TL;DR:

- Choosing between local and expat health insurance depends on your travel duration, healthcare needs, and mobility requirements. While local plans are more affordable within a country, expat insurance offers broader coverage and international portability ideal for long-term or multi-country stays. Assess your personal situation carefully, considering coverage, costs, and exclusions, to make an informed and tailored insurance decision.

Moving abroad or spending extended time in another country raises one question that many people underestimate until it’s too late: what kind of health insurance should you choose? You might assume that expat insurance is automatically the superior choice, but the reality is far more nuanced. In Thailand, for example, local IPD and OPD cover costs between $1,800 and $2,800 per year, while a comparable global expat plan can reach $3,500 to $6,000 or more annually. That gap surprises most people. This article breaks down both options clearly so you can make a confident, well-informed decision for your own circumstances.

Table of Contents

- What is expat insurance and local insurance?

- Comparing coverage and exclusions

- Cost breakdown: expat vs local insurance

- Choosing the right cover: practical decision criteria

- Our take: the uncomfortable truth about insurance for expats

- Find the best expat and local insurance for your situation

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Expat vs local costs | Expat insurance is often much pricier than local options, but offers wider coverage and flexibility. |

| Coverage differences matter | Expat insurance covers multiple countries, while local insurance restricts you to that single country’s care network. |

| Portability is crucial | Frequent travellers and global residents benefit from the portability and global claims support unique to expat insurance. |

| Choose cover by needs | Your health, travel plans, and local healthcare standards should drive your insurance decisions. |

| Hybrid solutions exist | Combining local and expat policies can sometimes offer the best value and protection. |

What is expat insurance and local insurance?

Having outlined the cost differences, let’s clarify what expat and local insurance actually are, because these terms are used loosely and the confusion can be costly.

