TL;DR:

- Public healthcare for expats is limited and often requires private insurance for full access.

- Language barriers and high costs deter over 80% of expats from seeking healthcare abroad.

- Many countries mandate private insurance proof for visas, making it essential for legal residency.

Moving abroad rarely comes with a healthcare manual. Many expats assume they will slot into the local public system, only to discover that public healthcare access is largely unavailable to non-residents without private insurance. Navigating pricing structures, understanding emergency fallback options, and meeting mandatory insurance requirements are challenges that can feel overwhelming when you are settling into a new country. This guide walks you through the realities of healthcare access for expats, what the barriers look like in practice, and how to secure the right private cover for your situation.

Table of Contents

- Understanding healthcare limitations for expats

- Key barriers: Language, finance, and local policy

- Comparing private health insurance options for expats

- Navigating mandatory insurance and visa requirements

- Why the true cost and complexity of healthcare access for expats is misunderstood

- Expert solutions for expats: Find your tailored health insurance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Limited public access | Expats usually cannot use subsidised public healthcare and must seek private solutions. |

| Barriers to care | Language, financial costs, and complex local policies are key hurdles in receiving treatment abroad. |

| Insurance strategies | Choosing the right cover requires balancing deductibles, policy options, and regional legal mandates. |

| Mandatory proof for visas | Countries increasingly require health insurance for visa and residency applications, shaping your available choices. |

| Practical advice | Preparation and expert support are your best tools for securing reliable care and cover as an expat. |

Understanding healthcare limitations for expats

Most people relocating abroad expect a seamless transition into local services. The reality is considerably more complex. Public healthcare is rarely subsidised for expats in host countries, meaning you are typically responsible for the full cost of treatment unless you carry private insurance. Emergency services may provide a safety net, but even those come with significant caveats around cost and eligibility.

Thailand offers a useful illustration. Expats living there can access emergency services at public hospitals, but they face tiered pricing structures designed specifically for foreign nationals. Routine care, specialist appointments, and elective procedures are priced at a premium compared to what Thai residents pay. This is not unique to Thailand. Similar patterns exist across Southeast Asia, Latin America, and parts of Eastern Europe, where public systems prioritise citizens and registered taxpayers.

“Expats typically lack access to subsidised public healthcare in host countries and must rely on private insurance or limited public emergency services.”

Understanding the types of expat insurance available to you is one of the most important steps you can take before relocating. The landscape spans everything from basic inpatient cover to comprehensive global plans that include outpatient, dental, and maternity care.

Here are the most common limitations expats face with public healthcare:

- No access to subsidised GP visits without residency or national insurance contributions

- Emergency care provided at full price, often requiring upfront payment before treatment

- Lengthy queues and limited English-language support in public facilities

- Chronic condition management largely excluded from public emergency pathways

- Visa applications often require proof of private insurance before arrival

The issue of public healthcare limitations is not just financial. It also relates to the quality of care available to non-residents, the administrative burden of accessing services without local documentation, and the language gap that creates friction at every stage of the process.

Planning before you move, rather than after a medical event occurs, puts you in a far stronger position. Reactive decisions made during a health crisis are rarely cost-effective or well-matched to your actual needs.

Key barriers: Language, finance, and local policy

Once you understand why public healthcare falls short for expats, it becomes essential to look at the specific barriers that prevent people from seeking care at all. These are not hypothetical concerns. The data reflects a widespread pattern across international populations living and studying abroad.

Research published in peer-reviewed literature found that 80.8% of international residents avoid seeking healthcare due to a combination of language difficulties and financial concerns. That is a striking figure. It means the majority of people in this situation are making decisions not based on their health needs, but based on fear of cost or miscommunication.

Language barriers create real problems at every stage of care. When you cannot fully communicate symptoms, understand a diagnosis, or navigate paperwork in the local language, the risk of receiving suboptimal care increases significantly. Even in countries with well-resourced healthcare systems, the absence of interpreter services at public facilities can leave expats feeling isolated and uncertain.

Financial barriers are equally significant. Without insurance, even a single hospital admission can cost thousands of pounds, euros, or dollars. In countries where upfront payment is required before treatment begins, the consequences of arriving uninsured can be severe.

Hospital capacity also varies considerably by country. Germany, for example, maintains approximately 7.5 hospital beds per 1,000 people, reflecting one of the highest healthcare infrastructures in Europe. This contrasts sharply with many popular expat destinations in Asia or Central America, where capacity is considerably lower and private hospitals are often the only reliable option for quality care.

Practical steps to reduce your vulnerability to these barriers include:

- Researching local healthcare infrastructure before committing to a destination

- Selecting insurance with multilingual support and a 24/7 helpline

- Downloading medical translation apps as a supplementary tool

- Keeping a brief medical summary in the local language for emergencies

- Following healthy travel tips to reduce the frequency of medical contact needed

Good expat insurance tips consistently highlight that understanding your local environment is just as important as selecting the right policy. The two decisions are interdependent.

