TL;DR:

- Travel insurance primarily covers emergencies and trip disruptions, but it does not provide comprehensive medical care abroad. Worldwide health coverage is designed for long-term residents or students, offering full-spectrum medical support across multiple countries, including preventive, outpatient, and chronic care. Choosing the right policy depends on your specific needs, duration abroad, and whether you require ongoing healthcare support beyond emergency services.

Many people living or studying abroad assume that a standard travel insurance policy will keep them fully protected. It is an understandable assumption, but it is also one that can lead to serious financial and medical risk. Travel insurance is not the same as worldwide health coverage. Travel insurance typically handles emergencies and trip disruptions, whilst worldwide health coverage supports your complete medical needs over months or even years abroad. If you are an expatriate on a long assignment or an international student settling into life overseas, understanding this distinction is not optional. It is essential.

Table of Contents

- Understanding worldwide health coverage

- Key differences: Worldwide health coverage versus travel insurance

- Who needs worldwide health coverage?

- What to look for in a worldwide health policy

- Our perspective: What most guides overlook about worldwide health cover

- Find the right worldwide health cover to protect your global lifestyle

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Global protection required | Living, working, or studying abroad needs more than just travel insurance for true peace of mind. |

| Travel versus health cover | Travel insurance covers emergencies; worldwide health plans support long-term medical and wellness needs. |

| Policy features matter | Always check for portability, renewability, exclusions, and local compliance with worldwide health coverage. |

| Visa rules can dictate cover | Students and workers may need specific types of cover to comply with destination country regulations. |

| Expert guidance saves | Consulting specialists helps avoid common pitfalls and ensures your coverage matches real-world needs. |

Understanding worldwide health coverage

Worldwide health coverage is a type of health insurance specifically designed for people who live, work, or study outside their home country for an extended period. Unlike domestic health plans, which tie you to a local healthcare network, or travel insurance, which focuses primarily on short-term emergencies and trip-related incidents, worldwide health coverage looks after your full spectrum of medical needs across multiple countries.

Think of it this way. If you fracture your wrist during a weekend trip and need an emergency consultation, travel insurance will likely step in. But if you need ongoing physiotherapy, follow-up appointments, or specialist care over several months, travel insurance simply was not built for that. As the US State Department guidance makes clear, travel insurance is often limited in scope and focuses on emergency or trip-related needs rather than long-term care across countries.

Worldwide health coverage fills that gap, and it does so comprehensively. A good policy covers:

- Hospital stays and surgical procedures in your country of residence

- Outpatient consultations with doctors and specialists

- Routine and preventive care, including health screenings and vaccinations

- Mental health support and counselling services

- Maternity and reproductive health, depending on the plan

- Emergency medical evacuation and repatriation

Understanding the distinction between travel insurance and health insurance is the first practical step in securing genuine protection for yourself abroad. It also helps to appreciate that the travel insurance vs health insurance debate is not simply about scope. It is about suitability for your actual lifestyle.

Worth remembering: Worldwide health coverage is not just a safety net for worst-case scenarios. It is an ongoing healthcare resource that supports your daily wellbeing, just as your domestic plan would back home. Good medical advocacy and care coordination can make a meaningful difference in how well you navigate healthcare systems in unfamiliar countries.