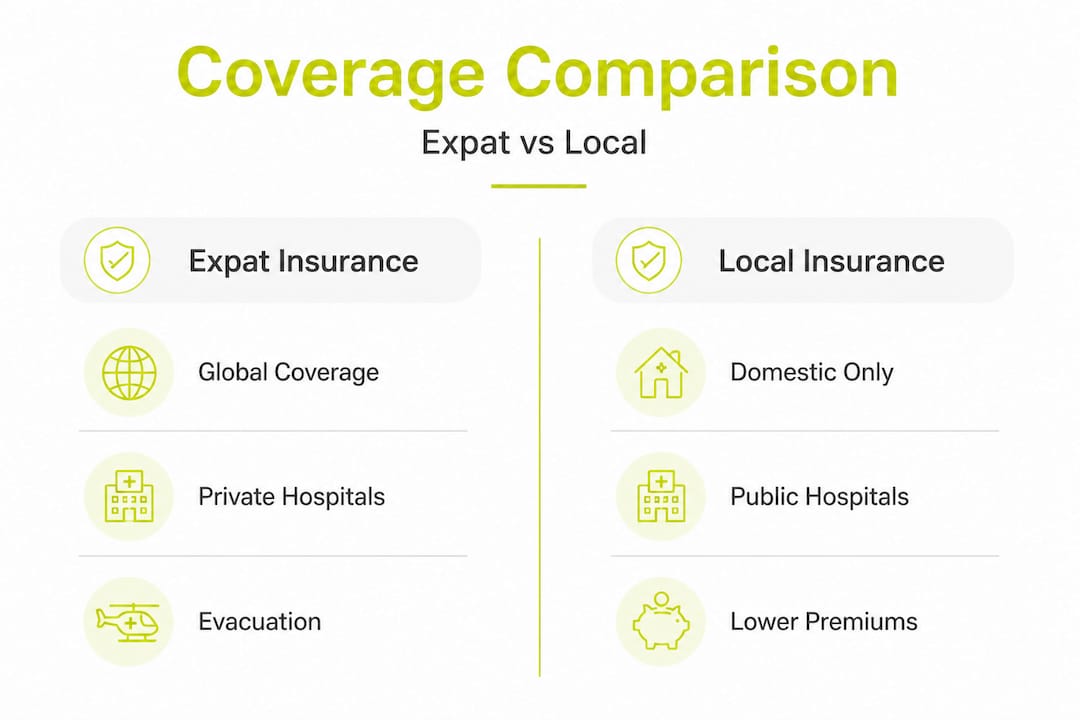

Expat insurance, sometimes called international health insurance, is a policy designed for people living, working, or travelling outside their home country for an extended period. It typically offers coverage across multiple countries, access to private hospitals worldwide, and features such as emergency medical evacuation, repatriation, and global claims support. These policies are built for mobility. If you move between countries for work or live as a digital nomad, expat insurance travels with you.

Local insurance, by contrast, is a health policy purchased in the country where you currently reside. It is regulated by that country’s authorities, priced according to local healthcare costs, and generally valid only within that nation. It covers you at local hospitals and clinics, both public and private depending on the plan tier, and it mirrors what a local resident would buy for themselves.

Understanding which category your situation falls into matters because the two products serve genuinely different needs:

- Travellers on short visits: often better served by travel insurance, which is a separate product again

- Expats on multi-year assignments in one country: may find local insurance perfectly sufficient

- Globally mobile professionals moving between postings: typically need the portability of expat insurance

- Retirees settling permanently abroad: can benefit from either, depending on local healthcare quality

- Families with children in international schools: often choose expat plans for broader specialist access

Coverage depth is a critical distinction. Local plans are country-specific, whereas expat plans can cover you regionally (Asia, Europe) or globally. However, local plans can be excellent in countries with strong private healthcare infrastructure, such as Thailand, Singapore, or Germany.

Pro Tip: Always verify whether a local insurance policy covers treatment at private hospitals, not just public ones, and confirm whether emergency medical evacuation is included. Many affordable local plans exclude both.

For a broader overview of your options, reading up on expat insurance tips can help you frame your thinking before comparing prices. You should also review the types of expat insurance available so you understand exactly what you’re comparing.

Comparing coverage and exclusions

Now that you know what each insurance type means, let’s review their coverage side by side. The differences are significant and knowing them in advance prevents nasty surprises.

| Feature | Expat insurance | Local insurance |

|---|---|---|

| Inpatient hospital care | Yes, globally or regionally | Yes, within country |

| Outpatient consultations | Often included (add-on or standard) | Varies by plan tier |

| Emergency evacuation | Usually included | Rarely included |

| Repatriation | Usually included | Very rarely included |

| Private hospital access | Wide international network | Dependent on local plan |

| Dental cover | Optional add-on | Sometimes included |

| Maternity cover | Optional add-on | Sometimes included |

| Pre-existing conditions | Often excluded initially | Often excluded |

| Portability (multi-country) | Core feature | Not available |

| Claims language support | Multilingual | Local language only |

The table above makes one thing clear: expat insurance wins on breadth, and local insurance often wins on price within a single country context.

Common exclusions to check carefully include:

- Pre-existing conditions: Both plan types may exclude these for an initial period or permanently. Some expat insurers offer moratorium underwriting, which can allow pre-existing conditions to be covered after a period of symptom-free living.

- Dental and optical care: These are rarely covered as standard in either plan type and typically require an add-on.

- Maternity care: High-cost coverage that most insurers treat as optional. If you’re planning a family abroad, this is essential to sort before you need it.

- Mental health treatment: Coverage varies enormously. Some expat plans now include therapy and psychiatric care; many local plans do not.

- Emergency evacuation: Frequently absent from local plans. If you’re in a country where emergency care is limited, this omission can be genuinely dangerous.

“The real cost of local insurance is not always the premium. It is what happens when you need treatment that your policy doesn’t cover.”

For a detailed explanation of what expat health policies include, the expat health insurance explained guide is worth reviewing. You can also explore expat medical plan examples to see how real-world plans are structured and priced.

