TL;DR:

- Understanding key insurance terms like deductible, co-payment, and exclusions prevents costly misunderstandings abroad.

- Comparing plan details such as maximum benefits, deductibles, and in-network providers ensures appropriate coverage.

- Investing one hour in reading and clarifying policy language enhances protection and financial security overseas.

Moving abroad is exciting, but the first time you face a medical situation overseas and discover your claim has been rejected due to a “policy exclusion” you never noticed, that excitement can turn to panic very quickly. Insurance jargon is genuinely confusing, and for expatriates and international travellers, misunderstanding even a single term can mean paying thousands out of pocket. This guide is here to change that. We will walk through the most important insurance terms you need to know, explain what they mean in plain language, and show you how to apply that knowledge when it matters most, whether you are renewing a visa, checking into a hospital, or simply comparing plans before your move.

Table of Contents

- Why expat insurance terminology matters

- Essential expat insurance terms and clear definitions

- Comparing insurance plan features: understanding the fine print

- Getting the most from your cover: practical scenarios for expats

- Why most expats overlook the value of mastering insurance terminology

- Explore expert resources for the right expat insurance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know the basics | Understanding common insurance terms prevents costly mistakes when using your cover abroad. |

| Compare carefully | Always scrutinise the details in different policies before purchasing expat insurance. |

| Clarify with providers | Consult your insurer about unclear terms before an emergency arises. |

| Use scenarios | Learn through examples to see how misunderstandings can impact real-life outcomes. |

Why expat insurance terminology matters

Expat insurance is not the same as domestic health cover. When you live or travel internationally, your insurance must account for different healthcare systems, currencies, regulatory frameworks, and medical standards across multiple countries. That added complexity means the policy language is often more intricate, and the consequences of misunderstanding it are far greater.

Consider what happens when an expat in Southeast Asia is hospitalised unexpectedly. If they do not understand the term “pre-authorisation” (which means getting advance approval from the insurer before a procedure or hospital admission), they may receive treatment that the insurer later refuses to pay for. That single misunderstanding can result in a bill totalling tens of thousands of pounds.

Understanding expat insurance types is the first step, but knowing the language behind those types is what truly protects you. Here are the most common scenarios where term literacy makes a tangible difference:

- Visa applications: Many countries require proof of specific cover thresholds. If you do not understand what “annual maximum benefit” means, you could submit a policy that does not meet the minimum requirements.

- Emergency admissions: Knowing what constitutes an “in-network” provider determines whether costs are covered or reimbursed at a reduced rate.

- Routine care: Terms like “waiting period” directly affect when you can use your cover after the policy start date.

- Claim submissions: Misidentifying a “co-payment” versus a “deductible” can lead to incorrect expectations about your out-of-pocket costs.

“The biggest source of insurance disputes is not fraud, it is misunderstanding. When policyholders read what they think a term means rather than what it actually means, outcomes suffer for everyone involved.” This principle applies especially to international health cover, where there is often no fallback domestic system to absorb the costs.

Following health tips for travellers is essential, but so is understanding the safety net that supports you if your health does falter. Term literacy is not optional for expats; it is a practical necessity.

Essential expat insurance terms and clear definitions

With the context set, let us look at the specific terms you must know to get the cover and care you expect abroad. The table below provides clear, plain-language definitions for the most critical insurance terms you will encounter in any international health or travel policy.

