If you travel internationally several times each year, relying on single-trip policies can drain your budget and leave gaps in protection. Many frequent travellers mistakenly purchase separate cover for each journey, unaware that annual multi-trip travel insurance offers comprehensive protection across unlimited trips within twelve months. This guide explains what these policies cover, how they adapt to your health and age, and why choosing the right annual plan delivers peace of mind and financial savings for expatriates and globetrotters alike.

Table of Contents

- Understanding Multi Trip Travel Insurance Policies

- Key Coverages And Rising Claim Trends

- How Age And Health Affect Premiums And Coverage

- Choosing The Right Policy For Your Travel Needs

- Explore Tailored International Insurance Solutions

Key takeaways

| Point | Details |

|---|---|

| Annual policies cover multiple trips | Most plans allow unlimited journeys within a year, each typically limited to 21, 31, or 45 days duration. |

| Core coverages protect finances and health | Emergency medical expenses, trip cancellation, possessions, and disruption are standard inclusions. |

| Age and health influence premiums | Older travellers and those with pre-existing conditions face higher costs and stricter medical assessments. |

| Medical claims dominate | Rising claim volumes show emergency medical costs constitute the largest share of payouts recently. |

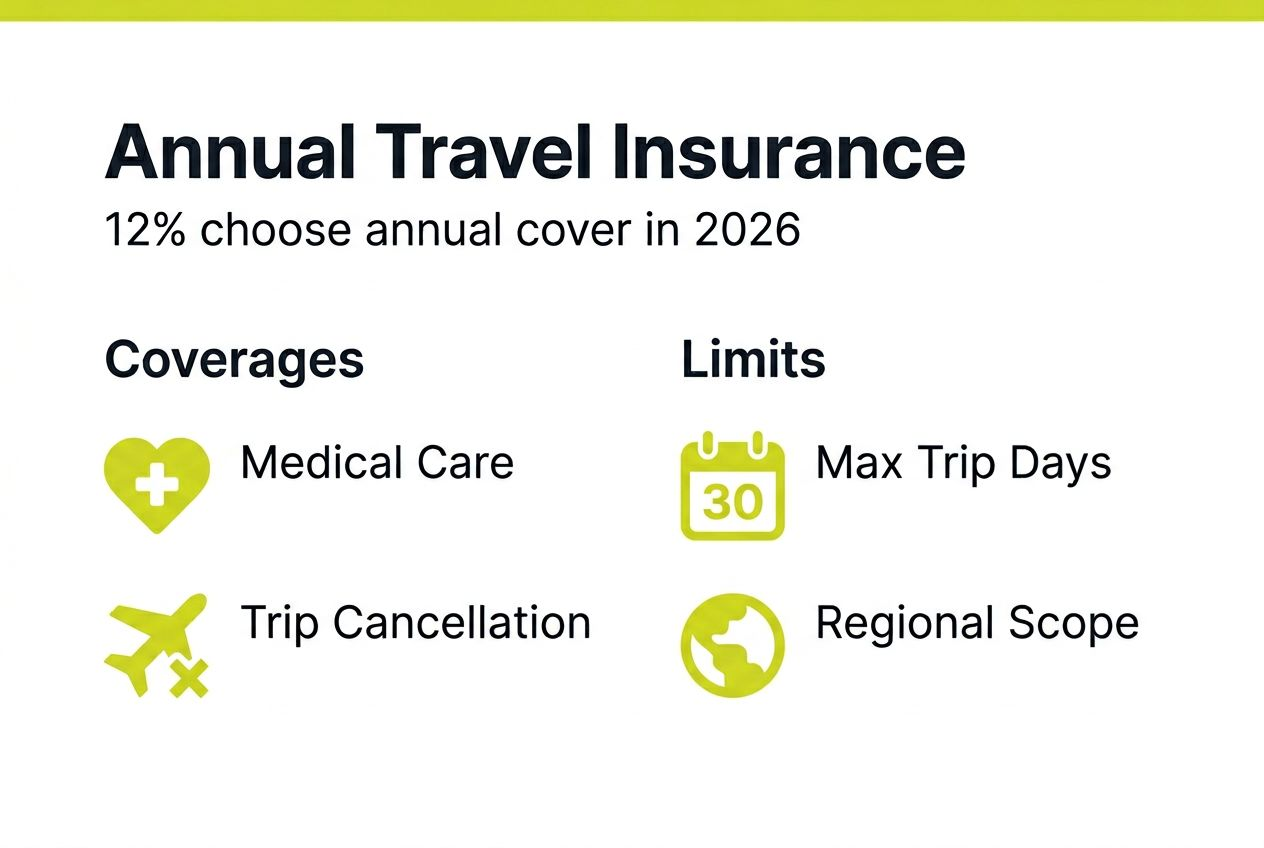

| Growing market share | Roughly 12% of travel insurance buyers opted for annual coverage in 2025, reflecting increasing popularity. |

Understanding multi trip travel insurance policies

Multi trip travel insurance, also called annual travel insurance, is a single policy that covers you for multiple journeys over a twelve-month period. Unlike single trip insurance expat cover that protects one holiday, annual plans let you travel repeatedly without purchasing fresh policies each time. This convenience suits expatriates, business travellers, and anyone making several international trips annually.