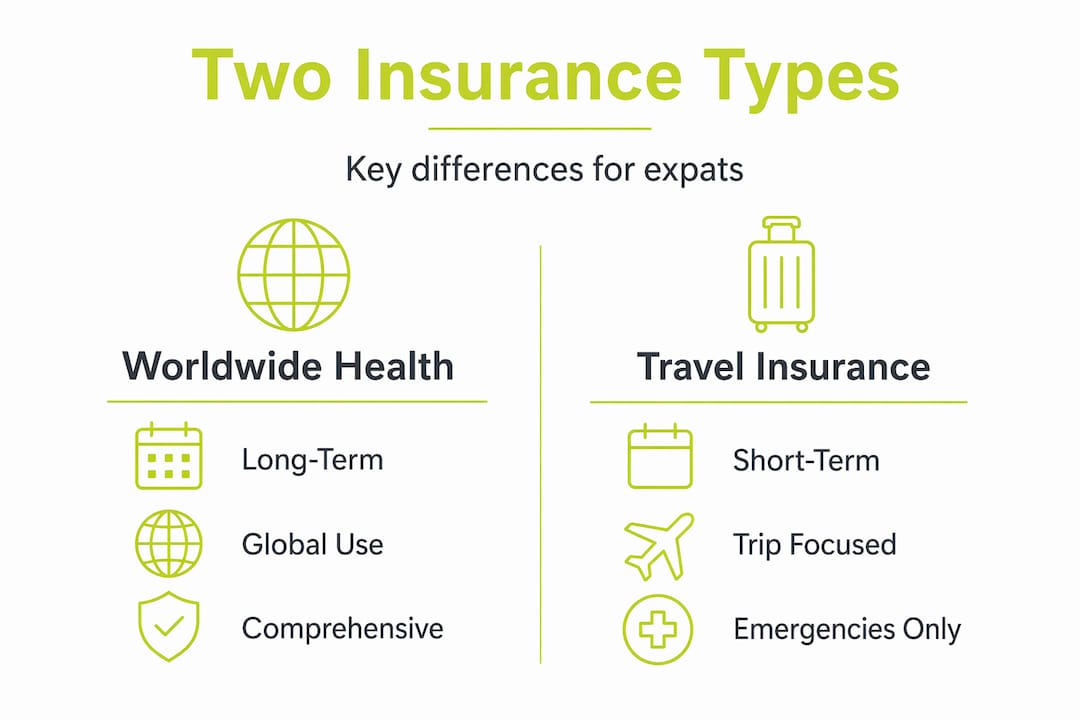

Key differences: Worldwide health coverage versus travel insurance

Now that we have defined both types, let us break down the main differences so you can decide what fits your situation.

| Feature | Worldwide health coverage | Travel insurance |

|---|---|---|

| Duration | Annual, renewable, long-term | Short-term, trip-specific |

| Scope | Routine, preventive, and emergency care | Primarily emergency and trip disruptions |

| Geographic reach | Multiple countries, full-term cover | Country or region for trip duration |

| Chronic conditions | Often covered with declaration | Usually excluded |

| Renewability | Yes, as long as premiums are paid | No, policy ends when trip ends |

| Trip cancellation cover | Rarely included | Core feature |

| Portability | Yes, moves with you between countries | Tied to specific itinerary |

The contrast is stark once you lay it out side by side. Travel insurance is excellent for what it does, but it was designed for holidays and short business trips. It was not designed for the realities of life abroad.

Worldwide health coverage brings several features that travel medical vs health insurance comparisons consistently highlight as critical for long-term residents:

- Chronic disease management with access to specialists over time

- Preventive screenings that catch health issues before they escalate

- Prescription medication cover for ongoing treatments

- Dental and optical add-ons, often available as supplements

- Continuity of care, meaning you see the same doctors and maintain medical records across appointments

When reviewing travel vs health insurance key differences, it is worth noting that emergency coverage under travel insurance often has strict time limits. Many travel policies will cover you for up to 30 or 60 days per trip, but they will not support you through a six-month student visa or a two-year expat placement.

Pro Tip: The most common misconception we hear is that “my travel insurance covers emergency hospitalisation, so I am fine.” Emergency hospitalisation is only one piece of the puzzle. Without follow-up care, prescriptions, and specialist access, a single hospitalisation can still leave you with enormous out-of-pocket costs.

Who needs worldwide health coverage?

With the differences clear, who should invest in worldwide health coverage, and when does it become the non-negotiable choice?

The honest answer is that almost anyone spending more than a few weeks outside their home country can benefit. But there are specific groups for whom it is not just advisable. It is critical.

-

Expatriates on long assignments. Whether you are relocating for one year or five, your home country’s domestic insurance almost certainly does not extend overseas. Expats are often surprised to discover that their existing health plan becomes void the moment they establish residency abroad. Comprehensive international expat health insurance is the practical solution for this group, covering everything from GP visits to complex surgery in your host country.

-

International students. Visa requirements in countries such as Germany, France, Australia, and the United States often mandate specific levels of health insurance coverage. Destination-specific visa and entry rules can make certain insurance types mandatory, even if a broader worldwide policy would otherwise be available. Students who fail to meet these requirements risk visa refusals or deportation. The right international health insurance for students plan accounts for both the academic calendar and local visa stipulations.

-

Professionals working across multiple countries. Digital nomads, international consultants, and business executives who regularly travel between countries need coverage that is truly portable. A policy tied to one country of residence will not serve someone who spends three months in Singapore, then two in Colombia, and then relocates to the Netherlands.

-

Families relocating abroad. Children and dependants require consistent, accessible healthcare. A family moving overseas needs a plan that covers paediatric care, school medicals, and routine check-ups without requiring them to navigate unfamiliar local health systems alone.

-

Retirees living abroad. Many retirees choose countries with lower costs of living, but older travellers face higher health risks and often have pre-existing conditions. Domestic pension health benefits rarely follow retirees abroad.

If you are studying abroad and wondering whether your university’s basic health scheme is sufficient, the short answer is usually no. University plans tend to be bare-bones and institution-specific, leaving you without cover during holidays, internship placements, or travel between terms. A dedicated worldwide health policy removes that uncertainty entirely.

Using a structured travel safety checklist before you depart can help you confirm that your insurance is in order alongside other essential preparations.

What to look for in a worldwide health policy

Once you know worldwide coverage is right for you, choosing the right policy is the next challenge. Not all plans are created equal, and the differences between them can have real consequences for your health and finances.

| Must-have features | Nice-to-have extras |

|---|---|

| Inpatient and outpatient cover | Dental and optical cover |

| Emergency evacuation and repatriation | Maternity cover |

| Prescription medication | Mental health add-ons |

| Pre-existing condition options | Wellness and health screening programmes |

| Portability across countries | Private room upgrades |

| Policy renewability | Alternative therapy cover |

Beyond the table, there are several considerations worth examining in detail when reviewing international insurance plans for expats.