| Term | Plain-language definition |

|---|---|

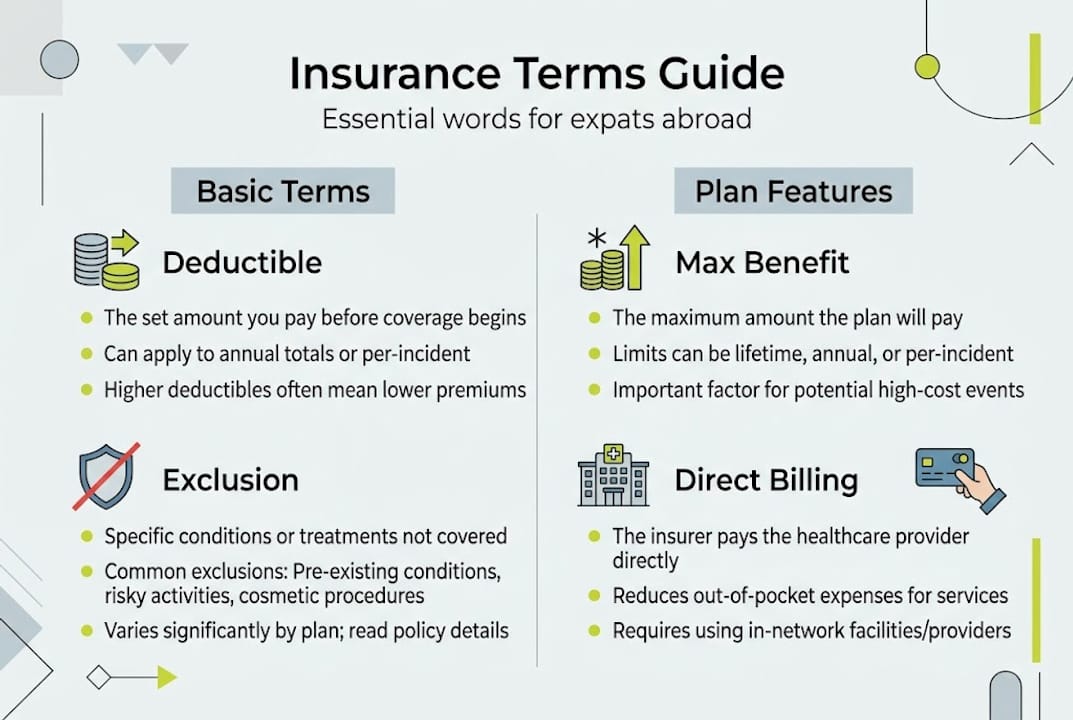

| Deductible | The fixed amount you pay out of pocket before your insurer begins covering costs. A £500 deductible means you pay the first £500 of any claim. |

| Co-payment | A fixed fee you pay per medical visit or prescription, regardless of the total bill. For example, £30 per GP visit. |

| Co-insurance | The percentage of costs you share with your insurer after the deductible is met. An 80/20 split means the insurer pays 80%, you pay 20%. |

| Exclusion | Any condition, treatment, or circumstance your policy will not cover. Common exclusions include pre-existing conditions and elective procedures. |

| Pre-authorisation | Advance written approval from your insurer required before undergoing certain procedures or hospital admissions. |

| Direct billing | An arrangement where your insurer pays the hospital or clinic directly, so you do not need to pay upfront and claim later. |

| Annual maximum benefit | The total amount your insurer will pay out in a single policy year. Once reached, you are responsible for all further costs. |

| Waiting period | A defined time after your policy starts during which certain benefits are not yet available. |

| In-network provider | A hospital, clinic, or doctor that has an agreement with your insurer, usually resulting in lower costs or direct billing. |

| Reimbursement | A process where you pay medical costs upfront and submit a claim to recover those costs from your insurer. |

Understanding how expat health insurance works becomes much simpler once these terms are familiar to you. A few of these deserve extra attention because they are so frequently misunderstood.

Exclusions are particularly important. Many people assume their policy is broad and only notice exclusions at the claim stage. Always read the exclusions section of any policy document first, not last.

Pre-authorisation trips up a surprising number of expats. In an emergency, your insurer may waive this requirement, but for planned procedures it is non-negotiable. Always confirm this in writing before proceeding.

Pro Tip: When reading a policy document, highlight every term you do not immediately understand and look each one up using your insurer’s glossary or contact their support team directly. A 30-minute call before your policy starts can prevent a costly dispute months later.

For visa applications and hospital admissions specifically, these terms are most frequently scrutinised:

- Annual maximum benefit (must meet host country thresholds)

- Territorial coverage (confirms which countries are included)

- Medical evacuation benefit (often required for remote postings)

- Waiting period for pre-existing conditions

You will find more insurance tips for expats to complement the terminology knowledge you are building here.

Comparing insurance plan features: understanding the fine print

Having a glossary is just the start. The real test is making sense of plan differences when you are actually shopping for insurance. Two plans may look similar at first glance, but the definitions buried in the small print can make them dramatically different in practice.

Consider these two sample plans side by side:

| Feature | Plan A | Plan B |

|---|---|---|

| Annual deductible | £500 | £1,000 |

| Annual maximum benefit | £1,000,000 | £500,000 |

| Co-insurance | 90/10 | 80/20 |

| Direct billing available | Yes, worldwide | Yes, select regions only |

| Pre-authorisation required | For inpatient only | For all procedures over £200 |

| Maternity cover | Included after 10-month wait | Optional add-on |

| Dental cover | Basic emergency only | Routine and emergency |

| Medical evacuation | Included | Not included |

Plan A may carry a lower deductible but read Plan B’s co-insurance carefully: you shoulder 20% of every bill after the deductible, whereas Plan A leaves you with only 10%. On a £50,000 hospitalisation, that difference means £5,000 more out of your pocket with Plan B.

When analysing policy documents and comparing plans, follow these steps:

- List your must-have benefits before you read any policy. Medical evacuation, maternity cover, and direct billing are common priorities for expats.

- Read the definitions section first. Every policy defines its key terms. “Emergency” in one plan might exclude anything that is not immediately life-threatening; another may cover urgent care broadly.

- Check the exclusions section in full. Do not skim this section. Look specifically for pre-existing condition clauses, mental health exclusions, and geographical restrictions.

- Compare annual limits per category. Some plans cap dental, physiotherapy, or mental health at very low annual sub-limits even if the overall annual maximum is high.

- Verify the direct billing network. Ask the insurer for their current list of in-network hospitals in your country of residence before you commit.

- Confirm the claims process. Understand whether you will need to submit paper or digital claims, typical processing times, and what documentation is required.

A common trap with travel medical insurance for expats is the varied definition of “emergency.” If your plan only covers emergencies that are immediately life-threatening, a serious but non-critical illness may fall into a grey area, leaving your claim in dispute. Always ask your insurer to clarify this definition in writing before you travel or relocate.