Typical coverage includes emergency medical treatment, hospital stays, repatriation, trip cancellation and curtailment, personal possessions protection, and compensation for delays or disruptions. Annual multi-trip travel insurance policies often include coverage for domestic trips within the UK, Europe, and worldwide travel, provided each trip adheres to the policy’s maximum duration. This geographic flexibility means you can hop between continents without worrying about separate regional policies.

Most insurers impose a maximum trip length per journey, commonly 21, 31, or 45 days depending on the tier you select. If a single trip exceeds this limit, you’ll need supplementary cover or a different product. The table below illustrates typical duration and geographic options:

| Policy tier | Maximum trip duration | Geographic coverage |

|---|---|---|

| Basic | 21 days | UK and Europe |

| Standard | 31 days | Worldwide excluding USA/Canada |

| Premium | 45 days | Worldwide including USA/Canada |

Understanding these parameters ensures you choose a policy that matches your travel patterns. If you regularly spend six weeks abroad, a 45-day limit is essential. Conversely, frequent short breaks fit comfortably within 21-day caps, often at lower premiums.

Key coverages and rising claim trends

Emergency medical expenses form the cornerstone of multi-trip travel insurance coverage. Policies typically cover hospital admissions, specialist treatment, emergency dental care, and medical repatriation if you fall seriously ill or suffer injury abroad. Repatriation alone can cost tens of thousands of pounds, making this protection invaluable for travellers venturing beyond the UK.

Cancellation and trip curtailment coverage protects your financial outlay if unforeseen events force you to cancel or cut short a journey. Covered reasons usually include sudden illness, family bereavement, jury service, or natural disasters affecting your destination. This shields you from losing prepaid flights, accommodation, and tour bookings.

Personal possessions and baggage cover reimburses lost, stolen, or damaged belongings during your trip. Trip delay and missed departure benefits compensate for additional expenses when transport disruptions strand you or force overnight stays. Together, these coverages address the most common travel mishaps.

Claims in the UK have risen sharply, with medical costs making up the largest share. This trend reflects both increased travel volumes post-pandemic and rising healthcare expenses in popular destinations. Key claim categories include:

- Emergency medical treatment and hospital stays abroad

- Trip cancellations due to illness or family emergencies

- Lost or delayed baggage causing significant inconvenience

- Travel delays requiring accommodation and meal expenses

The surge in medical claims underscores why adequate emergency cover is non-negotiable. A single hospital visit in the United States or Australia can exceed £50,000 without insurance, dwarfing the annual premium cost. These statistics highlight the real-world value of comprehensive multi-trip policies for frequent international travellers.

How age and health affect premiums and coverage

Pre-existing medical conditions may be excluded unless declared and accepted. Insurers assess your health status during application, and failing to disclose conditions can void claims entirely. Common conditions requiring declaration include diabetes, heart disease, respiratory illnesses, and cancer history. Some insurers specialise in covering complex medical profiles, though premiums reflect the elevated risk.

For older travellers, higher premiums and stricter medical screening are normal, reflecting higher claim risk. Age thresholds vary, but travellers over 65 often face detailed health questionnaires and premium increases. Despite higher costs, annual cover remains worthwhile for active seniors making multiple trips, as single-trip alternatives price each journey individually at similar age-adjusted rates.

Managing your application effectively ensures you secure appropriate cover without unnecessary exclusions. Follow these steps if you have medical conditions or are a senior traveller:

- Gather complete medical records and medication lists before applying

- Answer health questions thoroughly and honestly to avoid claim denial

- Compare travel insurance with medical conditions specialists who understand complex health profiles

- Request written confirmation of accepted conditions and coverage limits

- Review travel insurance for seniors coverage options tailored for older age groups

Pro Tip: Specialist insurers often offer better terms for seniors and those with pre-existing conditions than mainstream providers. Obtain quotes from both general and specialist brokers to compare coverage scope and premiums, ensuring you find the best balance of protection and cost for your unique health profile.

Choosing the right policy for your travel needs

Selecting the optimal multi-trip policy requires matching coverage to your specific travel habits, destinations, health status, and budget. Start by counting how many trips you anticipate annually and their typical duration. If you take four or more trips yearly, annual cover usually proves more economical than multiple single-trip policies.

Destination matters significantly. Europe-only policies cost less than worldwide plans, but if you occasionally visit non-European countries, worldwide coverage avoids gaps. Consider whether you’ll travel to the USA or Canada, as these destinations often require higher medical limits due to expensive healthcare systems. Trip duration limits must accommodate your longest anticipated journey to prevent coverage lapses mid-trip.