The claims process also differs meaningfully. With expat insurance, you often deal with an international insurer’s English-speaking team, use a global app, and access direct billing at partner hospitals. With local insurance, the claims process, forms, and dispute resolution are handled in the local language and under local regulations, which can be challenging if your host country language isn’t your own.

Cost breakdown: expat vs local insurance

If coverage is crucial, costs are the next thing expats and travellers scrutinise. Let’s look at the numbers in a structured way.

| Plan type | Annual cost estimate | Inpatient only | Inpatient + Outpatient |

|---|---|---|---|

| Local insurance (Thailand) | $1,000–$2,800 | $1,000–$1,500 | $1,800–$2,800 |

| Global expat insurance | $2,500–$6,000+ | $2,500–$3,500 | $3,500–$6,000+ |

| Regional expat (Asia-focused) | $1,800–$4,000 | $1,800–$2,500 | $2,800–$4,000 |

These figures illustrate the gap clearly. Thailand’s local IPD and OPD plans cost roughly half the price of a global expat equivalent. However, cost alone should never drive the decision.

Several factors directly influence the price you’ll be quoted for either type:

- Your age: Premiums rise significantly with age, particularly for expat plans. A 40-year-old may pay 60 to 80 per cent more than a 30-year-old for the same expat policy.

- Your medical history: Disclosed pre-existing conditions affect both the premium and the exclusions applied. Being upfront during the application process protects you later.

- Your location: Countries with high healthcare costs (the United States, Switzerland, the UAE) mean higher premiums regardless of which type of plan you choose.

- Coverage choices: Adding outpatient, dental, maternity, or evacuation cover increases cost meaningfully. Each add-on should reflect a genuine personal need.

- Excess (deductible) levels: Choosing a higher excess lowers your monthly or annual premium. This can be a sensible strategy if you’re generally healthy and want to save on routine costs.

How to compare costs logically:

- List your actual healthcare needs: Do you have ongoing conditions? Do you visit doctors frequently? Are you planning a family?

- Research the quality of local healthcare in your host country. Countries like Thailand and Germany have strong private hospital networks; others do not.

- Obtain quotes for both local and expat plans with comparable coverage levels, not just headline prices.

- Calculate the true cost: premium plus potential out-of-pocket expenses if excluded services are needed.

- Factor in the cost of evacuation if your host country lacks specialist care, since evacuation flights can cost tens of thousands of pounds.

Hidden costs are real and often ignored. Local plans may quote a low premium but include high per-visit co-payments. Expat plans may appear expensive but include direct billing and evacuation that saves you enormous sums in a crisis. For a structured breakdown of how to approach this, reviewing healthcare access for expats and exploring the insurance plans expert comparison will give you a clearer picture.

Choosing the right cover: practical decision criteria

Understanding costs brings us to the real question: how do you choose what’s right for you? The answer depends on your personal circumstances, not a general rule.

Here is a practical framework for thinking through your decision:

- Length of stay: If you’re in one country for fewer than 12 months, a short-term expat or travel insurance plan may be more appropriate than a full local health insurance policy.

- Residence status: If you have official residency or a long-term visa, local insurance may be accepted or even required by your host country’s authorities.

- Work versus leisure: Employed expats often receive employer-sponsored international health insurance. If yours doesn’t cover private care or evacuation, supplementing it with additional cover makes sense.

- Quality of local healthcare: In some countries, public hospitals are excellent and free. In others, private care is necessary but expensive without insurance. Know your host country’s reality.

- Personal health conditions: Chronic conditions or regular medication needs make comprehensive cover essential. A cheaper plan with exclusions may cost you more over time.

Thailand’s cost advantage for local plans is real, but it only holds if you plan to stay in Thailand long-term and access only Thai hospitals.

Hybrid solutions are worth exploring too. Some expats choose a local plan for day-to-day care and supplement it with a standalone evacuation and repatriation policy for emergencies. This approach can deliver solid value, particularly in countries with strong local hospital networks.