Getting the most from your cover: practical scenarios for expats

Now that you can read the fine print, let us see how these terms play out when you are on the ground and genuinely need your cover to work.

Scenario one: planned hospital admission. You need a minor surgical procedure. You contact your insurer and request pre-authorisation. They approve the procedure and confirm the hospital is in-network, meaning direct billing applies. You check in, receive treatment, and leave without paying anything upfront. Term literacy just saved you a potentially stressful reimbursement process.

Scenario two: unexpected emergency. You are in a country with no in-network hospitals nearby. You need immediate treatment and cannot wait. Most international policies waive pre-authorisation for genuine emergencies. You receive care, keep all receipts, and submit a reimbursement claim within 30 days. Knowing this process in advance means you focus on recovery, not paperwork.

Scenario three: routine GP visit. You visit a local doctor and pay a co-payment of £25 per the terms of your policy. You do not submit a claim because co-payments are your fixed share of routine visit costs. Understanding this prevents unnecessary admin and sets accurate expectations about what you will spend on everyday healthcare.

Maintaining your wellness protection abroad is about proactive planning, not just reactive claiming. Access trusted international clinics through your insurer’s network whenever possible to keep costs predictable.

These are the five most common mistakes expats make with insurance language:

- Assuming exclusions are standard. Every insurer defines exclusions differently. Never assume what is excluded based on a previous policy.

- Confusing co-payment with co-insurance. They sound similar but work very differently and affect your budget in distinct ways.

- Ignoring waiting periods. Arriving at your destination and then discovering maternity cover or pre-existing condition cover has a 12-month waiting period is a deeply unpleasant surprise.

- Failing to get pre-authorisation in writing. A verbal agreement with an insurer representative is not sufficient. Always have written confirmation.

- Not checking the annual maximum mid-year. If you have an ongoing health issue, track your cumulative claims against the annual maximum so you are never caught off guard.

Pro Tip: Before your policy goes live, schedule a short call with your insurer and run through two or three hypothetical scenarios relevant to your lifestyle. Ask them to walk you through the exact process and terminology that would apply. This one step can reveal gaps or misunderstandings before they become problems.

Why most expats overlook the value of mastering insurance terminology

Here is the honest truth: most expats treat insurance documents the way most people treat terms and conditions on a new app. They scroll to the bottom and tick the box. It is entirely human. The language is dense, the situations feel abstract, and when you are excited about a new life abroad, reading policy definitions feels like the last thing you want to do.

But experience, particularly the experience of watching expats navigate unexpected medical bills, teaches a hard lesson. The gap between what people believe their policy covers and what it actually covers is where financial distress begins. One misunderstood exclusion, one missed pre-authorisation, one confused co-insurance percentage can mean a bill that takes years to recover from financially and emotionally.

The counterintuitive insight here is this: you do not need to become an insurance expert. You need to invest roughly one hour up front. Read the definitions section. Call your insurer with specific questions. Confirm the claims process before you need it. That single hour of attention to secure expat care is worth more than any amount of worrying after the fact. Term fluency is not a burden; it is a form of freedom.

Explore expert resources for the right expat insurance

You now have a solid foundation in the terminology that shapes your international health and travel cover. That knowledge puts you in a much stronger position when evaluating, purchasing, or renewing a policy abroad.

At Unparalleled Global Benefits, we have built our resources specifically to help expats like you make confident, informed insurance decisions. From detailed plan breakdowns to side-by-side comparisons, our guides translate complex policy language into clear, actionable information. Explore your expat health insurance options to see how different plans align with your needs, or review the full range of insurance types for expats to ensure your cover reflects the life you are actually living abroad.

Frequently asked questions

What does a deductible mean in expat insurance?

A deductible is the amount you must pay out of pocket before your insurance starts covering costs. For example, with a £500 deductible, you pay the first £500 of any claim and your insurer covers the remainder.

Why are exclusions important to check in policy documents?

Exclusions are specific conditions, treatments, or circumstances your insurance will not cover, and missing them can leave you facing unexpected, significant costs when living or travelling abroad.

What is direct billing in global insurance?

Direct billing is an arrangement where your insurer pays the medical provider directly on your behalf, removing the need for you to pay upfront and then submit a reimbursement claim.

How can I confirm my insurance covers the hospitals I use overseas?

Request a current list of in-network hospitals and clinics from your insurer before you need treatment, and verify coverage for your specific country of residence or travel destination.

Is co-payment different from co-insurance?

Yes, a co-payment is a fixed amount you pay per visit or per prescription, while co-insurance is a percentage of the total treatment cost that you share with your insurer after your deductible has been met.

Recommended

- Understanding expat insurance: benefits, cover, and what you need – Unparalleled Global Benefits

- Step-by-step guide to expat insurance: secure global cover – Unparalleled Global Benefits

- Essential expat insurance tips: Protect your health abroad – Unparalleled Global Benefits

- Why expats need insurance: Safeguard your life abroad – Unparalleled Global Benefits