Comparing private health insurance options for expats

Now that the barriers are clear, the practical question becomes: which type of private health insurance actually addresses your needs, and what does it cost?

The range of products available to expats is broader than most people realise. Below is a simplified comparison of the main policy structures:

| Policy type | Coverage scope | Approximate monthly cost | Best suited for |

|---|---|---|---|

| Inpatient only | Hospitalisation and surgery | £60 to £120 | Healthy, younger expats |

| Comprehensive | Inpatient, outpatient, dental | £150 to £350 | Families and long-term expats |

| US-linked plan | Global including USA | £280 to £600 | Frequent US travellers |

| Local market plan | Country-specific coverage | £40 to £90 | Single-destination expats |

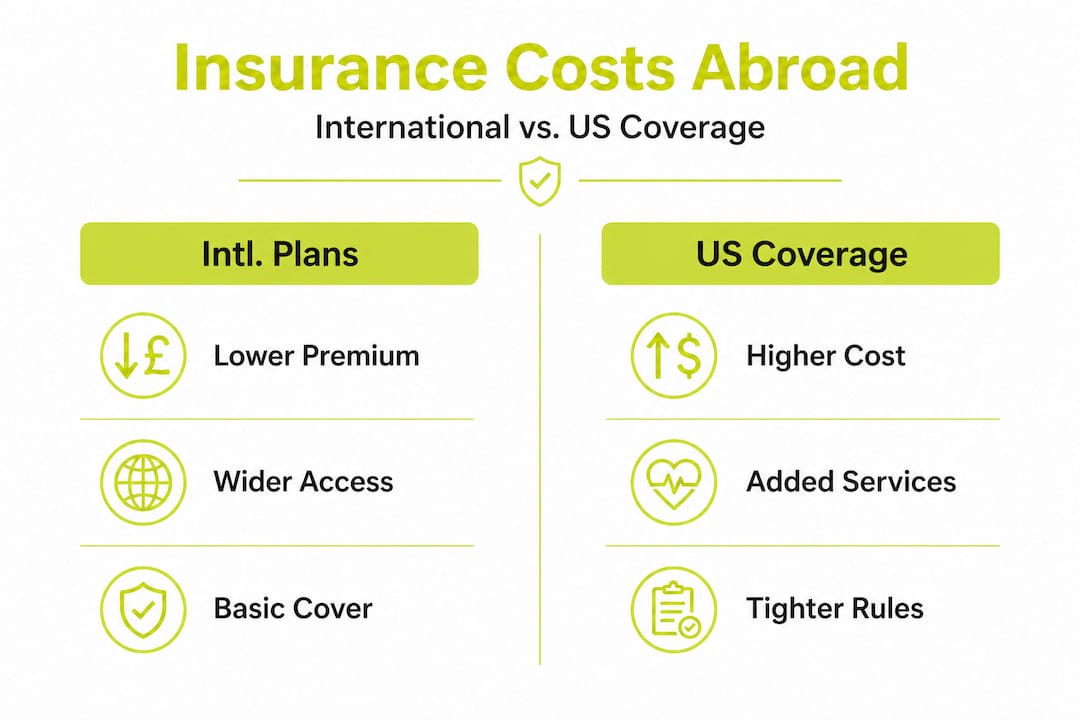

The cost difference between standard international plans and US coverage is substantial, often doubling the premium. If you do not intend to seek medical care in the United States, excluding it from your policy is one of the simplest and most effective ways to reduce costs without sacrificing meaningful protection.

Higher deductibles are another tool for managing premiums. Choosing a policy with a higher annual excess (for example, £1,500 rather than £250) can reduce your monthly premium significantly. The trade-off is that you absorb more out-of-pocket cost for minor claims. This works well for expats who are generally healthy and primarily want protection against catastrophic events rather than routine care.

Chronic condition coverage deserves particular attention. Underwriting practices vary considerably across insurers. Some will exclude pre-existing conditions entirely, others will cover them after a waiting period, and a few specialist providers will include them from day one at a higher premium. Reading the underwriting terms carefully is essential before signing anything.

To approach this systematically, consider these steps:

- List your existing health conditions and any regular medications you require

- Identify which countries you plan to visit, particularly whether the USA is on your itinerary

- Set a realistic budget that accounts for both premiums and potential excess payments

- Decide on your priority coverage, whether inpatient-only or comprehensive

- Compare at least three to five providers before making a final decision

You can compare health care insurance options through trusted platforms designed specifically for expats, which simplifies the process considerably. Reviewing an international insurance plans comparison gives you a clearer sense of how products differ across providers and regions.

Pro Tip: Do not overlook dental and vision when selecting your plan. Many expats assume these are covered as standard, but they are frequently add-ons. The cost of choosing dental insurance separately can exceed £600 annually in some markets, making a bundled plan more economical.

Navigating mandatory insurance and visa requirements

Understanding insurance products is one part of the picture. Knowing which regulations apply to your specific visa or residency status is equally important, and in some countries, non-compliance carries serious consequences.