- Geographic exclusions. Some policies exclude specific regions, such as the United States, due to high healthcare costs. If your work or travel takes you there regularly, verify that the US is included or available as an add-on.

- Deductibles and co-payments. A lower premium often means a higher out-of-pocket cost per claim. Understand the financial trade-off before you commit.

- Direct billing arrangements. The best plans allow hospitals to bill your insurer directly, meaning you never need to pay upfront and claim back. This matters enormously in an emergency.

- Pre-existing conditions. Some plans exclude these entirely. Others cover them after a waiting period. A few specialist providers cover them from the outset. Understanding types of expat insurance and how each handles pre-existing conditions can save you from a costly surprise.

- Renewability and age limits. Check whether your plan can be renewed year after year and whether there are age caps that could leave you without cover at 65 or 70.

When comparing top international health insurance plans, look carefully at the claims process. A plan that takes weeks to process reimbursements or requires excessive documentation can be almost as stressful as having no insurance at all.

Pro Tip: Always verify that your chosen policy satisfies the specific legal requirements of your host country. Some nations have exact minimum coverage thresholds for visas or residence permits. A plan that seems comprehensive may fall short of a local authority’s minimum standard if you have not checked the fine print.

Our perspective: What most guides overlook about worldwide health cover

Most articles on worldwide health coverage focus heavily on the headline features: what is covered, what is excluded, and how much it costs. That is all valuable information. But in our experience working with expats, international students, and globally mobile professionals, the most damaging gaps are rarely about the policy itself. They are about the expectations people bring to it.

Here is what we see consistently. People secure a policy, tick the box, and then forget about it until they actually need it. They do not verify that their chosen hospital is on the insurer’s approved network. They do not read the pre-authorisation requirements for specialist referrals. They do not check whether their cover resets at the policy anniversary or operates on a rolling twelve-month basis. These are not edge cases. They are routine administrative points that catch people off-guard at the worst possible moments.

There is also a deeper issue that most guides sidestep. The real cost of inadequate insurance is not the one-time emergency bill. It is the long-term health deterioration that happens when people avoid seeking medical attention because they are uncertain what their policy covers. An expat who delays seeing a specialist for several months because they “think” the consultation might not be covered can end up facing a far more serious and expensive condition down the line. Preventive and routine care is not a luxury feature. It is the financial and medical backbone of a sound worldwide health plan.

We also find that people underestimate how disorienting it can be to access healthcare in an unfamiliar system. Language barriers, different administrative processes, and unfamiliar referral pathways add stress to an already difficult situation. A policy with strong essential expat insurance tips embedded into the customer support model, including multilingual helplines and care coordination, is worth considerably more than a slightly cheaper plan with no support infrastructure.

In short, the policy document matters. But the support system behind it matters just as much.

Find the right worldwide health cover to protect your global lifestyle

Navigating the world of international health insurance can feel overwhelming, but you do not have to do it alone. The right starting point is a clear understanding of what international health insurance actually means for someone in your specific situation, whether that is a student in Germany, an executive in Singapore, or a family settling in Mexico.

At Unparalleled Global Benefits, we specialise in matching expats and international students with plans that genuinely suit their needs. Our resources make it straightforward to compare options side by side, and our guidance on selecting the right expat insurance provider helps you ask the right questions before you commit. You can also browse our curated list of top insurers to find providers with proven track records for international clients. Getting the right cover does not need to be complicated. It just needs to be the right fit for your life abroad.

Frequently asked questions

Is worldwide health coverage mandatory for expats?

Worldwide health coverage is not always legally mandatory for expats, but many host countries and employers require proof of comprehensive health insurance as a condition of residence or employment. Visa and entry rules vary significantly by destination, so always check the specific requirements before you relocate.

Can I use worldwide health coverage as a substitute for travel insurance?

Worldwide health coverage offers broader, longer-term medical protection but typically does not include trip cancellation, baggage loss, or travel delay benefits. As the US State Department notes, travel insurance and health insurance serve different purposes, and many globally mobile individuals carry both.

What happens if I move countries during my policy term?

Many worldwide health policies are designed with portability in mind, allowing your cover to follow you when you relocate to a new country during the policy term. However, always review regional exclusions and notify your insurer of any change in residency to avoid gaps in cover.

Does worldwide health coverage include routine and preventive care?

Most comprehensive worldwide health plans include routine and preventive care such as annual check-ups, vaccinations, and health screenings, though the exact level of cover varies by provider and the tier of plan you select. Always confirm what is included before purchasing a policy.

Recommended

- Expat health insurance: your complete guide for 2026 – Unparalleled Global Benefits

- How to Get Medical Insurance Abroad: Your Essential Guide for Expats and Travelers

- International Expat Health Insurance: Protecting Your Wellness Abroad – Unparalleled Global Benefits

- Essential expat insurance tips: Protect your health abroad – Unparalleled Global Benefits