Review policy documents carefully for coverage limits, exclusions, excesses, and speciality services. Medical coverage limits should reflect destination healthcare costs, with minimums of £2 million for Europe and £10 million for worldwide travel including North America. Excesses represent the amount you pay before claims activate, with higher excesses reducing premiums but increasing out-of-pocket risk.

The table below compares typical policy features to guide your evaluation:

| Feature | Economy tier | Standard tier | Premium tier |

|---|---|---|---|

| Medical cover | £2 million | £5 million | £10 million |

| Cancellation limit | £1,500 | £3,000 | £5,000 |

| Possessions cover | £1,000 | £2,000 | £3,000 |

| Trip duration max | 21 days | 31 days | 45 days |

| Geographic scope | Europe | Worldwide exc USA | Worldwide inc USA |

Roughly 12% of travel insurance buyers opted for annual coverage in 2025, suggesting growing awareness of its benefits despite remaining a minority choice. This market share reflects the product’s appeal to frequent travellers while highlighting that many occasional holidaymakers still prefer single-trip alternatives.

Follow these steps to select and purchase suitable coverage:

- Calculate your annual trip frequency and average duration to determine if multi-trip insurance suits your pattern.

- Identify all destinations you plan to visit and confirm geographic coverage includes each region.

- Declare all pre-existing conditions fully and compare specialist versus mainstream insurer offerings.

- Compare at least three quotes using identical coverage parameters via compare health care insurance for expats tools.

- Verify policy exclusions, excesses, and claims procedures before purchasing to avoid surprises.

- Set calendar reminders for renewal dates to maintain continuous coverage across years.

Pro Tip: Review your policy annually as travel patterns and health status evolve. If you start visiting higher-risk destinations or develop new medical conditions, upgrading coverage mid-term prevents gaps. Conversely, if travel frequency decreases, switching to single-trip policies may save money without sacrificing protection.

Explore tailored international insurance solutions

Navigating the complexities of multi-trip travel insurance becomes simpler when you access expert guidance and curated comparisons designed specifically for expatriates and frequent international travellers. Unparalleled Global Benefits specialises in matching travellers with optimal insurance solutions, whether you need comprehensive annual travel cover, expat health plans, or specialised protection for extended stays abroad.

Our platform offers detailed reviews of international expat health insurance providers, helping you understand coverage nuances and premium structures across leading insurers. Explore our top insurers section to compare policy features side by side, or use our compare health care insurance for expats tool to find personalised recommendations based on your travel frequency, destinations, and health profile. Securing the right protection starts with informed decisions backed by expertise.

FAQ

What is the maximum trip duration allowed under multi trip travel insurance?

Policies typically offer trip durations of 21, 31, or 45 days depending on the coverage tier you select. Each individual journey within your annual policy must not exceed this limit. If you plan a longer trip, you’ll need supplementary single-trip cover or a higher-tier annual policy with extended duration allowances.

Can pre-existing medical conditions affect my multi trip travel insurance coverage?

Pre-existing medical conditions may be excluded unless declared and accepted during application. Failing to disclose conditions can void claims entirely, even for unrelated incidents. Many insurers specialise in travel insurance with medical conditions, offering tailored coverage for complex health profiles at adjusted premiums.

Is multi trip travel insurance more cost-effective than single-trip policies?

For travellers making four or more international trips annually, multi-trip policies typically deliver better value by eliminating the need to purchase separate cover for each journey. Roughly 12% of travel insurance buyers opted for annual coverage in 2025, recognising both cost savings and administrative convenience. Compare total annual costs of your typical single-trip policies against one annual premium to determine your optimal choice.

Does multi trip travel insurance cover domestic UK travel?

Most policies include domestic UK trips alongside international journeys, provided each trip respects the maximum duration limit. This means weekend breaks within Britain count towards your coverage, offering protection for cancellations, medical emergencies, and possessions even when not crossing borders. Verify your policy wording to confirm domestic inclusion and any specific conditions.

How do I make a claim on my multi trip travel insurance?

Contact your insurer immediately when an incident occurs, ideally within 24 hours for medical emergencies. Collect all documentation including medical reports, receipts, police reports for theft, and booking confirmations for cancellations. Submit claims promptly with complete evidence to expedite processing. Most insurers provide 24/7 emergency helplines and online claim portals for convenience.

Recommended

- Annual Travel Insurance Cover 2025: Guide for Global Travellers

- Types of Travel Insurance: Essential Cover in 2025

- Annual Travel Insurance Including Cruise Cover: Complete Guide – Unparalleled Global Benefits

- 7 Best Annual Travel Insurance Plans for Seniors – Unparalleled Global Benefits

- All-Inclusive Cruise Vacations 2026 | All-Inclusive Cruises