Several popular expat destinations have made proof of health insurance a formal requirement for visa applications and residency permits. This is not merely a recommendation. It is a legal condition.

| Country | Insurance requirement | Type of visa affected |

|---|---|---|

| UAE | Mandatory employer or individual cover | All residency visas |

| Portugal | Valid health insurance required | D7, digital nomad visa |

| Schengen Area | Minimum £27,000 coverage | All Schengen tourist/short-stay visas |

| Thailand | Specific plans for long-stay visas | Retirement and long-stay visas |

Visa mandates for insurance in countries like the UAE and Portugal reflect a broader trend. Governments increasingly want assurance that foreign nationals will not place undue financial pressure on public health services. For you as an expat, meeting these requirements is about more than compliance. It is about securing your access to care if something goes wrong.

Here is what to keep in mind when aligning your cover with local requirements:

- Check the minimum coverage limit specified for your destination’s visa type before purchasing any plan

- Ensure your policy document is available in the host country’s language or accompanied by a certified translation

- Confirm that your insurer is recognised by local authorities, particularly in the UAE where approved insurer lists exist

- Review your policy renewal dates to ensure continuous cover throughout your residency period

- Understand what constitutes an approved policy in your destination country, as some exclude certain provider types

Consulting a dedicated expat health insurance guide before applying for your visa can save you from submitting inadequate documentation, which can result in delays or refusals.

Pro Tip: If you are relocating to a Schengen country long-term, your short-term Schengen travel insurance is unlikely to meet residency visa requirements. You will typically need a full international health plan rather than a travel policy.

Why the true cost and complexity of healthcare access for expats is misunderstood

Here is what most guides will not tell you directly: the most common mistake expats make is treating insurance as a box-ticking exercise rather than a strategic decision.

When expats approach insurance purely by price, they often end up with policies that look adequate on paper but fail them at the moments that matter most. A plan that excludes outpatient care sounds affordable until you are paying £200 per GP visit out of pocket. Inpatient-only cover is excellent for a healthy 28-year-old moving to Lisbon. It is potentially catastrophic for a 50-year-old with managed hypertension moving to Bangkok.

The regulatory landscape adds another layer that most price-comparison guides simply ignore. Wellness abroad insurance needs to account for the country you are in now, the countries you will visit, your specific health profile, and the visa conditions attached to your stay. These four variables interact in ways that a generic plan rarely addresses.

We have also observed that many expats underestimate how quickly local regulations can change. What was a compliant plan in the UAE three years ago may no longer meet the current requirements from the Dubai Health Authority. Keeping your insurance under annual review is not overcautious. It is practical.

The uncomfortable truth is that price-driven decisions are often driven by optimism bias: the belief that a medical event is unlikely to happen to you. The data suggests otherwise. Most long-term expats will encounter at least one significant health event during a multi-year stint abroad, whether an accident, illness, or the management of an existing condition. Choosing a plan based on what you hope will happen, rather than what could realistically occur, is a risk that rarely pays off.

Balanced decisions, which weigh premium costs against genuine coverage quality and regulatory compliance, consistently deliver better outcomes for expats over a two to five year horizon.

Expert solutions for expats: Find your tailored health insurance

Understanding the complexity of expat healthcare is the first step. Finding a solution that addresses it properly is the next one.

At Unparalleled Global Benefits, we work specifically with expats, travellers, and international families to identify cover that fits their real situation, not a generic profile. Whether you need expat health insurance that meets visa requirements, a plan that covers a pre-existing condition, or a policy that follows you across multiple countries, our team helps you navigate the options with clarity. Explore the full range of expat insurance types available through our platform, or browse our curated list of top insurers abroad to begin comparing providers today. The right cover is out there. Let us help you find it before you need it.

Frequently asked questions

Can expats use public healthcare in their host country?

Most expats cannot access subsidised care and must rely on private insurance or restricted emergency services available at full cost.

How much does international health insurance cost for expats?

Costs vary widely, but excluding US coverage can halve your premium, with comprehensive plans typically ranging from £150 to £350 per month.

Is health insurance a requirement for visas and residency?

Yes, in many countries. UAE and Portugal both mandate valid health insurance as a formal condition of residency visa applications.

What are the main reasons expats avoid seeking healthcare abroad?

Language and financial barriers affect over 80% of international residents, causing many to delay or entirely avoid seeking necessary care.

Are emergency services available to uninsured expats?

Emergency care may be accessible, but public emergency services typically come at full price for non-residents and represent a temporary fallback rather than a sustainable solution.

Recommended

- Compare Health Care Insurance for Expats: Step-by-Step Guide – Unparalleled Global Benefits

- Essential expat insurance tips: Protect your health abroad – Unparalleled Global Benefits

- United HealthCare International Cover – Vital for Expats – Unparalleled Global Benefits

- Types of expatriate insurance: smart cover choices abroad – Unparalleled Global Benefits

- Can You Travel Outside Ontario and Still Use OBSP? What Patients Need to Know – Valence Medical Imaging

- Why Kuwaiti Families Trust Swiss Healthcare Access | Young Explorers Club Switzerland