Pro Tip: If you travel between countries frequently, portability is crucial. A local plan ties you to one country’s healthcare system. If you’re regularly crossing borders for work or visits, an expat plan’s international network is a tangible benefit, not just a luxury.

For further guidance on making smart cover choices abroad, and to see real expat insurance examples that may match your situation, both resources are worth your time before committing to a plan.

Our take: the uncomfortable truth about insurance for expats

Most articles on this topic give you a checklist and then tell you to “choose based on your needs.” That is true but incomplete. After years of supporting expats across dozens of countries, we’ve observed a pattern: people make insurance decisions based on the wrong information, usually because they’re comparing headline prices without understanding what they’re actually buying.

The conventional wisdom in online expat forums is to buy the most affordable local plan and save money. Sometimes that advice is right. But it often glosses over the fact that local plans can have coverage ceilings that are dangerously low, networks that don’t include the best hospitals, and absolutely no provision for getting you home if you’re critically ill.

We’ve also seen the opposite mistake. Expats paying for premium global plans in countries with excellent, affordable private healthcare because “that’s what expats do.” They’re spending twice as much for portability they never use.

The uncomfortable truth is this: there is no universally correct answer, and anyone who tells you otherwise is simplifying to the point of being misleading. What we’d advocate for instead is honest self-assessment combined with proper professional advice. Ask yourself whether you’ve actually read your policy’s exclusions list. Ask whether you know what happens if you need a specialist procedure not available in your host country. Ask whether your insurer has a 24-hour emergency line and whether you’ve tested it.

Hybrid strategies, local insurance for routine care supplemented by an evacuation policy, are underused and often undervalued. They can provide real-world protection at a fraction of the cost of a full expat plan. We explore this further in our perspective on why international health insurance remains important even when local options look attractive.

The lesson: stay flexible, ask difficult questions, and never assume that the most expensive option is the safest one.

Find the best expat and local insurance for your situation

Ready to look at practical options? Here’s where to start comparing real plans. Making the right choice becomes much more straightforward when you have side-by-side comparisons and expert guidance specific to your destination and personal profile.

At Unparalleled Global Benefits, we’ve helped thousands of expats, travellers, families, and remote workers find the cover that genuinely fits their lives. Whether you’re weighing up a local plan in Southeast Asia or exploring a global expat policy for a multi-country assignment, our team can walk you through the options clearly and without pressure. Explore international expat health insurance options, compare the types of expat insurance available to you, and review our top insurers to get started with a quote tailored to your circumstances.

Frequently asked questions

Is expat insurance always more expensive than local insurance?

Expat insurance tends to cost significantly more, sometimes double the price of local insurance. In Thailand, local IPD and OPD plans range from $1,800 to $2,800 annually, while global expat plans run from $3,500 to $6,000 or more, though the broader coverage and portability can justify the price gap for many expats.

Can I switch between local and expat insurance easily?

Switching is possible, but you may face waiting periods, new exclusions for pre-existing conditions, or significant paperwork depending on your insurer and host country’s regulations.

Do local insurance policies cover treatment in other countries?

Most local insurance policies restrict coverage to healthcare received within the country itself, while expat insurance is specifically designed to cover you across multiple regions or globally.

What are the main exclusions I should check?

Always examine your policy carefully for exclusions on pre-existing conditions, dental care, maternity, mental health treatment, and emergency evacuation, particularly when reviewing local insurance plans, as these are frequently absent or limited.

Recommended

- Understanding expat insurance: benefits, cover, and what you need – Unparalleled Global Benefits

- Selecting The Right “Expat Insurance Provider”

- Types of expatriate insurance: smart cover choices abroad – Unparalleled Global Benefits

- Travel vs expat insurance: choose the right cover abroad – Unparalleled Global Benefits

- Compare the Best Providers: Aviva, AXA Health and Bupa