers, low-cost policies are the ones most likely to fail at the moment you need them most.

Cheap policies often come with restrictive definitions, low benefit limits, and lengthy exclusion lists. A policy that costs £15 may only cover £5,000 in medical expenses. In many countries, that will not cover a single night in intensive care. The saving at the time of purchase can pale against the out-of-pocket cost when a claim is refused or only partially paid.

There is also the question of service quality. When you are unwell abroad, you need a team that can make decisions quickly, liaise with foreign hospitals, and organise your care efficiently. Budget insurers often outsource their assistance services, resulting in delays, miscommunication, and frustration at a time when you are already under significant stress.

The role of travel insurance in high-cost emergencies goes well beyond reimbursement. Good insurers coordinate care and pay providers directly, removing the burden from you and your family entirely. That level of support is rarely available from the cheapest options on the market.

A health insurance guide for seniors illustrates this well. Older travellers who opt for budget cover frequently find that their policy’s age limits, pre-existing condition clauses, or low evacuation caps render the policy nearly worthless for the scenarios they are most likely to face. Investing in a policy that genuinely covers your needs is not an extra expense. It is the entire point of having insurance.

Next steps: finding trusted travel insurance for your trip

You now have a clear picture of what travel insurance does, what it costs when you go without it, and how to avoid the most common mistakes. The next step is finding a policy that genuinely fits your situation.

At Unparalleled Global Benefits, we specialise in international insurance solutions designed for travellers, expats, students, and families living or working abroad. Our plans are tailored to your specific needs, whether you are looking for a single-trip policy or long-term international health cover. Understanding how travel insurance protects you in practice is a valuable first step, and our guide to secure cover abroad walks you through the key decisions in straightforward terms. Speak with our team today to explore your options and travel with the confidence that comes from knowing you are genuinely protected.

Frequently asked questions

Does my domestic health insurance cover me abroad?

Most domestic health plans do not provide cover for medical emergencies while travelling internationally, so separate travel insurance is usually required. The CDC confirms that international medical cover is a distinct need that domestic plans rarely address.

Are pre-existing health conditions covered by travel insurance?

Pre-existing conditions are generally excluded unless disclosed and accepted with a waiver, and definitions can be strict, sometimes covering any recent doctor visits. Strict definitions apply, so always declare your full medical history at the point of purchase.

What happens if I take part in extreme sports or adventure activities?

Standard policies typically exclude high-risk activities such as off-piste skiing or deep-water scuba diving, and specialist add-ons or dedicated adventure policies are required for proper cover.

Why might my travel insurance claim be denied?

Claim denials are frequently caused by undeclared pre-existing conditions, missing documentation, or participation in activities not listed in the policy. Up to one in three claims is refused for these reasons, making thorough disclosure and careful record-keeping essential.

Is credit card insurance enough for international travel?

Credit card insurance is often secondary cover and may lack robust medical and evacuation protection, particularly for adventure travel or pre-existing conditions. A dedicated travel policy is strongly advisable for any meaningful international trip.